Coast FIRE: So Hot Right Now

Why wouldn’t it be! I get to *coast* to financial independence? Sign me up! And robots + humans agree! It’s all the rage. ChatGPT will have a nice chug of our fresh water to tell you Coast FIRE is one of the “fastest-growing FIRE concepts,” and the fine folks of Reddit are migrating like birds from the Traditional FIRE community to the Coast FIRE one. Because Coast FIRE isn’t about *not* working, it’s about flexibility, whether that’s pulling back or doing something that feels more authentic to yourself. Both of which strongly appeal to the younger generation, who strive either to connect on a personal level with their work or to do less of it.

As planners, we love this calculation because it quickly shows how on track a household is based on their current savings. It answers whether you are generally on the right track and can start making changes to live with more flexibility today. At its heart, Coast FIRE is about being in a position to save less, which creates room for more spending or for not needing to earn as much.

As with all things personal finance, achieving true Coast FIRE isn’t the end all be all. The concept is often romanticized, so I’m sharing this blog to explain the calculator we use, how it works best, and when Coast FIRE could be a realistic vision for your household.

How Traditional FIRE Works

FIRE is an abbreviation for “Financial Independence, Retire Early”.

In Traditional FIRE, the endgame is to no longer work, period exclamation mark! How exciting! You save 25x your annual expenses and walk away completely because of the 4% rule. So if you needed $100,000 in income to cover your annual expenses in retirement, you would need $2,500,000 in retirement savings. This is because 4% of $2,500,000 is $100,000, and that’s what the rule says you could sustainably withdraw from an investment portfolio starting in your 60s. Huge money hack alert! Instead of getting rich quick, get rich by saving and growing your investment account over time, then use that money to replace your salary. Okay, maybe not as thrilling as rocking your bod in Tulum on Instagram while bragging about how much passive income you get from your rental properties! But this actually works and is 1000% less cringeworthy.

As with everything in the FIRE movement, the most attractive part is the “Retire Early” aspect. “How do I save enough money to stop working before the traditional retirement age of 65?” Boy, you might not like the answer to that question. Unless you are lucky enough to receive a financial windfall, you have to drastically increase your savings. And if the savings side of your financial lever increases, then the spending side must decrease accordingly.

That’s the rub. If you aren’t earning a high-end income that lets you reduce spending while still maintaining a pretty fulfilling lifestyle with some convenience spending and worthwhile experiences, you may be sacrificing a lot. And for a growing subset of the population, that’s exactly what occurred. People were just not living in their 20s, 30s, and 40s. They’d eat ramen noodles (honestly, not the worst part) for most meals and forgo any and all lifestyle expenses or wants (that part definitely stings). But by missing out on the experiences that help define who you are in your young professional years, you can save beyond the traditional guidance of 10 – 20% of your income.

It’s not for me to judge whether that’s right or wrong for those who celebrate, but there are, of course, drawbacks, some of which I don’t think were entirely clear at the outset. Besides cutting costs and the challenges that come with it, consider how it impacts your relationships with friends and family. If they don’t share the same lifestyle, it’s likely you’ll drift apart somewhat. Then, retiring early leaves a significant void in your daily routine from 9 to 5. Most of your peers around your age are probably still working. You’re not spending when your friends are most active, and you’re not working when they’re at their busiest.

Additionally, as planners we know it’s hard to transition from a “saver” to a “spender”. Many books have been written on the subject to help retirees enjoy the financial independence they’ve worked so hard to achieve. So there’s no guarantee you’ll be able to simply “turn it on” and start using your money as a tool for happiness after decades of drastic frugality. This resulted in various versions of the FIRE movement, one of which is now commonly known as “Coast FIRE”.

How Coast FIRE Works

Coast FIRE, Explained

First we makey the money, and then we SURF! Coast FIRE is a wonky name because it has nothing to do with living on the coast or even retiring early, at least in a traditional sense. Achieving Coast FIRE is to have enough investment savings that you no longer need to add to it. Your nest egg is already expected to grow enough to allow you to make sustainable withdrawals from it by a future date.

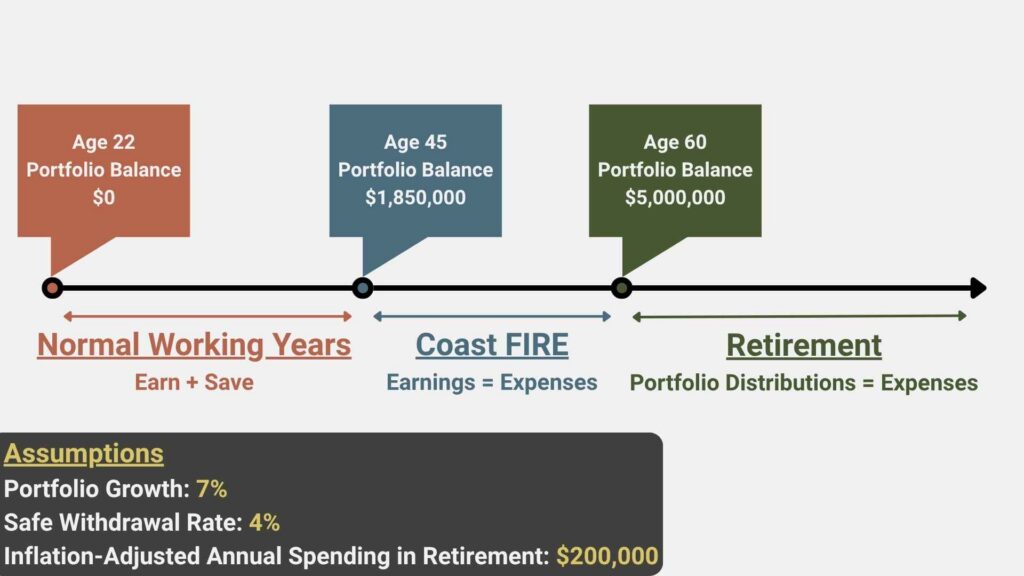

Here’s an example timeline with conveniently rounded numbers.

At Age 45, whether through regular saving or a sudden windfall, the example party finds themself with a $1,850,000 investment portfolio. While their annual living expenses are $130,000 at Age 45, this won’t remain steady forever due to inflation. So they need to calculate their inflation-adjusted annual spending in retirement. Assuming a 3% inflation rate, $130,000 in today’s dollars (Age 45) is equivalent to $200,000 in future dollars (Age 60). Hence, according to the 4% rule, they must accumulate an investment portfolio worth $5,000,000 to cover their $200,000 in annual expenses without working.

Using this same example and to make the math easy, let’s assume they saved an even $36,000 annually from Age 22 to Age 45, amassing the $1,850,000 portfolio. Let’s also assume they want to maintain their current spending from their normal working years and begin distributions at Age 60. By achieving Coast FIRE, they can reduce their income by $36,000 annually, and likely a little more, because, theoretically, they might pay less in income tax from Ages 45 to 60. So while they no longer have to add to their savings, for their Coast FIRE calculation to be successful, they still have to match their earnings with their expenses during their coasting years to avoid reducing their portfolio value.

Achieving Coast FIRE is defined by your earnings equaling your expenses in those coasting years.

Benefits of Coast FIRE

Wait, so I build up this epic portfolio, and I still have to work? Yeah… that’s right. In the example above, I used an even savings amount, but in reality you may be saving far more as you approach Coast FIRE than in earlier, normal working years. This may allow you to reduce your income by a more substantial amount.

Or you may have saved nothing and just received a sudden influx of money through the sale of a business, equity compensation, or an inheritance. It might be a number well over your Coast FIRE number, which may allow you to reduce your income by a larger amount.

Ultimately, you have to find a balance among the following levers: savings, spending, and how long you are willing to work. The longer you work, whether normally or during Coast FIRE, the less you need to save. The same concept applies to spending. If you are willing to spend less now or at your distribution age, that lowers the time you have to work or save.

True Coast FIRE allows for two (2) things before retirement age:

- You can spend more as you no longer need to save -OR-

- You can theoretically work less as you no longer need to earn as high of an income, assuming you can still cover all of your expenses.

When Coast FIRE Makes Sense

It’s helpful for households that did a great job saving in their 20s and 30s and now need permission to back off their savings rate because, deep down, they want to spend a little more or work a little less. Usually kids have entered the picture and bigger experiences or educational goals have come to the forefront.

And for pre-retirees who need a breather and are interested in working longer at something less strenuous while letting their current investments grow.

Overall, the calculation is most accurate for individuals planning to retire at a normalish age in their late 50s or 60s before they start drawing from their portfolio. It leaves less time for surprises.

When Coast FIRE Doesn’t Work Well

Saving shouldn’t be an all-or-nothing proposition. It’s beneficial to always save some while working, especially if it’s to collect a 401k match, avoid a high marginal tax bracket, or build in a cushion for when life happens or changes.

If I had a $1 for every time someone said they would “start consulting” and make about 70% of their current full-time salary, and could do that for decades by working only 5–10 intentional hours a week, I’d already be “consulting” myself! In reality, it’s hard to leave a stable, high paying job and become self-employed as a consultant or to follow a passion that also covers all of your expenses.

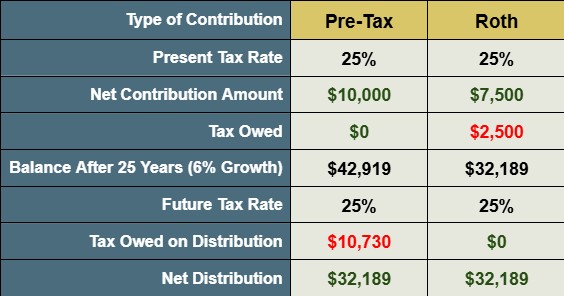

*How* the money is being saved adds uncertainty, as does future taxation. Of course, for a true calculation, it really needs to be your investment portfolio in post-tax dollars. But it’s hard to make blanket assumptions about tax rates across different buckets in the future. All of which have different effects not just on the taxation of the distribution, but also on eligibility for healthcare subsidies. Some of which is in your control (the act of the distribution itself), and some of which just isn’t (tax rates, penalties, healthcare subsidies).

Your “Coast FIRE” number is only as accurate as your true annual spending, and the earlier you stop saving or plan to fully retire and start taking distributions, the more that number tends to fluctuate as you hit certain milestones (paying for your kid’s college, paying off a mortgage, receiving Social Security, not having health care). Change is a certainty, and this calculation needs to be revisited often.

How We Calculate Coast FIRE

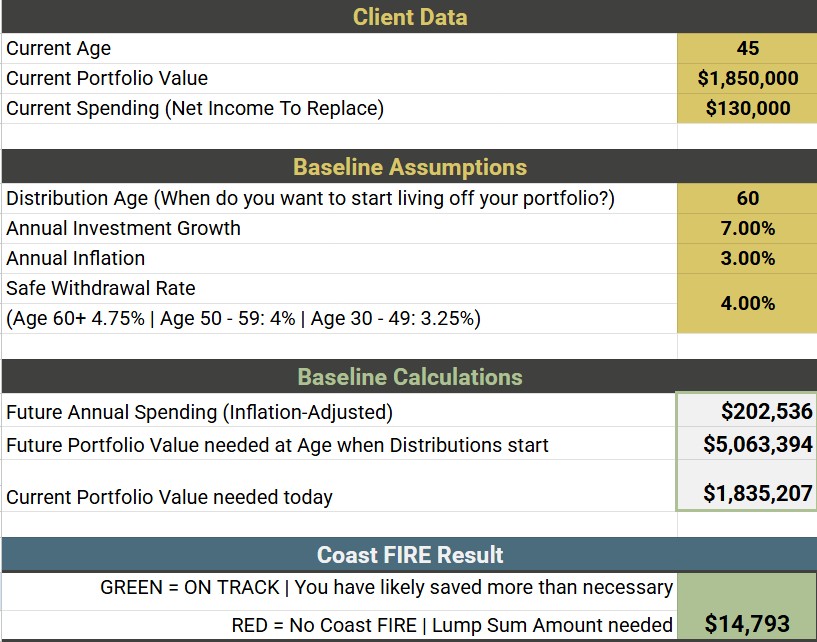

I present the calculator we use with our households to quickly gauge their Coast FIRE possibilities. Consistent with the example in the graphic above, I used the same assumptions. This results in our example client having saved $14,793 more than necessary at Age 45, enabling them to Coast FIRE until a starting portfolio distribution age of 60. I continue to note that they still have to earn enough from ages 45 to 60 to replace their net income of $130,000 until distributions start. If they earn less, they have to spend less so they do not need distributions from their portfolio.

While there are different, more complex, and certainly more involved or aggressive ways to model the “safe withdrawal rate”, this simple calculation isn’t meant to replace financial planning software or a review of your entire financial picture. We just want to know how on track you are at the moment. And that will likely change year to year.

Why Compound Interest Makes Coast FIRE Possible

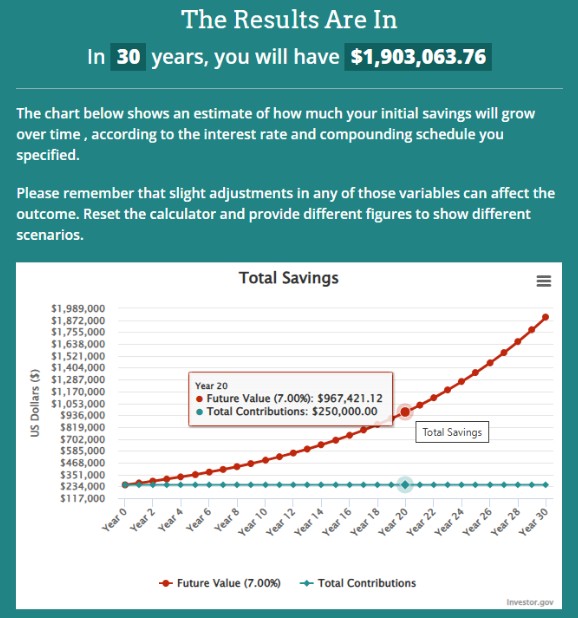

Your money still needs time to grow during those coasting years because Coast FIRE relies on compound interest, which demands time. Compound interest is really like an angsty teenager. Just leave me alone, man!!!

In the scenario below, if you had a $250k nest egg and never added to it, it would take 20 years to grow to almost $1M. And then the magic happens in the subsequent decade as your $1M nest egg grows to almost $2M by year 30. The slope of the Y-Axis (US Dollars) gets drastically steeper in those later years. A 7% gain on $250,000 is $17,500, but on $2,000,000 it is $140,000.

To Coast FIRE successfully is to let compound interest do its job. While time is necessary, the other component is money. You need a starting point that can get you where you need to go on whatever time horizon you’ve set. And that means you either:

- Saved and saved and saved while young

- Grew your savings later in life and are able to move into a role that allows you to delay taking distributions

- Received a sudden, life-changing financial windfall but just want to keep working for some arbitrary amount of time

- Built up a concentrated equity position and it performed very well

In any of these scenarios, you may actually have enough money to pursue Traditional FIRE, but you’re avoiding it because you enjoy working in some capacity, or you want to spend MORE in retirement, or you’re building in a safety net because you have no clue where life will take you decades from now.

Common Coast FIRE Mistakes

Coast FIRE can be challenging or misinterpreted when people flirt with it but really just want Traditional FIRE. As explained, the whole point of Coast FIRE is to continue working in some capacity to cover your normal living expenses, not to dip into your nest egg. So distributions, for any reason, work against you and can result in you needing to work longer or start saving again. Therefore, if you’re only just on track to achieve Coast FIRE, you can’t also claim that you want to reduce work in a way that involves withdrawing from your portfolio to meet your expenses. Unless, of course, you account for that cash withdrawal by reducing your starting portfolio value needed in the first place. Ultimately, Coast FIRE isn’t suitable for someone who merely wants to toy with working after their normal career years, since they can’t really fully exit without replacing that income. This isn’t really a F-YOU money situation. The further you are from your anticipated distribution age, the more harmful an unplanned distribution is from your portfolio.

And Really the Biggest Challenge

It’s hard for most to find that ideal job/balance. As mentioned, Coast FIRE is a little daydreamy. You imagine quitting a lucrative role as a law firm partner or in tech to pour beer at a brewery or pursue a career as an artist. Or simply go to work one day and announce that you will drastically reduce your hours and alter your day-to-day responsibilities. And in return, feel free to pay me 30% less. In most cases, following a passion or starting a business and going to $0 income isn’t what Coast FIRE is about. For most, the bigger the departure from your current earning capacity, the more drastic your spending cuts have to be. Some will find that easy. Others will find it very difficult.

In either case, you need a solid grasp of your cash flow. We run this calculation a lot, and clients sometimes insist they don’t need a certain amount of money to live on, saying the annual spending figure feels too high. But their numbers tell a different story. We know their income, tax liability, savings, and larger fixed expenses that will *hopefully* run out someday (tuition, mortgage payment). Everything else is being spent. We know the number, and just because some things are more expensive in your current season of life (kids) doesn’t mean other types of expenses won’t be in the future (health).

Is Coasting Right For You?

In my view, running this calculation is more valuable than following any BuzzFeed-like money rule articles that many major investment custodians or financial blogs publish, which suggest you should have $X saved by age 30, $X by age 40, and so on. We are all trying to slay the work/life balance dragon. And a proper Coast FIRE calculation attempts to account for your personal strategy. Like with any aspect of personal finance, you want to feel empowered to make the decisions that are right for you. Knowing what’s right for you involves asking the question, “What is enough?”

Frequently Asked Questions About Coast FIRE

Q1: What is Coast FIRE?

Coast FIRE is a financial independence strategy where you’ve already saved enough that your investments are expected to grow into your retirement nest egg without additional contributions. Rather than continuing to aggressively save, you only need to earn enough income to cover your current living expenses until retirement.

Q2: How do you calculate your Coast FIRE number?

Your Coast FIRE number depends on several factors, including your current age, expected retirement age, annual retirement spending, anticipated investment returns, and inflation. The goal is to determine how much you need invested today so compound growth alone can fund your retirement without future retirement contributions.

Q3: Does Coast FIRE mean you can stop working?

No. Coast FIRE assumes you’ll continue working to cover your living expenses until retirement. The difference is that you no longer need to save aggressively because your existing investments are expected to reach your retirement goal on their own.

Q4: Is Coast FIRE better than Traditional FIRE?

It depends on your goals. Traditional FIRE focuses on leaving the workforce as early as possible, while Coast FIRE prioritizes flexibility by reducing the pressure to keep saving. Coast FIRE can be a better fit for people who enjoy working but want more freedom to reduce hours, change careers, or spend more during their working years.

Q5: What are the biggest risks of Coast FIRE?

Coast FIRE relies on assumptions about investment returns, inflation, future spending, and retirement timing. Unexpected expenses, market downturns, or withdrawing money from your portfolio before retirement can delay your plan. Reviewing your Coast FIRE calculation regularly helps ensure it continues to reflect your financial situation and long-term goals.

Mike Turi, CFP® APMA™ is the Founder and a Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.