Wedding Budgeting for Couples: How to Plan a Wedding Without Financial Stress

For most couples, planning a wedding marks their first serious financial discussion together. It’s a major step up from playful “we don’t even need to spend money to have fun together” dates or choosing a restaurant. Add in varying family wealth levels, a saver versus spender dynamic, and a tight schedule, and it’s almost like Leo Beiderman and Sarah Hotchner getting married with a huge asteroid looming (Deep Impact reference!). Sneaky move by Leo, too – “Marry me because it’s your only chance to survive.” Romantic! All to say, navigating this milestone together requires collaboration, trust, a shared vision, and, of course, a spreadsheet.

Here’s how you can ensure your wedding experience is fulfilling and enriching for your soul, instead of being stressful and exhausting while trying to meet someone else’s idea of the perfect event.

Open Communication is Key

Create a Vision Board

Exchange your visions for the event and the corresponding weekend. Where are you? How many separate events are there? Are you heading straight to a honeymoon?

Separate your vision board into three (3) columns:

Non-Negotiables

Nice-to-Haves

Won’t Go Into Debt for

This will help organize the process of weighing trade-offs among various vendors and focus on what matters most. Our firm believes that how you live your life and celebrate important moments matters.

Therefore, we encourage you not to hold back while creating your vision board, even BEFORE discussing the money.

Finding a Realistic Financial Starting Point for Your Wedding

Disregard Broad Data Re: Wedding Spending

“What do weddings actually cost?” A well-intentioned question, but the answer completely misses the point. There is no one-size-fits-all wedding. And while this is just one data point, I’d argue it does more harm than good. Don’t emotionally anchor how much you should spend on your wedding to the “average” cost others spent on theirs. “Oh, the average wedding cost in Louisiana is $34,000, but we *feel* like we are doing better than most, so we probably can spend twice that amount.” Disaster!

Transparency Around Money

Without completely depleting your household’s individual savings, how much money do you have to contribute to the wedding today? This will vary depending on the household. Besides the emotional concern of how much savings you’ll dip into, it’s important to be realistic about factors such as job security, the ability to rebuild your emergency fund, and the opportunity cost of allocating this money elsewhere. Losing sleep over overextending yourself on your wedding and living paycheck-to-paycheck, or worse, accumulating debt without a realistic payoff plan, won’t help create a stress-free experience.

When It Comes to Stakeholders, Don’t Assume!

Bizarre traditions are well, bizarre traditions. Never assume that one partner’s family will pay for the entire wedding. If you’re fortunate enough to have stakeholders, approach them candidly about what they can contribute. Understanding their financial input will help you better align their resources with a meaningful part of the weekend. More on that later!

Establishing a Timeline

It’s not only the newly engaged who need assistance with wedding budgeting; parents may also be overwhelmed. Even if you believe your parents can cover part of the costs, their funds might not be instantly accessible. Engagements tend to happen rather abruptly. As a financial planner, I frequently see that parents need extra guidance on how much they can contribute and a pathway to making those funds liquid when needed. There’s nothing wrong with having a long engagement, especially if it gives you more time and opportunity to save for your wedding.

Enter: The Spreadsheet

Yes, you need a spreadsheet. Fortunately, you don’t have to start from scratch. Many wedding-oriented websites offer a free one to help you get started. Here’s what I think is important to track:

Estimated Cost

Actual Cost

Difference (Estimated Cost – Actual Cost)

Vendor Name

Vendor Contact Details

Deposit Amount

Paid (YES/NO)

Final Payment Due Date

Amount Remaining

Source of Payment

Once your spreadsheet is set up, I’d recommend narrowing down your guest list. Who NEEDS to be there? The venue is the most consequential decision you have to make, so make sure you research venues that fit your mandatory guest count. Now you can start getting a feel for what venues cost, what dates are available, and what’s included in the price. You can duplicate your spreadsheet to compare different venue scenarios. Some may include everything in the price, while others only provide the bare space. This will also allow you to experiment with your expected guest count and see how it impacts your budget. Remember, it all comes down to identifying your non-negotiables, which definitely includes guest attendance. If you can afford your “nice-to-have” items, that’s an added bonus!

As you start pulling in quotes from vendors, it’s a great time to revisit discussions with your parents or stakeholders. Instead of giving you a check, it may be more meaningful to “sponsor” something. Whether it’s the band, a dress, or a reception dinner, this is an excellent way for them to feel more connected to the wedding. Hell, that excitement may even put a few more dollars in your pocket.

Budget vs. Reality

There’s your original budget, and then there’s reality. CRINGE MEME, sorry Gen Z!

Wedding expenses are similar to home renovations; once you start, it’s hard to stay within your budget. Unexpected costs will arise, and you’ll find it hard to resist adding certain items.

The more you think you thought of everything, the more surprised you’ll be that you haven’t. You should anticipate paying 1.5 to 2x your original budget.

Show Me The Money

Wedding Fund Location

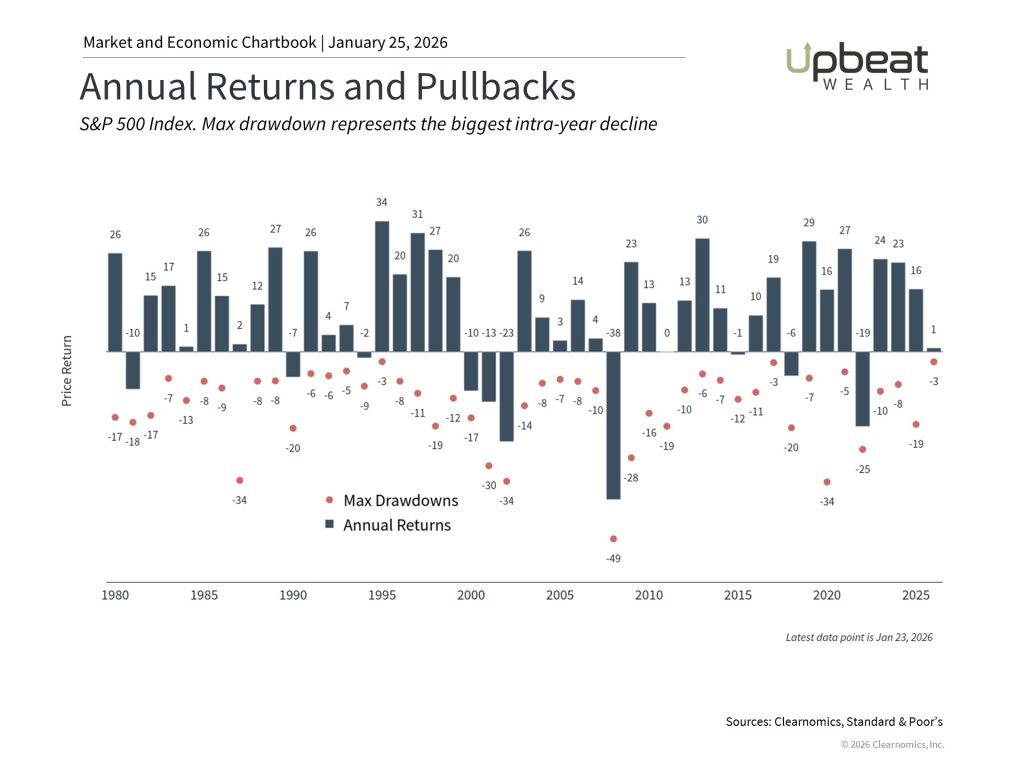

You’ve set money aside, and you’re continuing to save, but where does it go? While you may be able to postpone other large purchases, like a home, if investment returns don’t align with your desired timeline, a wedding has a definitive date, and most of the money is due before it happens. Therefore, you should not be looking to *grow* this money as if it were your long-term retirement fund. Keep the wedding expense money in cash and liquid. If you’re already using a portion of your investments to fund the festivities, it can be tempting to keep it invested. But you’re taking a huge gamble that your wedding could become incredibly more expensive if you have to sell those assets at an inopportune time.

See the illustration below, which shows that the average year sees a stock market drop of -13.5%.

It’s Okay to Pause Retirement Savings, But…

This may be an unpopular opinion, but I’m okay with you pausing your retirement savings to help absorb the cost of a wedding (if that’s something you value!). Life is for living, and it’s okay to lean into those moments. But you should really have a plan for getting back on track. Extenuating circumstances aside, a majority of families should be putting atleast 10% of their gross income toward their retirement. This also isn’t great if you’re losing your 401k match. It’s another *hidden* cost that increases the overall expense of the wedding.

In personal finance, you either make small behavioral changes now or face the need for drastic changes later. And while the roadmap isn’t or doesn’t need to be universal, it tends to get harder, not easier, post-wedding.

The Wedding Economy is Real… Expensive

This is just an anecdote from our wedding, but we were surprised at how costly some rental items were. Instead, we chose to *purchase* certain items and resell them afterward. My wife heroically handled ordering custom pieces from Alibaba for less than the rental cost. We then resold those items on Facebook Marketplace because, well, is there any other place to buy anything? Used is Vintage. Vintage is Beautiful! We also purchased a used Cricut, which helped us create and further customize decorations. I say *we/us* very liberally. I’m not even sure I qualified as an elf in this Santa wedding workshop my wife was running.

Debt Can Be An Ally, But It Is Not Your Friend

There are three (3) important distinctions when it comes to using debt to fund a portion of your wedding, whether it’s through credit cards, venue payment plans, or a personal loan.

- Opportunity cost is in your favor. You already have the money, but you are taking advantage of a promotional opportunity that lets you keep it earning interest by shifting certain expenses to a later date.

- Income is coming, but you need some extra time. You have a completely reasonable path to paying off the wedding in full from your income/wages, and you are using a 0% credit card promotional rate with some timely benefits (honeymoon!) to create extra runway.

- This is a YOLO moment, and you’re taking on high-interest debt you can’t afford to pay off now or in the future without a substantial change in your financial situation.

As mentioned earlier in this post, it’s important to be very clear about where to draw the line and what expenses aren’t worth going into debt for. Financial issues are the primary source of stress in relationships, so accumulating debt on day one is not a recipe for success. Which is my next point…

The Wedding Is The Beginning, Not The End

The beautiful thing about working with young couples is the cluster of milestones that tend to happen close together. Weddings, homes, starting a family, maybe even starting a business. Don’t lose sight of your longer-term goals. Always keep your vision of a wealthy life in mind and collaborate openly with your partner to define and live out your shared statement of financial purpose.

Frequently Asked Questions About Wedding Budgeting

Q1: How much should a couple spend on a wedding?

There is no “right” amount to spend on a wedding. Couples should base their budget on available cash, income stability, future goals, and what they value most—rather than national or state averages.

Q2: Is it okay to go into debt for a wedding?

Debt can make sense in limited situations, such as using a 0% promotional credit card with a clear payoff plan. High-interest debt without a realistic repayment strategy can create long-term financial stress early in a marriage.

Q3: Where should wedding savings be kept?

Wedding funds should be kept in cash or a high-yield savings account. Because weddings have a fixed date, investing this money exposes couples to unnecessary market risk.

Q4: Should couples pause retirement savings to pay for a wedding?

Temporarily pausing retirement contributions can be reasonable if there’s a plan to resume quickly. However, couples should account for the lost employer match and long-term opportunity cost.

Q5: How can families contribute without causing conflict?

Open conversations about expectations and boundaries are key. Allowing family members to “sponsor” specific wedding elements can help them feel involved without losing control of the overall plan.

Q6: Why do weddings almost always exceed the original budget?

Unexpected costs, upgrades, and emotional decision-making add up quickly. Couples should plan for wedding costs to be 1.5–2x their initial estimate.

Q7: What’s the biggest financial mistake couples make when planning a wedding?

Anchoring decisions to average wedding costs instead of their personal financial reality—often leading to overspending or unnecessary debt.

Mike Turi, CFP® APMA™ is the Founder and a Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.