The Price of Admission

When it comes to funding higher education for your children, knowing what it will cost remains the trickiest part of determining how to save for college. You’re mostly guestimating the cost of college 10+ years from now and how much funding your child will need.

Internal Factors:

State of Residency and In-State School Cost/Desirability

Will they attend college?

Scholarships/Grants/Financial Aid

Career Goals, Public Student Loan Forgiveness Eligibility

External Factors:

Future of Student Loan Borrowing Terms

Educational Cost Inflation

I’m not sure what’s tougher, getting a read on your 4-year-old or your government. So, instead of making predictions, let’s review the current landscape of attendance costs and some rule-of-thumb approaches toward setting educational goals and funding them.

2024-25 National On-Campus Average Cost of College (Tuition, Fees, Housing, Meal Plan)

Public Four-Year In-State: $29,910

Public Four-Year Out-of-State: $49,080

Private Four-Year: $62,990

To bring those numbers closer to home in Louisiana, here is the cost of attendance at the four most widely attended local universities:

LSU: $27,876

ULL: $23,392

Southeastern: $19,992

Tulane: $92,328

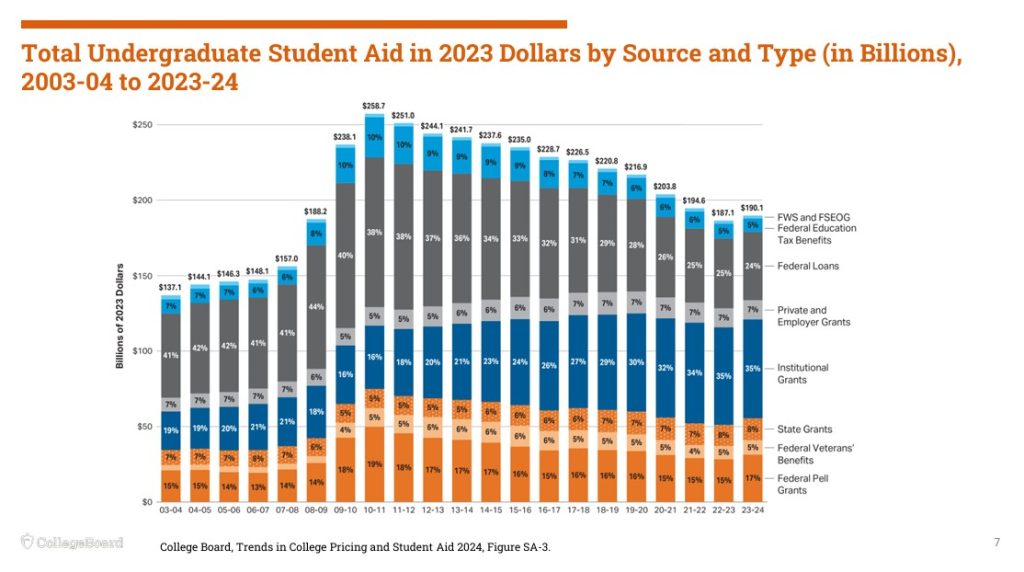

Education Inflation (Not Terrible Anymore?) and Trends in Financial Aid

We always take a conservative approach at Upbeat Wealth, so our in-house assumption for education inflation is 5%, which reflects the price increases of the last 30 years. The silver lining is that most of the increases happened between 1995 and 2015. From 2015 to 2025, the cost of attendance has moved more in line with the general inflation rate of 3%. Want to learn more about trends in college pricing? Here’s some great data from Collegeboard.org.

The other encouraging trend? More students are receiving some form of financial aid – and it’s the good kind! Grants, free money that doesn’t need to be repaid, are increasing as a percentage of total student aid. This has led to a decrease in federal loans, although this data does not include private loans.

Setting an Education Funding Goal

The best metaphor I’ve ever heard for setting an education funding goal for your kids is the same protocol you’re instructed to follow if there’s a drop in cabin pressure on an airplane. When oxygen masks drop in an emergency, put yours on first before assisting others. Another tired analogy would be that there are student loans, but there aren’t retirement loans. It’s important to ensure you are on track for your definition of retirement before funding education goals. If you aren’t careful, you might unintentionally shift the burden of your kids taking out student loans—which can often be managed through forgiveness or paid over time—to supporting your retirement or covering the high costs of end-of-life care.

If we broadly define “ensuring you are on track for retirement,” it would mean saving at least 10% of your income annually. Obviously, there are about a gazillion other variables that go into this, but I think that’s simple enough for the purposes of this blog.

Okay, so you’re contributing 10% of your income annually, but also have a couple of kids, so what’s next?

Here Are Two Goal Funding Frameworks That Households Have Had Success With

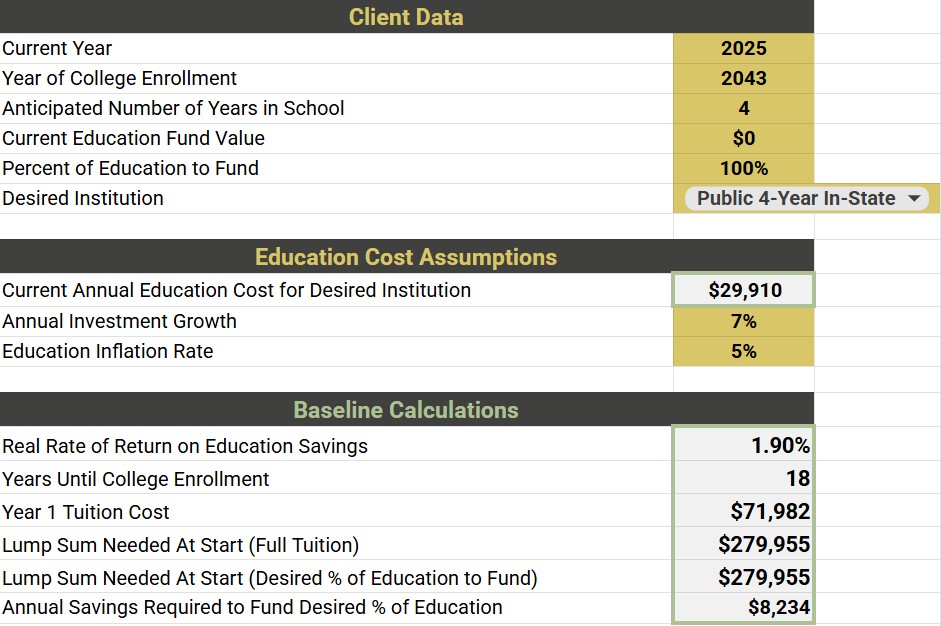

Saving Strategy No. 1: Aim to Save Enough to Cover 100% of a Public 4-Year In-State College

Even if you prefer your child not to stay in-state, this offers a generous starting point before they need to consider taking on some financial responsibility and having skin in the game to attend a higher-cost university. E.g., that degree better be worth it.

To do this, you need to save approximately $685 per month. Here’s an example using our calculator and a few assumptions.

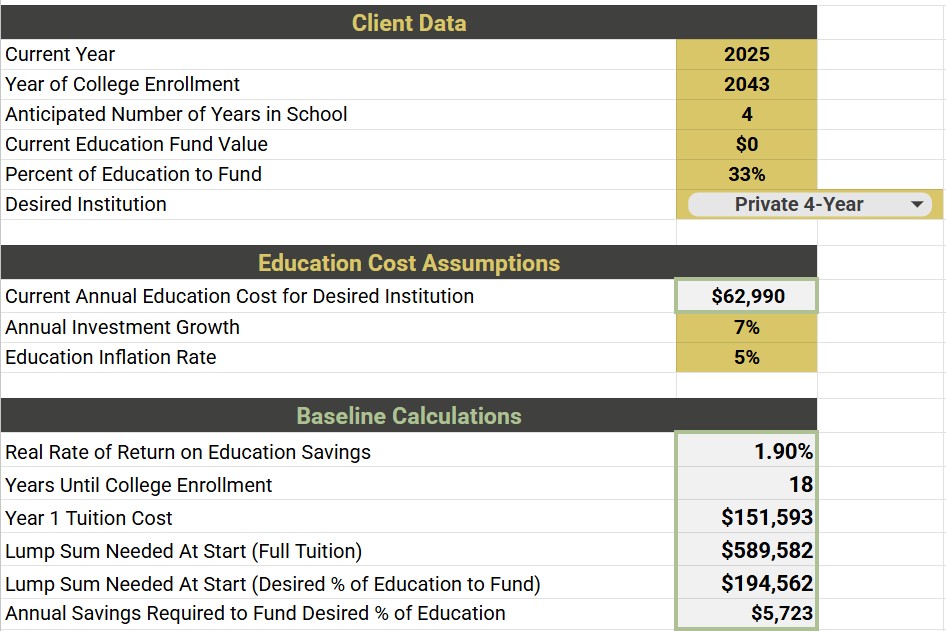

Saving Strategy No. 2: You Save ⅓ Now, You/Financial Aid Pays ⅓ Then, They Borrow ⅓ to Pay in the Future

I first learned about this strategy from another financial planner, Meg Bartelt with Flow FP. I really like it because it covers a little of everything—about a third, actually! You save a recurring amount that will satisfy a ⅓ of the price of college. Then, during the years your child is in college, you make some trade-offs to cover another ⅓ of the cost from your income, and hopefully, there’s some financial aid involved. Finally, your child covers the remaining ⅓ through student loans, which you can, of course, help them pay off with your future earnings if you wish.

It’s a great framework to start saving right away and then reevaluate as you get closer. Maybe you’re in good shape for retirement and can contribute more than a third during the enrollment years. Perhaps your child doesn’t even need to know that, and you can laugh at them as they complain about student loans. Or maybe you can act as the lender on the student loans and offer better terms than the federal government, which still believes it’s a good idea to burden our youth with high interest rates as they work to further their education and build a foundation for a fulfilling life.

It’s just a balanced way of saying, hey yeah, I care. I’ve done something to help you. Perhaps I can do more when I earn more, and I feel confident that I am taken care of. And by the way, it’s your life, take some responsibility for what you hope to get out of this education.

Here’s another example using the same assumptions as above, but this time to save enough for 33% of a Private 4-Year education. You would need to save about $475 per month now for the first third. If you chose to pay another third at the time of attendance, you’d be looking at approximately $50,000 per year for those 4 years, assuming they didn’t receive any financial aid.

Where Do I Actually Save The Money For My Child’s Education?

Okay, you’re doing a good job saving for yourself, and now you’ve created an education funding goal. Where the heck does this money go? Here are common options, along with our assessment of each.

Option 1: Uniform Transfers to Minors Act (UTMA)

This is not much different than setting up a normal brokerage account at a Schwab, Vanguard, or Fidelity. You maintain custodial power over the money inside this account until the beneficiary listed reaches the age of majority, which is now 22 in Louisiana. A quick note: the age of majority varies by state. In Louisiana, it was historically 18. This meant that if you contributed $100,000 to a UTMA account for your child, once they turned 18, they could use the money however they wanted. That makes for a fun first year of college.

UTMA Pros

“Kiddie tax” rules for 2025 allow you to pay no tax on the first $1,350 of earnings annually (dividends, interest, capital gains). The next $1,350 of earnings are taxed at the child’s tax rate, which is likely zero.

The beneficiary can use this account for anything without restrictions. It doesn’t just have to be for educational purposes.

More investment options, but that doesn’t necessarily mean *better* options, at least not in Louisiana.

UTMA Cons

Lack of control. The money that you contribute to this account is an irrevocable gift. You can’t just change your mind and reclaim it. Once it’s in there, your only responsibility is to manage it as the custodian for your child’s benefit.

High assessment rate when your child fills out the Free Application for Federal Student Aid (FAFSA). Because this is a child-owned asset, any financial aid they would have otherwise qualified for would be reduced by 20% of the UTMA’s value.

The beneficiary can use this account for anything without restrictions. Once they hit the age of majority in your state, that money is theirs. While 22 is better than 18 in Louisiana, it’s still pretty young to inherit a lump sum of cash. Most 22-year-olds I know don’t stop wanting to spend money after they graduate from school. Usually, they’re making big decisions about the affordability of renting homes and leasing cars. Well, things have just become a whole lot more affordable, and perhaps only temporarily, until the money is gone.

Our UTMA Assessment: The lack of control, combined with the beneficiary’s early access to the funds, makes this option pretty unattractive. With the recent rule changes increasing the flexibility of the 529 Plan (our next option) beyond college tuition, there is no longer a worthwhile benefit to having an UTMA account. Unless you’re not interested in them using this money for postsecondary education and don’t mind the possibility of giving your child a lump sum at an age when they’re most likely to spend it on something questionable. That’s TRUST.

Option 2: The 529 Plan

Last year, I filmed a segment for Great Day Louisiana and wrote a blog about the Louisiana START 529 Plan. Since then, with the recent passing of the One Big Beautiful Bill Act (OBBBA), 529 Plans have become even more lenient on how you can use/access the cash beyond college tuition. Here’s a big list of qualified withdrawals. You can contribute up to a lifetime maximum of $35,000 to a beneficiary’s Roth IRA, but there are certain caveats and restrictions.

Here are some of the main pros and cons of Louisiana’s 529 START Plan. To find out how your state’s 529 plan compares, visit the SavingForCollege website, which outlines the key features of each plan.

Louisiana START 529 Plan Pros

LA State Tax Deduction. $2,400 Single & $4,800 Married Filing Jointly per beneficiary. If you contribute more than the maximum annual deduction amount, the excess carries forward as a deduction in subsequent years.

Earnings Enhancement. Louisiana matches between 2% and 14% of your contributions based on your Adjusted Gross Income.

Tax-Free Growth and Distributions. Money grows tax-free and can be withdrawn tax-free if used for qualifying purposes (see link above re: qualified withdrawals).

Maintain Control. The beneficiary is never entitled to the money. You can change beneficiaries on the account as many times as you’d like.

Louisiana START 529 Plan Cons

Separate Account Location. Some may find it inconvenient that you have to open up the plan directly through the STARTSaving.LA.gov website. It is technically one more thing that you’ll have to keep track of.

Penalties. While the list of what constitutes a qualified expense continues to grow, if you make an unqualified distribution, you may be subject to paying income tax on the earnings as well as a 10% penalty.

Small Impact on Financial Aid. When owned by a parent, there is a slight reduction in the financial aid your child could qualify for, but this is much less severe than the penalty for an UTMA.

Our 529 Plan Assessment: The 529 Plan is the premier vehicle for saving for your child’s future education. Workarounds, such as being able to pay for K-12 tuition and possibly contributing a maximum of $35,000 to a Roth account, have made this option more attractive for funding at higher levels in recent years. Our only caveat is that we typically recommend families aim for 33% to 66% of funding through the 529 plan to limit the risk of overfunding. There’s always a possibility that you’ll need that money for other purposes, and current workarounds and increased flexibility for non-penalized withdrawals might still be insufficient.

Reasons that the percentage would be closer to 66% rather than 33%? You have multiple children, which increases the chances that someone in your family will benefit from the money. Or you have the financial means to the extent that you wouldn’t mind if the money ends up going to your grandchildren.

Option 3: A Taxable Brokerage Account

You keep the money in your name and just set up a separate account so it’s not commingled with your general investment funds. We strongly advocate using separate accounts, each designated for a specific investment goal, to save money intentionally. When money is mixed together, it’s harder to maintain a clear investment strategy, and you might feel guilty spending it when that goal isn’t predetermined.

Taxable Brokerage Account Pros

Ultimate Control & Flexibility. Money is yours to spend however you see fit.

Taxable Brokerage Account Cons

Taxes, of course! You’ll be taxed along the way on dividends and interest. While there are strategies to reduce capital gains taxes, you’ll likely pay something when you sell appreciated investments to access the money.

Our Taxable Brokerage Assessment: Tax planning is a major part of our work. We believe it’s one of the most important ways we deliver value to our households. However, this is one of those cases where I think that maintaining control and flexibility to supplement your education savings makes a lot of sense, even if it comes with a higher tax liability. Yes, when you earn money in a taxable account, you owe taxes. But it’s not uncommon for a carefully planned and financially smart strategy to fail and end up costing a household much more just because life threw them a curveball. This is like contributing to a 401k plan without having a proper emergency fund. It might have saved you money initially, but if something happens and you need to withdraw funds from the 401k, you’ll face taxes and penalties, which could end up costing you much more.

Our Overall Assessment: Ultimately, we believe the 529 Plan and the Brokerage account are a perfect marriage for Louisiana residents seeking to optimize their tax savings, receive a state funding match, maintain flexibility over the funds, and help jumpstart educational and non-educational goals alike.

Statistically, More Education Is The Best Way To Increase Earning Power

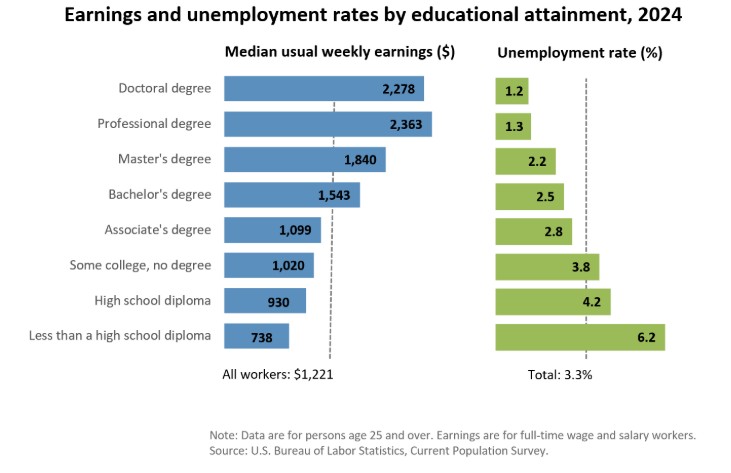

As I speak with more and more families, there is a growing sentiment that college will not be a driving force of personal economic growth for their children. There’s also considerable frustration with the system. These certainly go hand in hand. Of course, college isn’t the be-all and end-all. There are numerous lucrative paths for those who don’t follow the traditional route. Anecdotal examples are everywhere, from Fortune 500 CEOs to your cousin, Bill. However, the chart above from the Bureau of Labor Statistics shows a very clear picture. If you put a ceiling on your education, it becomes tougher, not easier. For now, there still is a real benefit in exchange for the price of admission.

Mike Turi, CFP® APMA™ is the Founder and a Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.