Why Buying or Leasing a Car Feels So Complicated

Choosing a set of wheels is on the Mount Rushmore of tough consumer decisions. It’s right up there with becoming a homeowner, choosing health insurance, or paying for childcare. And while having a roof over your head, access to good healthcare, and seeing to your child’s safety are probably more important, securing reliable transportation is by far the most aggravating of the bunch. It’s a pressure cooker of aggressive sales tactics, opacity, and time-consuming negotiations. All set to leave you emotionally drained and ready to just be done with it already.

How can anyone reasonably expect to compare all deals when the combinations are endless and constantly changing? We can trick ourselves into thinking we got the “best deal”, but you’ll truly never really know. Furthermore, you won’t even know if it was a good deal, let alone the “best deal” for you until 3, 5, or maybe 10 years after making it. So I truly believe that purchasing or leasing a car just had to *feel* good. And for something to feel good, you need to understand some rules of thumb and key terms. Let’s discuss the pros and cons of buying versus leasing, what to expect when financing, how to choose the right car, and ways to boost your leverage during negotiations.

Key Terms You Need to Know Before You Buy a Car

MSRP (Manufacturer’s Suggested Retail Price): As the name suggests, it’s what the manufacturer recommends you pay for the car.

Dealer Add-ons: Dealers sometimes add silly things like “paint protection,” which aren’t standard vehicle add-ons, to increase profit on a car.

Dealer Mark-Ups: Extra fee/profit added to vehicles in high demand with limited supply.

Sales Tax: State/Local Tax on Vehicle Price. Most states also allow you to deduct any trade-in value, lowering the amount you are subject to sales tax on.

APR (Annual Percentage Rate): When financing, the interest rate is separate from the APR, which combines the interest rate with any extra fees included in the loan.

Depreciation: Decline in a vehicle’s value over time, affecting resale value.

Key Terms You Need to Know Before Leasing a Car

Net Capitalized Cost: The price of the car that the lease payments are based on. Can include vehicle cost along with other fees not paid up front.

Residual Value: Set at the beginning of the lease by the manufacturer, it’s the estimated value of the car at the end of the lease. It’s also the price you have the option to buy the car for at the end of the lease. The actual market value at the end of the lease may be higher or lower.

Money Factor: the interest rate on a lease, but expressed as a small decimal rather than a percentage. To get the percentage, multiply the money factor by 2,400.

GAP Insurance: Covers the difference between what you owe on the car and the fair market value. Required by most dealerships, but you can add to your existing auto insurance policy rather than roll it into your monthly lease payment. It’s also a reason to try to avoid putting a down payment on a lease. If your car is totaled, the insurance company will just pay off what you owe on the car, not what you’ve already paid.

Mileage Allowance: Maximum miles allowed annually before incurring extra cost.

Buying vs Leasing: Which One Is Right for You?

When Buying Makes More Sense

Anticipate using the car for longer than the financing period, or at least 6+ years.

Drive the car more than the usual 10,000 to 15,000 miles per year common in leases, which can lead to higher mileage and wear-and-tear fees.

When Leasing Makes More Sense

Enjoy having a new car every 3 years.

Are uncertain whether you’ll want/have/need this car beyond the lease period.

Prefer less hassle/maintenance in your life.

Really just need a lower monthly payment because you have other financial priorities at the moment, or can’t afford a 20% down payment when buying a new or used car.

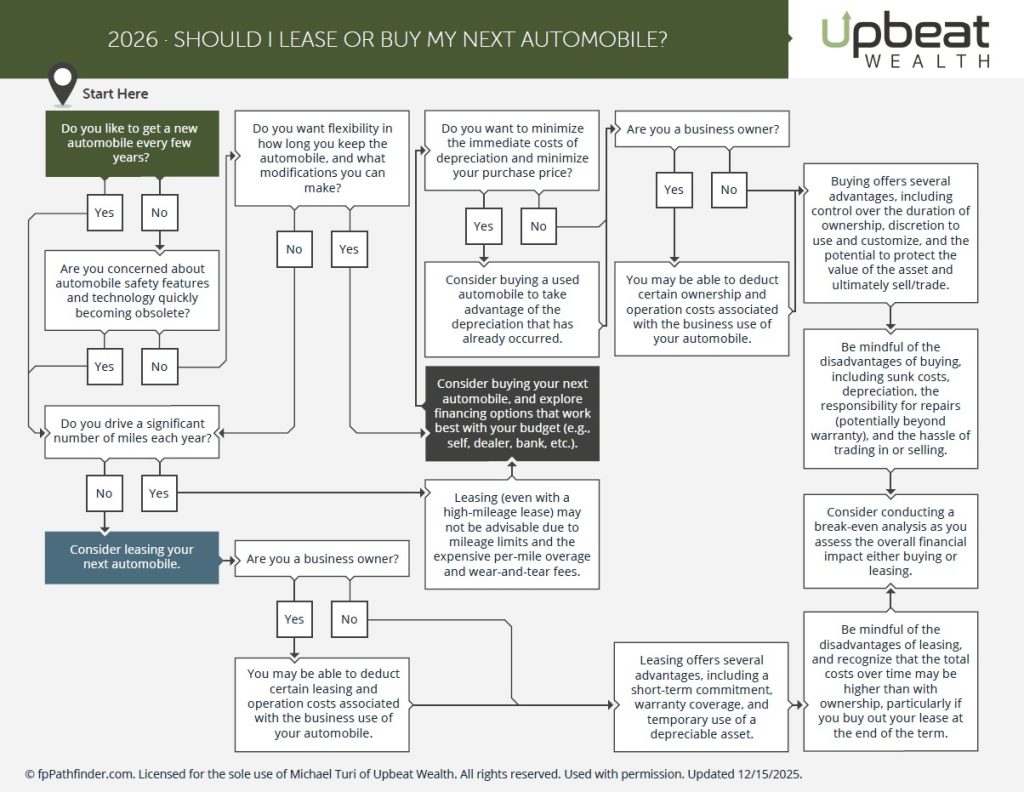

Still a little unsure? Here’s our firm’s flowchart for deciding whether buying or leasing your next vehicle is right for you.

The Cheapest Way to Own a Car Long-Term

Although the financing terms are important and leasing with a subsequent purchase at residual value could be advantageous, the most straightforward way to save money in the long term is to buy a car and keep it for at least a few years after the financing period ends. Even better, you hold onto it for up to 10 years, after which you’ll need to decide if creating an exit plan is worth it. This will depend on your daily usage and the vehicle’s manufacturer. I recommend that any prospective car buyer review the consumer reports on vehicle reliability and vehicle repair costs.

Hybrid vs Gas vs Electric: Which Is Most Cost-Effective?

Hybrid Break-Even Analysis

While there are clear environmental benefits to choosing a hybrid or electric car, I often hear broad claims that it’s also a cost-effective option. Let’s start with a hybrid vehicle. I actually ran this calculation for myself a few years ago when purchasing a car.

The Inputs:

- Hybrid Surcharge: $3,500

- Annual Mileage: 12,000

- Average Gas Price: $3.25/gallon

- Non-Hybrid Miles Per Gallon: 24

- Hybrid Miles Per Gallon: 35

- Non-Hybrid Annual Gallons Used: 500

- Hybrid Annual Gallons Used: 342

Ultimately, it would cost $1,625 (500 x $3.25) annually to fuel the non-hybrid version of this car compared to $1,112 (24 x $3.25) for the hybrid. The hybrid would save our family $513 each year. Since it costs an extra $3,500 to buy the hybrid, it would take nearly 7 years to break even given those assumptions. While I was hoping the break-even would come a few years earlier, this still felt like a victory for our family because I knew we’d keep this car for over 10 years. Or so I hope to, as I admit I am taking a bit of a gamble since I don’t know much about the inner workings of a hybrid car and its expected shelf life versus its non-hybrid counterpart.

Are Electric Vehicles Worth It Financially?

Before the federal EV tax credit expired, going electric seemed to make a lot of financial sense. Even the leases on EVs were very cheap because dealers passed the tax credit through in order to attract folks to make the switch. Since we were buying a vehicle to be our primary family car, an electric vehicle wasn’t an option for us. For hurricane evacuation, we needed a vehicle capable of transporting multiple kids and dogs through traffic that could be at a standstill for hundreds of miles, without the worry of not knowing where the next charging station would be.

But for a secondary vehicle just to get around New Orleans by car, I’d be surprised if I bought anything that runs on gas. Admittedly, I don’t know much about lithium-ion batteries or this technology, but the idea that I could have a car for 10-15 years with very little maintenance and no time wasted at the gas station seems luxurious. If the federal tax credit is reinstated in the future, or if your state offers its own, it’s definitely worth exploring. Unfortunately, there isn’t a universal answer because the same factors still apply to your intended use, expected maintenance, and price differences.

Is the “Buy Used” Strategy Still Worth It?

Here’s what the advice USED to be: buy a certified pre-owned car that is 1 -3 years old.

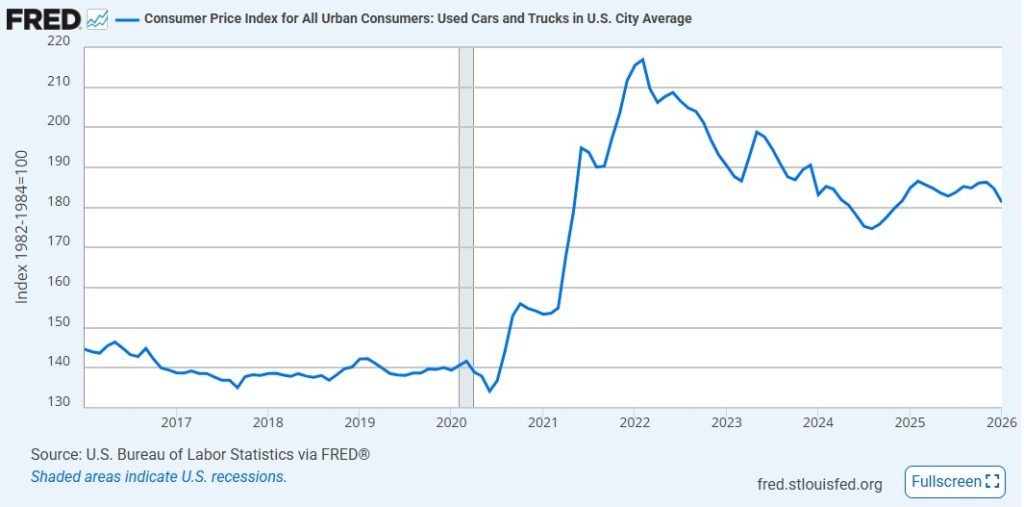

Rationale: Cars depreciate faster during those first few years, and you still have significant useful life left in the vehicle. See the chart below for why this is now a little more complicated.

Used car prices jumped 56% due to supply shortages that began during COVID-19. While they’ve come down in recent years, they’ve only decreased 16% from their post-COVID highs. In comparison, new vehicles *only* spiked 22% post-COVID, though prices have remained relatively flat since.

Certainly, this might still make a lot of sense, but you’re getting less value for your money with a car that usually has a shorter warranty and fewer years of useful life. The further you get away from a car being brand new, the more risk you assume in its remaining useful life.

Eddy Jurgielewicz, a partner and lead financial planner at Upbeat Wealth, has done most of his car shopping outside of dealerships. He filters online marketplaces for used, single-owner cars with no major accident history and few recalls. Yes, he would even target makes, models, and years that appeared to have few maintenance issues. But that was a kidless Eddy living in New Orleans, where owning a car was more for convenience than a requirement. I would be surprised if he used this strategy with a child while residing in Los Angeles for a primary family vehicle.

While buying used no longer seems like a slam-dunk strategy, there is still an opportunity to get a great deal. We know that the profit margins on used cars are usually higher for dealerships. And if you have the ability to negotiate in the private market, there’s definitely value in cutting out the middleman. Either way, that gives you a better chance to negotiate a price reduction. For some, this is worthwhile; for others, it may cause unnecessary stress.

How Leasing Can Actually Make You Money

The manufacturer sets a residual value for the car, which is your guaranteed price to buy it at the end of the lease. There’s always a chance that your residual value is less than the car’s fair market price (the price you could otherwise sell the car at), and you might have built equity unknowingly. Of course, you need the cash available to buy it, but if you do, it could work out in your favor. Think about everyone who leased a car before the huge rise in used car prices following COVID. Cars didn’t depreciate as much as manufacturers expected and had included in the leases because supply and demand dynamics changed dramatically. This created an opportunity for our family when we went to swap out car. We had a leased vehicle with a $17,000 residual value. However, the Kelly Blue Book Fair Market Value was $23,000. We bought our car for cash with no intention of keeping it. In fact, we traded it in a few days later to a dealership as a down payment for our next vehicle.

Downpayments and Financing

How much money is considered a sufficient down payment? A couple of different levels to this question.

- If you know you want to buy a car, you should aim for at least a 20% down payment, whether that is cash, the trade-in value of a prior vehicle, or a combination of both.

- HOWEVER, if you are in a strong financial position and could purchase the vehicle outright, that doesn’t mean you SHOULD put 20% down or pay in full.

Here’s the rationale. A 20% down payment keeps your monthly payment manageable. If you haven’t been saving toward the purchase of a car to begin with, you might struggle to pay off the increased monthly payment that comes with putting less than 20% down.

On the flip side, if you could just pay off the car anyway or aren’t worried about the monthly payment, then the interest rate dictates how much you should finance.

- 0 – 3%: You could make more money in a High-Yield Savings Account, so finance as much as possible.

- 4 – 6%: Maybe your money can beat this in the market; maybe not. Use a hybrid approach and put down at least 20%, probably more. Consider prepaying as well, assuming no penalties.

- 7%+: Finance as little of it as possible. Assuming you have cash reserves beyond this, the flexibility of holding cash isn’t as valuable to you.

Thinking about the financing term isn’t much different. Great rate? Finance for a longer period. Meh rate? Ideally finance as close to 36 months as possible. Terrible rate? Finance for a maximum of 36 months. And usually, the interest rate incentives/deals are tied to specific term periods. As another general rule of thumb, we find that households with annual debt exceeding 33% of gross income (mortgage, student loans, auto loans, personal loans) tend to feel a little strapped for everything else.

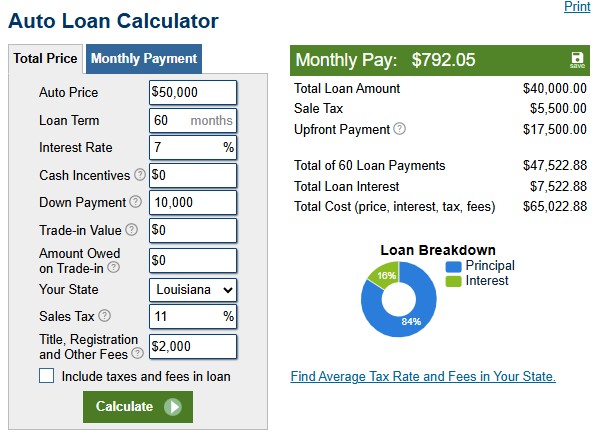

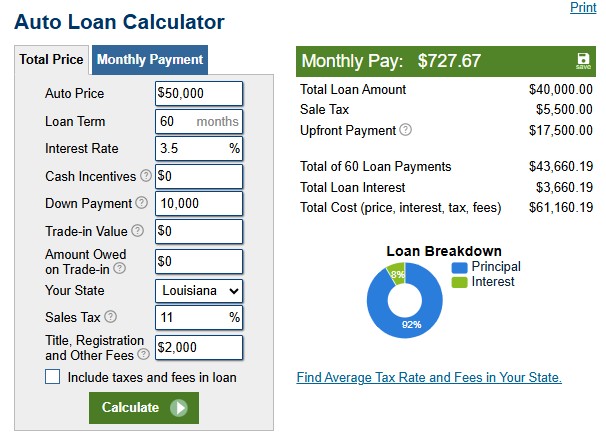

Financing MATTERS, especially with current interest rates. Here’s a comparison of the real cost of financing cars with identical prices but different interest rates.

In this example, an interest rate of 7% versus 3.5% increases your car’s purchase price by 8%. And that’s not including rolling in the sales tax, title, registration, and other fees into the loan.

Smart Car Shopping Tips to Save Money

Shopping for a car isn’t enjoyable, especially when you desperately need one and feel trapped. For example, if your car is in the shop and you’re on a tight deadline to find a replacement. So our best advice for shopping for a car is to do so before you become a captive audience. This will help you establish a reference point for negotiation. Here’s our recommended framework.

- Begin filtering cars by preferred size and reliability metrics.

- Search online for any promotional purchase, leasing, and/or financing rates for these makes and models.

- Check for any upcoming seasonal promotional events offered by these manufacturers.

- Check when new models are usually released. This might lead to a better deal on last year’s model overnight.

- Review inventory online at local dealerships, but also on sites like CarMax and Carvana.

- Create a separate email to prevent spam in the future for your primary email and start inquiring about certain cars. This initiates the negotiation before you walk through the door.

- Treat buying a car and trading in your car as separate deals. I prefer to negotiate the price of the new car first. Afterwards, you can discuss what I want to get for a trade-in.

- Use sites like Carvana to get an automatic “buy it now” price for your current car and also check the Kelly Blue Book value. This provides some leverage to keep a dealer honest on the trade-in value.

- Don’t let a salesperson reduce your car-buying process to a question of “how much do you want to pay monthly?” You’re after the best price, period! Over a long enough financing period, they can meet any monthly payment. That doesn’t mean it’s financially worth it to you. Focus on the total cost of the car.

- A final reminder: the more leverage you have, the better off you’ll be. The less you *need* to do something, the more wiggle room you’ll find.

Frequently Asked Questions About Shopping For Cars

Q1: Should I buy or lease a car?

You should buy a car if you plan to keep it for more than 5–6 years, drive high mileage, or want to minimize long-term costs. Leasing may be better if you prefer lower monthly payments, drive fewer miles, and like upgrading vehicles every few years.

Q2: Is leasing a car ever a good financial decision?

Yes, leasing can make sense if the residual value is lower than the car’s market value at lease-end, or if you prioritize cash flow and flexibility over long-term savings.

Q3: What is the cheapest way to own a car long-term?

The cheapest strategy is to buy a reliable car and keep it for several years after the loan is paid off. This avoids ongoing payments while minimizing depreciation costs.

Q4: How much should I put down on a car?

A 20% down payment is a common guideline to keep payments manageable. However, if interest rates are low (0–3%), it may make more sense to finance more and keep your cash invested or in savings.

Q5: Is buying a used car still a good strategy?

It can be, but the advantage has narrowed due to higher used car prices post-COVID. Buyers should carefully evaluate price differences, warranty coverage, and expected lifespan.

Q6: What is the biggest mistake when buying a car?

Focusing only on the monthly payment instead of the total cost of the car. Dealers can adjust loan terms to hit almost any monthly payment, often increasing the total cost significantly.

Mike Turi, CFP® APMA™ is the Founder and a Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.