Navigating Employer-Sponsored Health Insurance When Pregnant

It’s hard enough to go through open enrollment and choose your health insurance when it’s just you. Now add a life event into the mix, and the extra consideration can drive you crazy. Marriage can be challenging because it involves another stakeholder who may have their own benefits, requiring teamwork and coordination. That’s just the tip of the iceberg when it comes to the most complicated life event, pregnancy.

How will you decide which insurance and benefits are best for you and your growing family? There’s the prenatal care, labor and delivery, and then using the insurance for routine check-ups until the next open enrollment. And with a baby, nothing will feel routine. In this blog, we will help define key health insurance terms, evaluate different coverage options, and provide a checklist for next steps. And for a little precursor, not just focused on pregnancy, you can review Eddy’s original piece on the importance of open enrollment season, here!

Where You Can Buy Health Insurance

Generally, you face the same range of choices as when you weren’t pregnant. Now, though, you’re just evaluating the Family Coverage columns (and costs) of those same avenues. The starkest difference may be in states where Medicaid isn’t extended to individuals who meet the income-eligibility requirements unless they belong to a protected class, such as being a minor or pregnant. There’s also, of course, the Health Insurance Marketplace at Healthcare.gov, which everyone is eligible for. However, there are eligibility requirements to qualify for the subsidies. For the Health Insurance Marketplace, open enrollment is November 1 to January 15th. However, you have to enroll by December 15th to have in-force coverage on January 1st.

For our purposes, we’ll focus on those with employer-sponsored health insurance, which applies to about 60% of people under age 65. It’s important to understand that not all employer health insurance options and benefit packages are the same. While larger, publicly traded companies tend to share certain traits, the options provided by small- to medium-sized employers vary significantly. As does the support available to help you make the best choice, sadly.

Defining Key Health Insurance Terms

Here are the most basic terms to review when determining health insurance.

Premium Cost: Monthly payments to keep the plan in-force

Deductible: Amount you pay before insurance kicks in

Coinsurance: Percentage share of costs you are responsible for after your deductible and before your out-of-pocket maximum

Out-of-Pocket Max: Maximum amount you pay before insurance covers the rest

Coverage Amounts: Certain expenses, like prenatal visits, can be fully covered

Flexibility of In-Network Care: Are your doctors covered?

Using These Terms to Answer the Most Important Questions

There are many acronyms when comparing different types of coverage, but ultimately, you want to know:

- How much does the plan cost?

- What does it cover?

- Which healthcare organizations or doctors are included (in-network)?

One of the best ways to answer these questions is by looking at your Summary of Benefits and Coverage. This 2-5 page document gives a brief overview of what’s covered and provides examples of how costs are shared in specific situations, like pregnancy. If your employer doesn’t give you this document during open enrollment for each medical plan option, you can probably ask for it. The good news is that the examples are quite similar across different insurance companies. Here’s an example document:

How to Best Gather More Information About Your Health Insurance Options

While the examples above may be similar, the plans themselves won’t be. There are a lot of them, and the cost passed on to the employee is determined mainly by how much your employer contributes. So if you find yourself in a deep Reddit hole on the subject, please know that what works for one doesn’t necessarily work for all.

The best thing you can do around open enrollment is schedule a meeting with your company’s benefits manager, as well as make a call to a rep from the health insurance plan. To get specific information, you unfortunately do have to set aside time to contact the people who understand the plan details best. You’ll want to get the best estimate of the associated costs from start to finish and understand whether any alternative birthing methods or extra services are covered if that is a consideration for you.

The Biggest Challenge: Lack of Pricing Transparency

A challenge, because no one is really going to be able to *tell* you exactly what something will cost. Standard prenatal care visits will be easy to assign a cost to in advance. But most people hit the grey area rather quickly on items like ultrasounds, genetic testing, and non-routine visits. So, you’ll want to know where the insurance company draws the line between medically necessary and *voluntary*.

Beyond how an insurance company perceives the medical guidance you need, they also won’t know how much it will actually cost. Which, unfortunately, does make some sense. Your doctor hasn’t provided services to you or billed for them yet. Since every pregnancy is different, your doctor isn’t exactly sure what those services will be either. Covering expenses and medications under co-pays or your deductible is fairly straightforward. However, a significant portion of your costs could be determined by a coinsurance provision. As explained earlier, coinsurance is usually about 20%, meaning you pay 20% of the cost for certain services. The cost itself has two (2) layers do it.

The amount billed by your healthcare provider.

The negotiated rate between your healthcare provider and your insurance company.

Here’s a normal Labor & Delivery example. Your healthcare provider *bills* your insurance company $36,000. The insurance company has a pre-negotiated rate behind the scenes for how much they’ll actually pay your healthcare provider, which lowers the cost to $9,000. Let’s say you had $2,000 left on your deductible and aren’t close to your Out-Of-Pocket-Max. Using a 20% coinsurance, your final bill would be the remaining deductible ($2,000) plus the coinsurance ($1,400), for a total of $3,400. That’s a far departure from the $36,000 that your healthcare provider *billed* your insurance company for.

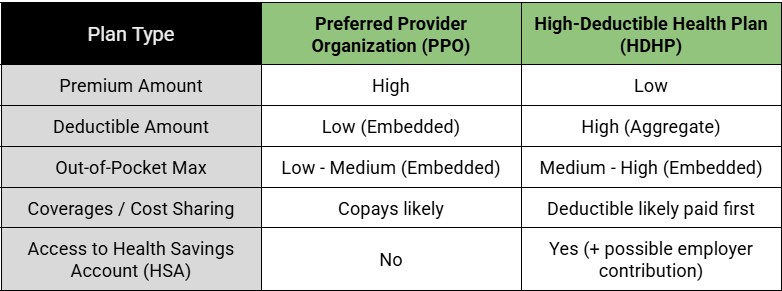

PPO vs. HDHP: The Most Common Health Plan Decision

The most common decision is between a high-premium/low-deductible plan, usually a Preferred Provider Organization (PPO) plan, and a low-premium High-Deductible Health Plan (HDHP). Here are some general characteristics:

Please consider that prenatal care guidelines are very inconsistent. It’s common for plans to provide this coverage for free or with a lower co-pay than usually expected. I’ve seen many High-Deductible Health Plans that include generous prenatal benefits.

Aggregate vs. Embedded Deductibles and Out-of-Pocket Maxs.

As noted above, PPOs generally have embedded deductibles, while HDHPs have aggregate or non-embedded ones. Usually, the out-of-pocket maximum is always embedded. Embedded and aggregate refer to how each family member’s medical expenses count toward the limit. Here’s a definition and example of when each could be beneficial for you.

Aggregate Deductible: Usually, it’s a higher deductible amount that your entire family must meet before copays or coinsurance start. This arrangement works better when medical expenses are lower and shared evenly among covered family members, as they may not have met their individual deductibles otherwise.

Embedded Deductible: Usually, a lower deductible amount that can be met by just one covered family member before copays and coinsurance apply for everyone. This tends to work better when only one family member faces high medical bills because it helps you meet the deductible faster for everyone on the plan.

Embedded Out-of-Pocket Max: Generally, all plans have embedded out-of-pocket maximums, including individual limits and a family limit. Each family member will stop paying medical expenses once they reach their individual limit. Additionally, if multiple family members have expenses but haven’t yet reached their individual limits, and their combined expenses reach the family maximum, then no further payments for medical expenses are required. If there is an Aggregate Out-of-Pocket Max, which there may be, but I have never seen it, then there would be no individual limits, only a family limit that must be met by any combination of family members.

Differentiating Expenses Between Mom/Baby & Actually Paying For Them

We performed a simple labor and delivery calculation earlier in this article, but it was simplified for illustrative purposes regarding the lack of transparency in pricing. It goes even further. Who are these expenses even billed to? Until delivery, everything was billed to the expectant mother, but now there’s another person involved. That little person crying nonstop in the corner has its own individual deductible and out-of-pocket maximum. Depending on if they are embedded or aggregate, they’ll start incurring their whole new set of costs. But when does that occur? Bad news, it’s not entirely clear! Although this is worth inquiring about with your prospective health insurance company.

Generally, many of the charges for newborns within the first 48 hours are bundled and covered under the mother’s insurance and billed accordingly. However, if you have specific pediatric needs or the baby requires ICU care, that will be covered under the baby’s insurance. However, as stated, how those expenses get itemized between the mom and the baby isn’t an exact science.

Negotiating Your Bill and Payment Plans

Negotiating your final bill is an option, as it may save you money, but it can be a morally ambiguous decision. Of course, feel free to fight anything tooth and nail with your actual health insurance company. There’s nothing to be ashamed of there. However, when it comes to negotiating with your healthcare provider, the reality is that our system is imperfect, and in an oversimplified view, most issues stem from how insurance companies operate rather than how healthcare providers bill for their services. And the providers are often left with the bill if or when patients cannot make the payment. As a strategy, your healthcare provider may be willing to reduce your bill if you wait 60 days or more, because, unfortunately, if they send you to collections, they will only receive about 33% of that money anyway. So that’s always a phone call you can make.

Healthcare providers also recognize this, so most now offer generous payment plans to avoid the need for negotiation entirely. Although lowering your bill is still preferable, taking advantage of a 0% interest payment plan, if available, isn’t necessarily a bad next step. It remains a good idea even if you can afford to pay everything upfront, as the money could continue earning interest in a high-yield checking account and thereby effectively lowering the amount of money spent.

Qualifying Life Event

An important reminder not to miss your window to add your newborn to your health insurance plan. This must be done after the birth with a copy of the birth certificate. Most plans give you 30 days to do so, so set reminders accordingly before the sleep deprivation kicks in.

Another important point is that not all employers let you change your health insurance plan during a Qualifying Life Event like your child’s birth. You may only be able to add your child to your current plan, making open enrollment from the previous year very important. Even if you can change your health insurance plan, tread carefully. It’s not guaranteed that your current expenditures will automatically roll over to the new plan. Therefore, you might have to start from $0 toward your deductible or out-of-pocket maximum. If they do rollover, make sure you understand how that process works and when the new effective date begins so there are no gaps in coverage or surprises.

Our Preparation Checklist

Have a phone call with the person responsible for your company’s benefits. That could be an internal benefits manager in HR or an external benefits consultant from the firm your company partners with to provide the benefit options for employees. They can hopefully filter through the plans to determine a select few that could make sense and break down the pros and cons.

Review the Summary of Benefits and Coverage document for each plan to understand how pregnancy is covered. This will help you better grasp how deductibles, cost-sharing, and out-of-pocket maximums apply.

Confirm that your preferred healthcare providers are in-network.

Contact a family ambassador or representative from the health insurance company itself to get their expertise on navigating that plan during pregnancy. This is made easier if you’re reviewing different tiers of plans from the same insurance company. Make sure to ask about how prenatal care is covered throughout and roleplay any special circumstances or alternative care not included under routine procedures.

Understand your worst-case scenario by adding your premium to your out-of-pocket maximum. For HDHP, understand how a Health Savings Account affects your bottom line through employer contributions and tax deductions. It’s common for employers to contribute $1,000 voluntarily to an HSA, which can be used to offset your healthcare expenses. Or a great way to invest. Here’s an earlier blog by Eddy on maximizing your HSA. Most importantly, don’t just assume a PPO is a better option. If the out-of-pocket maximums are similar and you expect to reach them anyway, the extra premium for the PPO plan might end up costing you more.

Switching plans using your Qualifying Life Event may make sense, but you want to be really clear on whether your employer actually allows you to do so, if the progress toward the deductible and out-of-pocket maximums will rollover, and what would be billed to the old plan versus the new one. Examples of when this MAY make sense. You’re on a PPO plan with an early-year birth and end up exceeding your out-of-pocket max, or have a relatively straightforward birth. It may be worthwhile to switch to an HDHP for the remainder of the year if the premium savings are substantial enough. Or perhaps you are on an HDHP, and your child requires significant post-delivery care; it MAY make sense to switch to a more expensive PPO plan if you’ll hit the out-of-pocket max much sooner.

Once you have the baby, use your Qualifying Life Event to add them to your health insurance within 30 days. Understand that delaying this doesn’t delay what gets billed to you or what gets billed to them. Charges will be itemized according to the billing codes provided by your healthcare provider and will be applied retroactively to your child even before they are added to your insurance.

Review your bill for accuracy and don’t be afraid to ask a question if you don’t recall receiving a service listed there. Wait at least 60 days before making a payment or negotiating, if you choose to do so. Check if there’s a 0% or low-interest payment plan that works in your favor. Do not pay anything before it has a chance to go through insurance.

Most importantly, enjoy!

Mike Turi, CFP® APMA™ is the Founder and a Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.