The Key Financial Planning Decisions We Made When Expecting

Are you planning to grow your family, or already expecting the newest addition? If so, I hope this post serves as a helpful tool for navigating the mostly financial (and some not-so-financial) baby preparation checklist.

I’ll break down exactly what my wife and I did by trimester, but keep in mind that your situation might mean doing things differently.

A general word of advice...

If you have a partner through this journey, work together as a team as much as possible. Communicate. Give yourselves grace. Key into when one of you may need to step up and take the lead on a task, so the other can step back and focus on themselves.

Before I give context to each step, here’s the overview of exactly what we did:

First Trimester

- Chose a provider and where we wanted to give birth

- Reviewed our health insurance and the estimated costs of pregnancy + birth

- Looked over our other employee benefits

- Created new savings buckets and cash goals

- Reviewed our monthly household cash flow

- Assessed our life insurance coverage and made necessary increases

- Mapped out a plan for leave

- Began looking into options for childcare and other support

Second Trimester

- Made and shared the registry

- Put the baby’s room together

Third Trimester

- Got our estate plan done

- Made final purchases of baby supplies

Fourth Trimester

- Obtained our baby’s birth certificate and Social Security card

- Added the baby to our health insurance

- Reviewed the hospital bills

- Updated our estate plan

- Opened a 529

- Made a note for the child tax credit

- Took necessary steps to open a Trump Account

While we put some intention behind the order of things, you could certainly switch it up. We also wanted to front-load the pregnancy with these financial tasks to leave space for more unexpected life things that might come up as the pregnancy progressed.

The First Trimester

Choose Your Provider and Where You Want to Give Birth

For us, this was fairly easy. My wife’s sister had recently given birth to her second baby, having had a great experience with her OB-GYN and the hospital. This was enough for my wife to feel comfortable following suit. Still, we needed to confirm that the provider was in-network. Fortunately, she was.

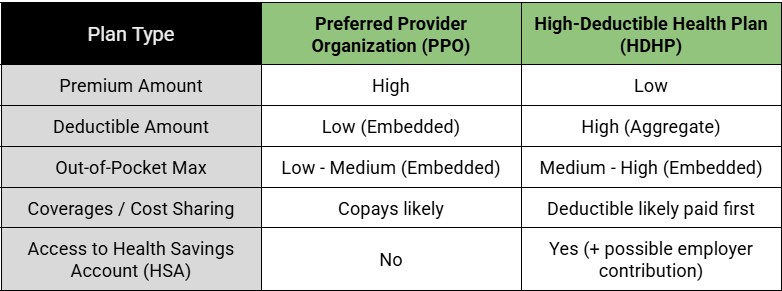

Review Your Health Insurance and Estimated Costs

We knew there would be plenty of surprises to come. If we could help it, we didn’t want the cost of birth to be one of them.

My wife spent a healthy amount of time on the phone with various representatives for our health insurance company, over the course of multiple calls, investigating the specifics of costs and coverages for pregnancy and birth-related care.

To be safe, we made a plan to proactively save an amount equal to our out-of-pocket maximum in a dedicated cash bucket. That way, if we encountered something unexpected, we’d still have the funds available to take care of the bill.

Mike gets into everything you need to know about evaluating health insurance while pregnant in this previous blog post.

Look Over Your Other Employee Benefits

Beyond health insurance, there are some other employee benefits that can be especially valuable when expecting a baby. We sat down to review exactly what else we had access to through my wife’s employer (that’s where our family gets our benefits).

Getting pregnant, while an incredibly fortunate and life-changing milestone, is not a “qualifying life event” that allows you to make changes to your benefits outside of the standard open enrollment. But if you pass through an enrollment window for your job (or even switch jobs, giving you an initial benefits enrollment period) while expecting, this is a great opportunity to make any impactful updates. Otherwise, birth is the next chance you’ll get to make adjustments (more on this below).

Create New Savings Buckets and Cash Goals

Hello, Ally (we love their bucketing system for organizing cash)!

There were 3 new cash buckets we wanted to add to the mix:

- Medical Expenses

- Doula

- Baby Supplies

As I mentioned, we wanted to set aside enough cash to cover our OOPM for a potential “worst case” scenario. That went into the “Medical Expenses” bucket. Once we knew how much a doula would cost, we put money aside here to have ready. Then, we set a target of $2,000 for the “Baby Supplies” bucket to cover up-front costs. The idea was that this would cover things like a stroller, car seat, bassinet, etc… anything we thought we’d need ready for when baby came home (emphasis on thought, because I’m telling you… you just can’t fully know until you’re in it).

A word of advice: Based on your baby and how you choose to operate, you will likely find there are new or different things you need after you bring your little one home. We were quick to pivot on some things, or introduce new gadgets to make our lives any bit more manageable in those first weeks. So leave some cash on hand in the “Baby Supplies” bucket for those early postpartum days. You. Will. Need. It.

Review Your Household Cash Flow

Obviously, a new child doesn’t merely come with a one-time setup cost… there’s ongoing maintenance involved. We wanted to make sure we were managing our expenses in a way that we could absorb the increased month-to-month outflows that a new family member creates. When you get to this point, consider things like how you plan to feed (will you have expenses like bottles and/or formula early on?) and how soon you expect to incorporate paid childcare.

This exercise also helped inform us on how we could meet the up-front cash savings goals mentioned above, since we still had time to build those up.

Assess Your Life Insurance Coverage & Increase if Needed

As your family grows, life insurance cannot be overlooked. The bottom line is this: if someone depends on your ability to earn an income, you need appropriate protection in place.

There’s a reason I include this as an action item in the first trimester. Pregnancy-related health complications, like high blood pressure or gestational diabetes, for which women are at a greater risk in the second and third trimesters, could potentially cause coverage to be denied. In other cases, the insurer may delay the application process until after the baby is born, or they’ll issue a policy with a lower health rating (meaning higher premiums).

In short, your health matters. So it’s especially important for birthing mothers to handle this as early as possible to have the best chance of a policy being issued and earning an optimal health rating. Non-birthing parents shouldn’t delay either. Your age contributes to the premium as well!

Even if you’re planning to stay at home for an extended period of time, your family will benefit from you having coverage too. While you may not be earning a salary during that time, it goes without saying that you do provide a wealth of support. If something were to happen, that benefit could allow the surviving parent to take some time away from work with your child, search for a different job that provides greater flexibility of time, cover the added expenses to keep the household together, and more.

Here’s a previous blog post with a helpful explainer on all things life insurance. And this is a calculator we use with our families to help them determine an appropriate amount of life insurance to put in force.

Map Out a Plan for Leave

Parental leave plays a big role in the finances of a baby. How much do you have? Is it fully paid? Can you tap into a state-paid family leave system? Do you and your partner stagger leave to extend the amount of time before needing additional support or paid childcare?

It’s somewhat of a guessing game, especially this early on, since you can’t know exactly what the due date will be. But we wanted to have a draft plan in place as soon as possible so that we could generally know what to expect in terms of other support and childcare.

Begin to Plan for Childcare and Other Support

Even if you don’t know for certain whether you’ll be fortunate enough to have family support, seek out a nanny, put your child in daycare, or do some combination of these, I recommend learning the cost of everything in your area. It’s very location-dependent! Getting on this as early as possible also helps increase the chances you get into the daycare of your choice, if that’s the direction you go. It’s not crazy for wait lists to be several months.

The Second Trimester

Make and Share the Registry

If you’re like us, you’re lucky enough to have already received a random assortment of hand-me-downs and loaned items at this point. This is about the time we sat down to take inventory of what we’d been given and what we thought we’d still need.

After hours of research and interviewing friends with babies, we built out our registry and began sharing it with family + anyone else who was generous enough to ask for it.

Put the Baby Room Together

It didn’t feel totally real in the first trimester. But my type A-ish personality wouldn’t let us get past the second trimester without getting the baby’s room set up. We learned much more about the supplies and such we’d need as the nursery came along. So taking care of this sooner allowed us to have those realizations with less concern that time was ticking down too quickly.

The Third Trimester

Get Your Estate Plan Done

This had been on my mind since getting married earlier in the year, and a baby on the way was just the motivation I needed to get this across the finish line.

With the help of an online DIY-type estate planning platform, we worked through the big decisions… beneficiaries, guardian roles, powers of attorney, healthcare agents, end-of-life wishes, and so on.

In the end, we drew up the following documents:

- Financial Powers of Attorney

- Health Care Powers of Attorney

- Medical Directives (living wills)

- Wills

We plan to set up a trust as well, which is on our to-do list for the current year…

If you’re looking for a helpful primer on the various estate planning documents and the important roles they play in your family’s life, start by reading this blog post.

Make any Final Purchases

In the final weeks, we filled in any gaps from the registry and hand-me-downs. I have to plug Facebook Marketplace and local “Buy Nothing” groups here. With resources like these, you really don’t have to spend a small fortune on all that baby stuff, unlike what the baby industrial complex might have you believe (unless that’s your thing, which is cool too).

The Fourth Trimester (yes, this is a thing)

Get the Birth Certificate and Social Security Card

After marking the baby, these two documents are a top priority as you navigate those first few dizzying days. In our case, the hospital had a person responsible for grabbing one of us for a few minutes to fill out the necessary forms. They then handled mailing them off to the proper destinations and provided the next steps for us to complete at home. I couldn’t see straight to know if my spelling was correct, so it was a pleasant surprise when the documents came back with our baby’s name spelled the way we wanted.

Add Baby to Your Health Insurance

As I mentioned above, birth is a qualifying life event, so this is the precious window where you want to get your newest family member added to your health insurance. Employers will give you 30 days (or more, in some cases) to get this done.

For us, this meant notifying my wife’s HR department and our insurance company. We had to send in a copy of our daughter’s birth certificate and provide her Social Security number, so it’s helpful to be on top of getting these promptly.

Review the Hospital Bills

This part was anxiety-inducing, even though we’d prepared for the worst-case scenario. Be on the lookout for those bills. And don’t worry, they know how to find you. Review them carefully and know that you have some options. If you feel inclined to do so, negotiating your bill can possibly save you some money. Also, many healthcare providers will offer generous payment plans that could include 0% interest.

Update Your Estate Plan, If Needed

Now that our daughter had been born, there were a couple of things we wanted to adjust in our plan. Don’t let any updates to your plan slip through the cracks!

Open a 529

Since we wanted to get money to work for college quickly, we opened a 529 as soon as our daughter had a Social Security Number. This is all you’ll need to get the account open (on top of the basic stuff like name and address).

Check out Mike’s college savings blog post for a more in-depth look at how we think about planning for education costs.

If you want to be creative and open a 529 sooner… You could start one before your child is even here and designate yourself as the beneficiary (if you don’t already have one). Start funding it whenever you want. Then, after your baby arrives, simply change the beneficiary of the account from you to them. 529s allow for a beneficiary change to a “qualified family member” at any time without taxes or penalty. Your child counts as one such qualifying family member.

Make a Note for the Child Tax Credit

The IRS gives a $2,200 tax credit for each child under age 17. Up to $1,700 of this is refundable. Both of these amounts are the same for tax years 2025 and 2026.

So if you welcomed a new child in 2025, you could get a larger refund (or owe less money) come tax time this year. Moving forward, you can also decide whether or not you want your W4 to reflect the child tax credit.

Including the child tax credit on your W4 generally results in a higher paycheck throughout the year and less, or no refund at tax time (get your money when you earn it). By not notating the credit on your W4, you’ll get a smaller paycheck throughout the year and may get a larger refund.

And don’t forget that other dependents – those aged 17-18, full-time college students ages 19-23, or older dependents – can be claimed for a nonrefundable credit of up to $500 each.

Make a Note or Take Action to Open a Trump Account

Since our daughter was born in 2025, she’s eligible to receive $1,000 from the Treasury Department toward a Trump Account in her name. We don’t plan to add any additional funds, but we’re happy to accept the free money!

To sign up, the IRS has a new document: Form 4547, which you can file with your 2025 tax return, indicating that you’d like an account to be opened. Our CPA included a checkbox on his intake form for our 2025 taxes to make sure this gets included with the return.

There’s also an online portal that should allow for enrollment this coming summer.

Eddy Jurgielewicz, CFP® is a Partner and Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.