In our work with young families, one of the first layers of their financial landscape we assess is life insurance. For most people, there are two ways to put this critical protection in place: through your job’s benefits via group term life insurance and/or on your own with an individual term policy.

Each avenue differs in a handful of ways. There’s often a clear winner in terms of getting the right mix of protection and value. But it may not always be what you expect…

In short, your group term life insurance may not offer enough coverage. And even if it provides the needed death benefit, you may be able to save money by getting a policy elsewhere.

So let’s break it down here.

What is Group Term Life Insurance?

Group term life insurance is coverage that is made available to you through your employer, as part of a benefits package. Further, it’s broken into a couple different flavors: basic and supplemental.

Basic Group Life Insurance

- It comes at no cost to you, since the employer covers the premium.

- It is guaranteed-issue (no health screening).

- Generally, it offers a smaller coverage amount, such as $50k or up to a minimal factor of your salary (like 1.5x salary).

- The premium amount on the first $50k of coverage paid for by your employer is not treated as taxable income to you. However, any premium amount paid for by your employer on a death benefit in excess of $50k is considered taxable income to you, even though you never receive the cash. This is called “imputed income”.

Here are a couple examples of how this coverage is detailed in a benefits packet:

Supplemental (Voluntary) Life Insurance Through the Employer

- You are fully responsible for the premiums on this coverage.

- The coverage may be guaranteed up to a certain coverage amount.

- Additional coverage may be available beyond the guaranteed benefit (up to a stated max) contingent on medical underwriting, though the health screening is often “lighter” than when applying for personal coverage.

- The premium is simply deducted from your paycheck on an after-tax basis.

- The coverage is issued with “group rates”, meaning the cost is based on a large risk pool.

Again, here are a couple examples of how this may appear in a benefits packet:

Is Group Life Insurance Enough Coverage?

Maybe. Probably not.

Mike goes into depth on several key aspects of life insurance in this blog post, covering: how much to get, when to get it, what type to get, and mistakes to avoid, among others. So I’ll quickly hit a few high points here.

For starters, if someone depends on your income, both now and in the future, it’s worth protecting. AKA, you need life insurance. As far as how much is enough, we have this life insurance calculator you can use to arrive at a true coverage need based on your wishes.

As with anything, life insurance is a personal decision, one that depends heavily on your unique situation, goals, and values. Generally, families want to provide coverage for some combination of:

- Income replacement

- Debt

- Education expenses

The right coverage means that your family’s desired lifestyle and future goals continue to be a reality, even in a worst-case scenario. In many cases, group life insurance won’t offer a benefit high enough to provide full coverage.

Is Group Term Life Insurance a Good Value?

Maybe. Sometimes no.

Even if you could get enough coverage through your employer, it still pays to thoroughly examine the cost of that policy.

Life insurance premiums are based on two main factors: your age and health. In some cases, your health may even disqualify you from getting coverage altogether, outside of a guaranteed-issue policy.

If You Have Health Conditions

A major benefit of group life insurance through your employer is that some amount of coverage will be issued on a guaranteed basis, requiring no “evidence of insurability”. For those who wouldn’t otherwise qualify for life insurance, this is significant.

Remember that the “basic” coverage amount will be guaranteed. Then, if supplemental coverage is an option, a portion of that is typically also offered as guaranteed-issue. In the example below, any amount over $700k requires a health screening (evidence of insurability). But that means you could still secure up to $700k in death benefit without answering a single health question.

So if this is your only way to get access to coverage, there’s no way to beat the value of getting something vs. nothing.

If You Are Healthy

Keep in mind that rates for group coverage are based on a large health pool. Essentially, the “average” person. If you’re in good health, it may behoove you to capitalize on that by applying for coverage through a personal policy. There’s a good chance you’d pay less per amount of coverage compared to a group policy through your job, since you’d land a more favorable health rating.

I almost always see this work out in favor of the healthy individual. If that’s you, your group policy may very well NOT be a good value. Look to get the coverage through a personal policy.

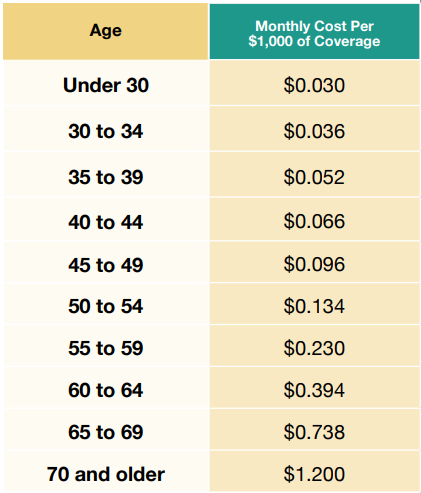

Watch Out for Increasing Premiums

Commonly, the premium for supplemental coverage through an employer will increase over time, based on your age. This could mean a very affordable cost while you’re younger. But that can shift quickly as you get older. Check out an example of this in the screenshot below.

Alternatively, it’s possible to obtain a “level premium” term policy when doing so outside of your employer. This means the cost is set for the duration of the policy. Over the course of 10-30 years, this could mean substantial savings if you qualify for a good health rating with a personal policy, even if the group policy is relatively cheaper at the start.

In short, if you’re healthy, you’ll likely find more value by securing an individual life insurance policy. If you don’t otherwise qualify for coverage, take advantage of all the guaranteed benefit you can through the employer.

Important! If you are going to replace an existing supplemental group policy with an individual one, be sure you’ve paid for and locked in any new outside coverage before dropping the voluntary policy with your job. It’s best to avoid gaps in coverage.

What Happens to Group Life Insurance If You Leave Your Job?

Oftentimes, group coverage is not “portable”. If you separate from your job for any reason, it may not go with you. That’s a big deal, given that life insurance is a major layer of risk protection for your family. We can’t always predict employment separation, since it could include being laid off or fired. It’s not just a planned retirement or quitting. For that reason, we often recommend excluding any employer-based life insurance coverage amount when calculating your need.

If coverage is portable, it will be the supplemental amount (not basic coverage). You need to check with your employer to determine whether or not the policy is portable. Also, know that the rate would likely be different after leaving.

The Complete Group vs. Personal Coverage Comparison Workflow

Here are the steps you should take to navigate this process:

- Take what’s given to you for free through your employer (basic coverage).

- Determine your true coverage need.

- Does someone else depend on your ability to earn an income?

- If so, use this life insurance calculator.

- Compare the cost of getting that coverage between a supplemental group policy vs. an individual policy.

- Once you know how much benefit you need in place, get quotes for an individual policy through an insurance broker.

- Apply for a policy through the carrier that offers you the best rate and complete any underwriting requirements. You’ll never know your actual cost until you receive a health rating from the insurance carrier, which requires a completed application.

- If you are denied coverage, then the guaranteed-issue amount of group supplemental coverage is your only way to get meaningful protection.

- If you receive a low health rating, the supplemental coverage will likely be a better value for you. Then, you’ll need to assess the cost/benefit of paying a relatively higher premium to secure full coverage beyond what the employer policy provides (paying mind to the portability of group coverage).

- If you land a strong health rating, you will most certainly be in a position where putting an individual policy in force makes the most sense, with no need to pay for supplemental group term life.

A Final Note on Shopping for Coverage

When you go searching for life insurance coverage, we recommend using a broker, rather than an agent who represents only one insurance company. This way, you can compare quotes across several different carriers and increase your chances of getting the most competitive rate for a policy.

While we don’t sell any products at Upbeat Wealth, we do walk through this entire process with our families. In doing so, we can be an objective sounding board to ensure the most appropriate coverage for their unique situation is acquired. No decisions are made alone.

Frequently Asked Questions About Group Term vs. Individual Life Insurance

Q1: Is group term life insurance enough coverage?

In most cases, no. Employer-provided group life insurance typically offers limited coverage (often 1–2x salary), which is usually not sufficient to fully replace income, cover debts, and fund long-term goals like education.

Q2: What is the difference between group and individual life insurance?

Group life insurance is provided through an employer and often has limited coverage and flexibility. A portion of it may be fully paid for by the employer (basic), with the option to purchase more coverage (supplemental). Individual life insurance is a personal policy that you own, totally separate from your employer, with customizable coverage and typically level premiums.

Q3: Is supplemental life insurance through an employer worth it?

It depends on your health and alternatives. If you have health conditions, supplemental coverage can be valuable due to a certain benefit amount being guaranteed issue. If you’re healthy, an individual policy is often more cost-effective over the long-term.

Q4: Do you lose group life insurance when you leave your job?

Sometimes. In many cases, group life insurance is not portable. If it is portable, it’s usually only the supplemental portion and the premiums may change after leaving your employer.

Q5: Why is group life insurance sometimes more expensive over time?

Group policies often have increasing premiums based on age, while individual term policies can lock in a level premium for 10–30 years, making them more predictable and often cheaper long term for healthier individuals.

Eddy Jurgielewicz, CFP® is a Partner and Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.