What is the Greatest Risk to My Family or Loved Ones?

For us in New Orleans, we are intimately familiar with homeowners, flood, and auto insurance. Perhaps “intimately familiar with” isn’t the best way to phrase it. Let’s say “tortured by.” Yeah, that’s better. It’s easy to understand the need. If you own a home that would cost $500,000 to rebuild and owe $400,000 on your mortgage, you’ll likely carry homeowners and flood insurance, regardless of how painful the premiums may be. You don’t want to lose your home while still being responsible for your mortgage payments 25 years from now.

You purchased that home because you were confident you would earn enough money to live there until you decided to move on someday.

But what if you lost your ability to earn because of death or disability? If someone relies on your income and that income ceases to exist, your loved ones may lose their sense of autonomy regarding housing, transportation, education, and quality of life. Financial goals and objectives that previously seemed attainable may now appear out of reach.

Here’s the deal: if someone depends on your income, both now and in the future, it’s worth protecting. Please do not leave your ability to financially support your loved ones to chance or a GoFundMe.

And if you’re in your early 20s with no dependents, you likely don’t need to worry about life insurance. It would have to be quite a unique situation otherwise. Therefore, you can tell your friend at—just making up a name—Northwestern Mutual that you’re all set.

Buy Insurance? Surely, There are Other Forms of Risk Protection!

Insurance just feels gross. You pay all this money with the goal of never needing it. So, let’s explore other forms of risk protection to see if there’s an alternative.

Risk Mitigation: Minimize your risk exposure by avoiding it entirely or implementing protective measures. Easy enough! Kid on the way? Maybe leave the motorcycles, helicopters, skydiving, and deep-sea diving to Tom Cruise.

Self-insuring: Personally accepting the financial consequences of a risk occurring. Self-insuring can be effective for everyday risks or those that are relatively minor and low risk. For instance, you might not buy travel insurance every time you fly. Or you might build up, say, an emergency fund to protect against losing your job and a temporary loss of income.

While living a safer, healthier lifestyle sounds great – shit happens. And unfortunately, I’ve participated in far too many of those *shit happened* conversations since starting in this business 14 years ago. You *might* be able to self-insure it, but the odds are low if you’re at the beginning of your career and haven’t had a chance to build up your assets.

Enter Insurance: a Basic Explainer

And here comes the Upbeat Wealth disclaimer: we do NOT sell insurance, so this isn’t a sales pitch. We take pride in our fee-only approach to financial planning, which strives to remove conflicts of interest. This helps us (and you) remain objective, knowing that we are always a fiduciary working in your best interest. This is more of a heart pitch to take care of your loved ones.

Purchasing Insurance: Transferring the financial consequences of a risk to a third party in exchange for premiums paid. Insurance is usually comprised of these four (4) components:

Premium: The amount you pay to keep the policy active, typically on an annual basis.

Coverage: The type of risk you are protecting against.

Benefit: The pool of money left to you or your beneficiaries in the event of a claim.

Term: The duration of time that coverage is provided to the insured.

Term Life Insurance → This is The Way

As you enter your family-building years, Term Life insurance policies are typically affordable, straightforward, and offer substantial benefits to help replace income, which can pay off your family’s mortgage and fund your children’s educational goals.

If you’re seeking financial stability for your household in case you’re no longer around, term life insurance is the primary option to consider. Using the components of insurance above, here’s how that would translate to a Term Life Insurance policy:

Premium: Annual amount required to maintain the policy. Although there are different types of term life insurance policies, the most popular is the “fixed premium” term life policy, meaning your annual premium will stay the same throughout the duration of the policy. According to NerdWallet, the average rate for a 30-year-old woman to obtain a 20-year, $1,000,000 policy is $374 per year.

Coverage: Transferring the risk of your premature death to a third party (the insurance company), effectively protecting your future income that you have not yet earned. Later in this article, we’ll discuss more about choosing a coverage amount.

Benefit: Should you pass away unexpectedly with coverage, your beneficiary(ies) will receive a sum of money equal to the policy’s face value, tax-free!

Term: The policy will provide coverage for a set amount of time as long as you pay the fixed annual premium. In the example of buying a policy because you have young kids, we aim to align the policy term with the birds leaving the nest. There is also no cancellation policy. So if you experience a sudden money event, such as your company stock soaring or selling your business, thereby accumulating significant assets that your family could comfortably draw from, you could stop paying your premiums and allow the policy to lapse.

Calculating Term Life Insurance Coverage is Part Art, Part Science

When calculating suggested coverage amounts and term lengths, we aim to align the timing of when dependents will be out of the home with the necessary amount to protect after-tax earnings, pay off debts, and fund education. While I believe you should think carefully about the amount of coverage you ultimately obtain, this is one area where I wouldn’t let analysis paralysis consume you. Anything is better than nothing.

And while having no earned income and applying for a $5M Term Life Policy may raise some red flags, there generally aren’t many restrictions on the amount of coverage you can reasonably obtain. Therefore, the best answer is to go secure the bag at a number where you sleep well at night. For those seeking a more strategic approach to selecting the ideal policy, here’s how we guide households through the process.

Case Study:

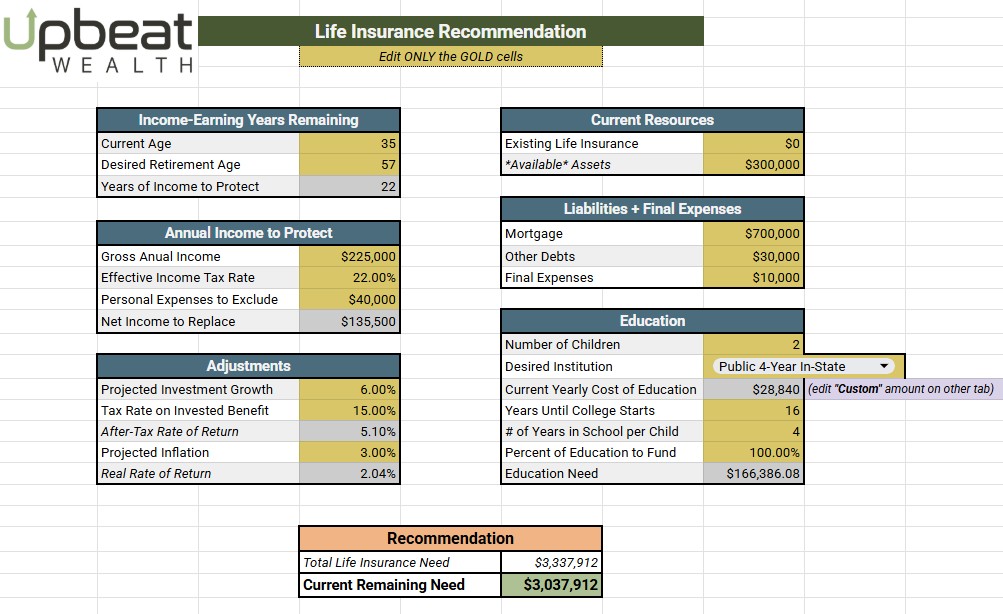

Muses and Thoth are 35 years old, married, and have one child, who is 2 years old, with another on the way this year. They have a household income of $300,000 comprised of Muses ($225,000) and Thoth ($75,000). They recently purchased a $900,000 home and have $700,000 left on their mortgage. In addition to their mortgage, they have a $30,000 car loan. Muses also has $200,000 in Federal Student Loan Debt. Based on their savings rate, they project to achieve work flexibility by Age 57.

In this scenario, if we were reviewing Muses’s Life Insurance Need, we would use the following inputs:

Income-Earning Years Remaining: We aim to protect Muses’s net income for her estimated 22 years of earnings.

Annual Income to Protect: We excluded $40,000 in “personal expenses,” representing the household’s annual savings. The payout from the life insurance policy would effectively replace their need to keep saving. An effective tax rate for a household in Louisiana with an income of $300,000 is approximately 19% federal and 3% state. Since term life insurance benefits are tax-free, we only need to account for the net cash flow to the household rather than the gross amount of income.

Adjustments: While the S&P 500 Index has returned approximately 10% annually over the past century, we will use a more conservative estimate of 6% for projected investment growth. After considering tax drag (taxes on capital gains, dividends, interest) as well as inflation (the rising cost of goods and services), we arrive at a real rate of return of 2%.

Current Resources: Muses has employer-provided life insurance of 1x salary ($225,000) through work. However, we will disregard this. Muses doesn’t expect to stay in this job forever, and this policy is not portable. Therefore, when leaving this position, coverage will no longer be available. However, their household currently has $300,000 in investable assets that would be used to help replace unearned wages due to death. We’ll deduct this amount from their Total Life Insurance Need.

Liabilities + Final Expenses: Canvas ready? Here comes the art of determining your unique needs. Yes, by successfully replacing Muses’s net income, they could reasonably expect to pay off their mortgage according to the original payment schedule. However, Muses expressed, “F that! We just bought this place, and I never want my family to risk losing it.” Muses incorporated this into the death benefit so Thoth could pay off the mortgage and significantly reduce their housing costs. They also decide it’s in their best interest to use the proceeds to pay off the car and cover any funeral expenses.

Education: Muses and Thoth want to intentionally save enough money to cover the tuition costs of a public four-year in-state college. Using the current tuition cost growing at a 6% inflation rate, they have a present educational need of $166,386. Assuming the funds earmarked for college tuition increase by 8% annually, they will satisfy educational goals for both children.

Current Remaining Life Insurance Need (today): $3,037,012.

20-Yr Annual Premium Cost (Preferred Best Health Class): ~$1,200

15-Yr Annual Premium Cost (Preferred Best Health Class): ~$900

From a planner’s perspective, if you’re in good health, that is a small premium to pay to ensure life continues with some semblance of normalcy for your loved ones.

Avoiding Common Life Insurance Mistakes

Don’t rely too heavily on your employer’s group life insurance benefits. Just because you have employer-paid life insurance or access to additional voluntary insurance doesn’t mean you’re fully covered. Group term life insurance policies are typically NOT portable. If your employment status changes, you will lose this coverage. Moreover, your health may change, making qualifying for a preferred rate more difficult than when you were younger and, perhaps, healthier. Securing voluntary coverage through your employer can be beneficial if you have a pre-existing condition that impacts your health class rating, as there is typically a specific amount of voluntary coverage you can obtain without undergoing medical underwriting. However, if you are young and healthy, you will likely pay more for voluntary coverage through your employer than if you purchased a policy privately.

If expecting a baby, do not wait until the third trimester to apply for term life insurance. Even if you are having a low-risk pregnancy, insurance companies may underwrite you differently as you get further along. This can be a costly mistake throughout the duration of a policy that could have been avoided by merely mistiming the application by a few weeks.

While we understand that children are dependents, we shouldn’t overlook aging parents. If you’re part of the sandwich generation, they might also rely on you for care.

Even if one spouse is a stay-at-home parent with no earned income, there is likely still a need for life insurance. Close your eyes and relive the wonder of what single-parenting looks like when your significant other is gone for a weekend. Yeah, you’re probably going to have some additional childcare costs.

Overinsuring yourself, especially if no one is actually relying on your income. If you don’t need life insurance, don’t purchase life insurance. One unique situation where you might still consider it is if you have a hereditary disease that hasn’t taken hold but is known to be passed down in your family. Perhaps you still plan on having dependents one day, and it makes sense to get ahead of something that might be pre-existing.

Another area where I see folks overinsuring is with their kids. Losing a child is an unimaginable tragedy, but they don’t require an insurance policy on their life, especially one that combines insurance with investing. Instead, just invest for them. And in a poor attempt to lighten the mood, feel free to ignore this if your little one is in a deep sports gambling hole with a bookie. Sorry…

And finally – be cautious of sales pitches that seem too good to be true, particularly those that combine insurance coverage with retirement investing. This is an article for another time, but just remember that good products are bought while bad products are sold.

Looking for more risk protection tips? Here’s our risk checklist!

Mike Turi, CFP® APMA™ is the Founder and a Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.