The Simple Framework for 401(k) Contributions

Not to sandbag our version of this question right out of the gate, but this blog/article/education exists on every personal finance resource on the interwebs. Yet, it’s still one of the most common questions that people standing around at a bar, looking for free financial advice clients ask us.

The math is really quite simple. If you’re in a lower tax bracket when making withdrawals in retirement, you’d want to make Pre-Tax Contributions now. If your funds are subject to a higher tax rate later, you’d be thankful you made Roth contributions now. But that’s where the simplicity ends. You might not even know what you’re having for dinner, let alone what life might look like in 40 years. And even if you had that crystal ball, there’s no telling what federal and state tax rates might be. If you’re an actual wizard and do know what the tax brackets will be, there are still scenarios where having access to both Traditional (Pre-Tax) and Roth buckets would be beneficial.

And I won’t bury the lede any further: Here’s a simple way to view the timing of Traditional and Roth contributions.

Early Career: Roth

Mid Career: 50/50 Split

Peak Earning Years: Traditional

But if you want some additional guidance on the full considerations between the two, keep reading!

Because, as mentioned, you are probably somewhat uncertain about:

- Retirement Age

- Reduced Income Prior to Retirement (Back to School, Sabbatical)

- State of Residence

- Expected Federal Tax Brackets

- If You’ll Need a Large Sum of Money Suddenly (Home, Health, Grandkid’s Education)

- Tax Brackets for Your Kids Upon Inheriting Money

- If You’ll Inherit Money and If That Will Be Pre-Tax or Roth

- Needing Health Insurance Before Medicare-eligibility

Explain 401(k) Contributions To Me Like I’m Five

401(k) plans are employer-sponsored retirement accounts that enable employees to contribute through automatic payroll deductions. You might hear a 401(k) called a “Traditional 401(k)” or a “Roth 401(k),” but they are the same employer-sponsored plan. It’s a single 401(k) that accepts two different contribution types. Also, “Traditional” Contributions refer to Pre-Tax Contributions, and these terms can be used interchangeably. Some 401(k) plans even offer a third type of 401(k) contribution known as After-Tax Contributions, which should not be confused with Roth contributions. We’ll skip the After-Tax Contribution bucket for the purposes of this blog.

Understanding How 401(k) Contributions Are Taxed

The key difference between Traditional and Roth contributions is the timing of taxation.

Traditional 401(k) Contributions: Defer tax now, pay taxes later

Roth 401(k) Contributions: Pay tax now, withdraw tax-free later

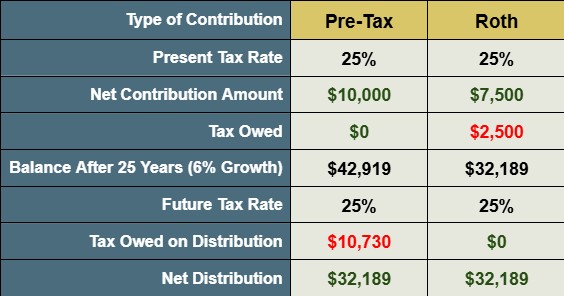

A popular metaphor is “the seed vs. the harvest.” The seed is taxed when you make Roth Contributions. The harvest is taxed when you make Traditional or Pre-Tax Contributions. Mathematically, if you’re subject to the same tax rate on contributions and withdrawals, it doesn’t matter whether you’re taxed today (the seed) or in the future (the harvest).

An example:

When the tax rate is flat, the math – maths. Even though you paid more in cumulative taxes by deferring them, your net distribution remains unchanged.

Won’t My Tax Rate Always Be Lower In Retirement?

“I’m not making any money, so why would I be paying more in taxes?” right? RIGHT!? It certainly makes sense, but it’s not that straightforward. Here are some reasons you might end up subject to a higher tax rate or face higher costs later on, even without any earnings.

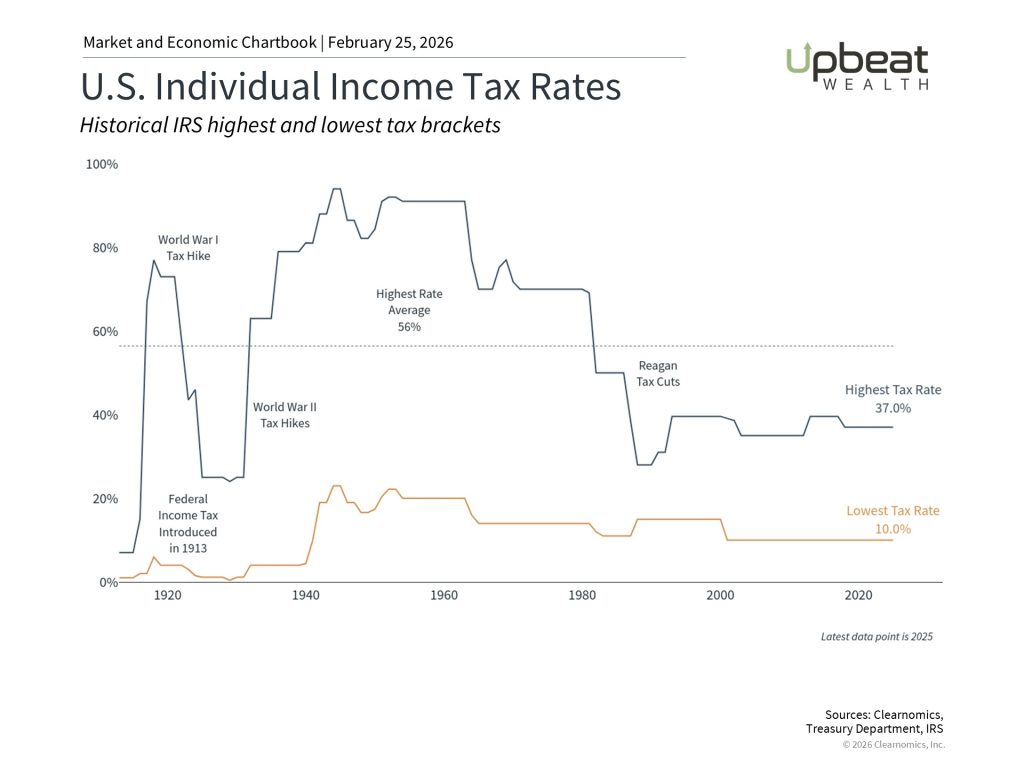

Future Federal Marginal Tax Rates and Brackets

When it comes to future tax rates, we are purely speculating. Here is a chart of the historical highest and lowest marginal tax rates since its inception.

And this chart doesn’t even fully capture how difficult it is to predict how future rates may move across different income levels. The highest marginal rate may apply to only a small number of taxpayers. More specifically, it will come down to how each income threshold is taxed at what rate and where you will fall in comparison. However, if you were to speculate that our low maximum marginal tax rate, combined with increasing national debt, might result in higher future tax rates, I certainly wouldn’t stop you! But note that’s been a popular thesis for decades, and current tax rates have actually decreased relative to certain periods.

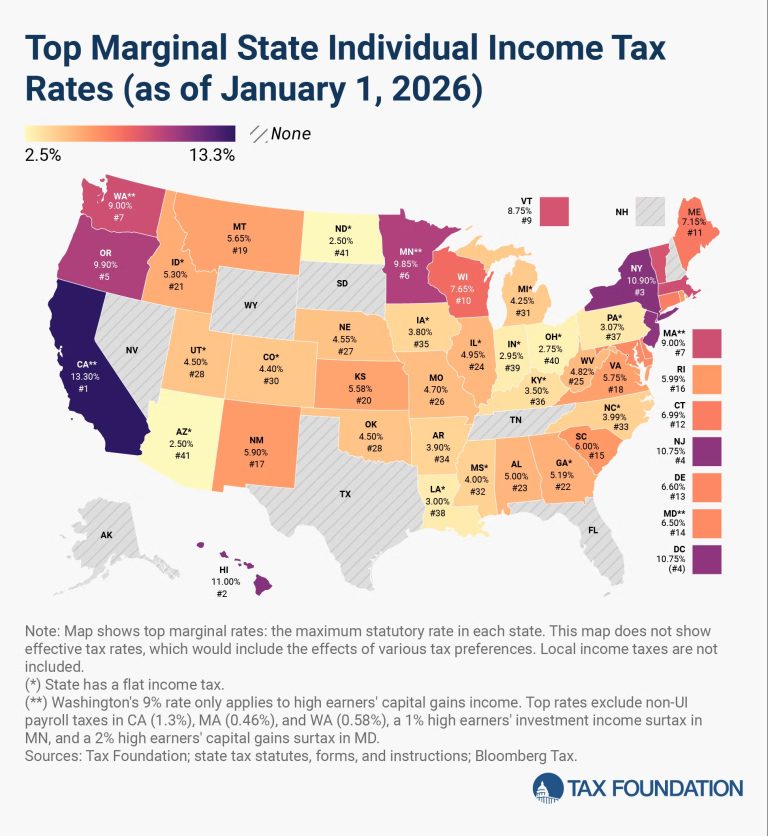

State Tax Rates

The next biggest reason your tax rate may increase is a change in your state of residence. See how your state or desired home in retirement stacks up!

Thinking about retiring in California after working in Louisiana? That’s a big jump in state taxes paid on distributions. Therefore, you might think twice about making traditional contributions today, since you’ll pay a good bit extra at the state level later. But then you might hit your 50s, and your entire personality could be honoring the late, great Jimmy Buffett. So now you’re riding motorcycles and drinking pina coladas (not at the same time, of course!) and eyeing a move to Florida. Well, then you might be kicking yourself a little for not saving pre-tax in Louisiana, since Florida has no income tax.

Obscure Taxes, Penalties, and Costs

Based on current tax rules, there are additional financial *consequences* such as the Net Investment Income Tax (NIIT), the Medicare Income-Related Monthly Adjustment Amount (IRMAA), and how health insurance premiums are determined if you go through the Healthcare.gov exchange without access to an employer-sponsored plan or Medicare and have too much income to qualify for Medicaid. Being forced to make a large amount of pre-tax distributions within a calendar year could result in additional money owed, even if it’s not directly tied to the tax rate on the retirement income itself.

Required Minimum Distributions (RMDs)

Some people are naturally great savers. And if you’re great at saving, you might have a hard time spending money, too. Therefore, you may build a substantial pre-tax nest egg. Based on your birthdate, the government says you must start taking withdrawals from this money between the ages of 70.5 and 75. These mandatory Required Minimum Distributions could exceed what you were earning while working.

You Inherit Money, or Your Kids Inherit Your Money

If you are around my age or most of our clients’ ages, you have boomer parents. And if you have boomer parents, you know they just don’t talk about money. It’s not in their DNA. You’ll get what you get when you get it. But if you are fortunate enough to get *something* and it’s pre-tax money, you’ll have ten (10) years to empty the account to $0. It’s a GOOD problem to have, but it still affects how much you get to keep. There’s a lot of tax planning involved. And if your money is already tied up in 100% pre-tax accounts and the government is forcing you to take distributions, you might find yourself with very little flexibility on what tax rate it’s subject to. You’ll just owe what you owe.

Or, if you are the one saving now and building a 100% pre-tax allocation with the goal of passing money to your own kids, they might actually be fulfilling the American dream of doing better than you! And now you have deferred taxes on money your kids will realize at a higher rate.

That’s A Lot of *Stuff*

That’s not even an all-encompassing list. But it’s worth listing some of the main reasons it’s never as simple as anyone wants to make it. A lot of these things, we just don’t know. And that’s okay! A financial planner can certainly help you address some of these blind spots and make educated guesses/assumptions around tax planning. But if you’re doing it yourself, I’d suggest focusing on what seems best now rather than overthinking every future multiverse scenario.

Emotional Benefits of Roth vs Traditional Contributions

Traditional (Pre-Tax) Contributions Provide CONTROL

I’ll start with pre-tax contributions because I just spent the last couple of minutes of your time making you second-guess whether you should even make pre-tax contributions at all. While we’ll give further financial guidance on when you should consider making pre-tax contributions later in this article, here’s a softer reason. For the most part, you maintain control over your tax consequences. By deferring taxes now, you have control over when you make distributions based on your tax rate at that time. While the government tries to force your hand with RMDs, that may be decades away.

But aren’t there rules and penalties that prevent you from making distributions before Age 59.5? Yes, but you could do what’s known as Roth Conversions. As the name suggests, Roth Conversions allow you to convert Pre-Tax funds to Roth funds beforehand and avoid the 10% early withdrawal penalty. There are a few other considerations and *gotchas* that I won’t go into here, but you should definitely look into them if you’re considering making Roth Conversions. Here’s an educational piece from Schwab that outlines them. I mention Roth Conversions because they are a great tax-planning tool for those who are going back to school, taking a sabbatical, on track for early retirement, or have an opportunity to fill lower tax-rate thresholds before RMDs.

Roth Contributions Provide Peace of Mind

While you lose control over how your money is taxed, the good news is you don’t have to worry about it anymore! Assuming certain holding periods and age thresholds are met, the money in this bucket is 100% unequivocally yours! Taxes have already been paid at the time of contribution, and distributions are not included in your gross income. Therefore, you don’t have to worry about obscure tax laws or rules that tax you more, reduce certain credits, or penalize you as your Adjusted Gross Income or Modified Adjusted Gross Income increases.

Even if you don’t end up with the highest tax-adjusted balance, understanding how much money truly belongs to you can make retirement planning easier.

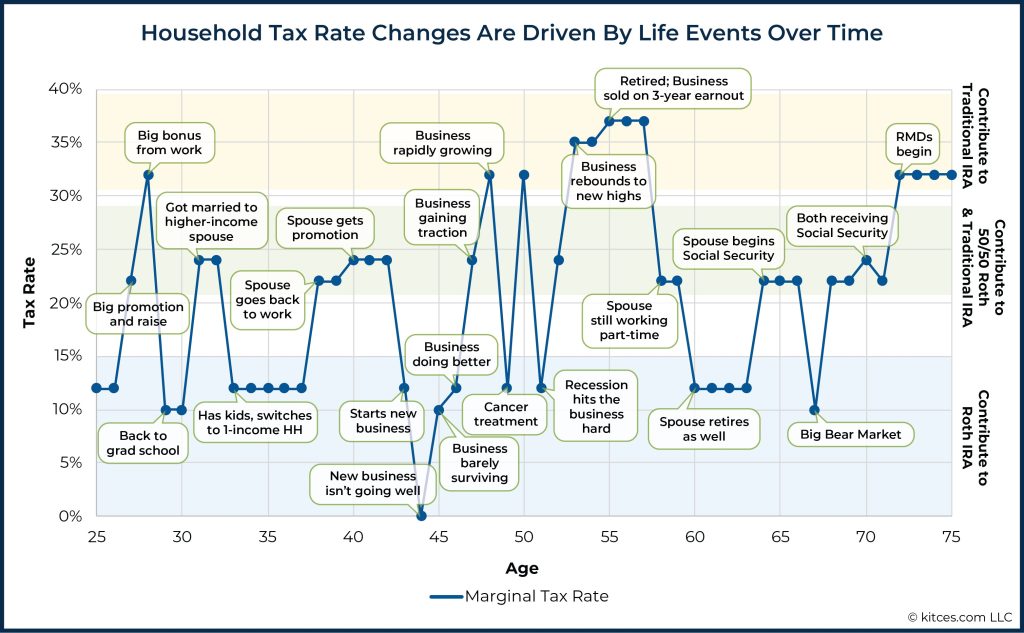

How Life Events Can Influence Contribution Strategy

There isn’t a better graphic to illustrate this than the one in this Kitces.com article, which I’ve included below.

Above, you’ll see reasons you may contribute to a Traditional IRA, split contributions 50/50, or contribute to a Roth IRA, based on life events that affect your tax rate. Here’s the synopsis:

Contributions by Tax Rate

12% or Lower: Roth Contributions

22% – 24%: 50/50 Split

32%+: Pre-Tax Contributions

While the future is important, it’s often more practical to concentrate on today’s events and adjust accordingly. As your life changes, so should your 401(k) contribution method. This approach helps you systematically build your allocations across different tax buckets, offering you maximum control and flexibility when taking distributions before retirement, during retirement, or passing on an inheritance to your family.

Ultimately, a balanced approach to your 401(k) contributions will help you make the most of your funds as you near or enter retirement.

Frequently Asked Questions About 401(k) Contributions

Q1: Should I choose Roth or Traditional 401(k) contributions?

Choose Roth contributions if you expect your tax rate to be higher in retirement. Choose Traditional contributions if you expect your tax rate to be lower later. Many investors benefit from using both to create tax flexibility.

Q2: Is it better to pay taxes now or in retirement?

It depends on your future tax bracket. Paying taxes now (Roth) is better if tax rates rise or your income increases later. Deferring taxes (Traditional) is better if you expect lower income in retirement.

Q3: Can I make both Roth and Traditional 401(k) contributions?

Yes. Most employer plans allow you to split contributions between both types, helping create tax diversification for retirement withdrawals.

Q4: Why should I have both Roth and Traditional retirement savings?

Having both creates flexibility. You can withdraw from different accounts strategically to manage taxes, avoid Medicare premium increases, and reduce required minimum distribution impacts.

Q5: Can Roth conversions help later?

Yes. Roth conversions allow you to move Traditional savings into Roth accounts during low-income years, helping manage taxes before retirement or RMD age.

Mike Turi, CFP® APMA™ is the Founder and a Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.