When Do We Officially Enter a Recession?

Recessions are tough to measure definitively, but as the famous saying goes, you know it when you see it. They are typically defined as two consecutive quarters of negative growth in Gross Domestic Product (GDP), a term used to measure a country’s total output of goods and services. As GDP grows, companies hire to meet demand, productivity increases, and laborers earn more money. As GDP shrinks, we will likely see a spike in unemployment, a decrease in asset values, and a reduction in consumer spending. Let’s face it, though. No one thinks of GDP when considering the threat of a recession. It’s… am I going to lose my job? Will my 401k recover?

Lessons from History on Bear Markets

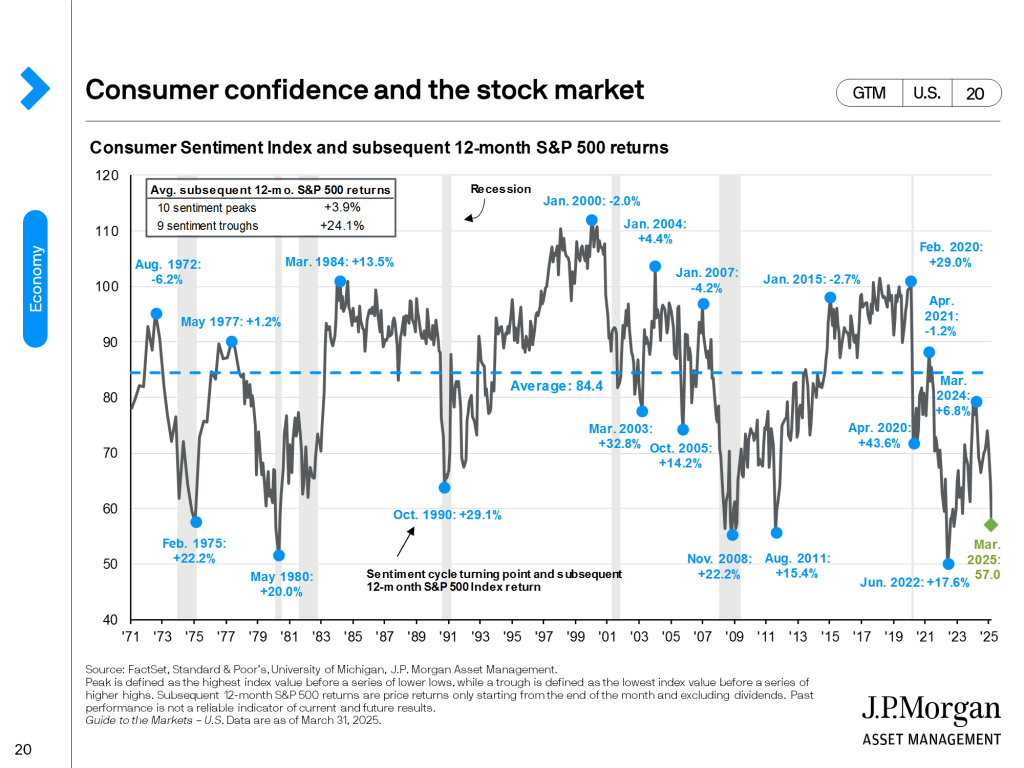

Bear markets (when the market declines by 20%) often coincide with recessions, but accurately timing the market recovery would require a time machine. If this isn’t an impossible task for you, congratulations! You’re the best investor in the world. The challenge, especially for the general public, is that market recoveries historically happen swiftly and at a moment when consumer sentiment is at an all-time low. Here’s a chart from J.P. Morgan showing sentiment cycle lows and subsequent 12-month S&P 500 returns.

You’ll notice the disconnect between present fear and future returns. Things will never have felt worse right before the market pushes higher.

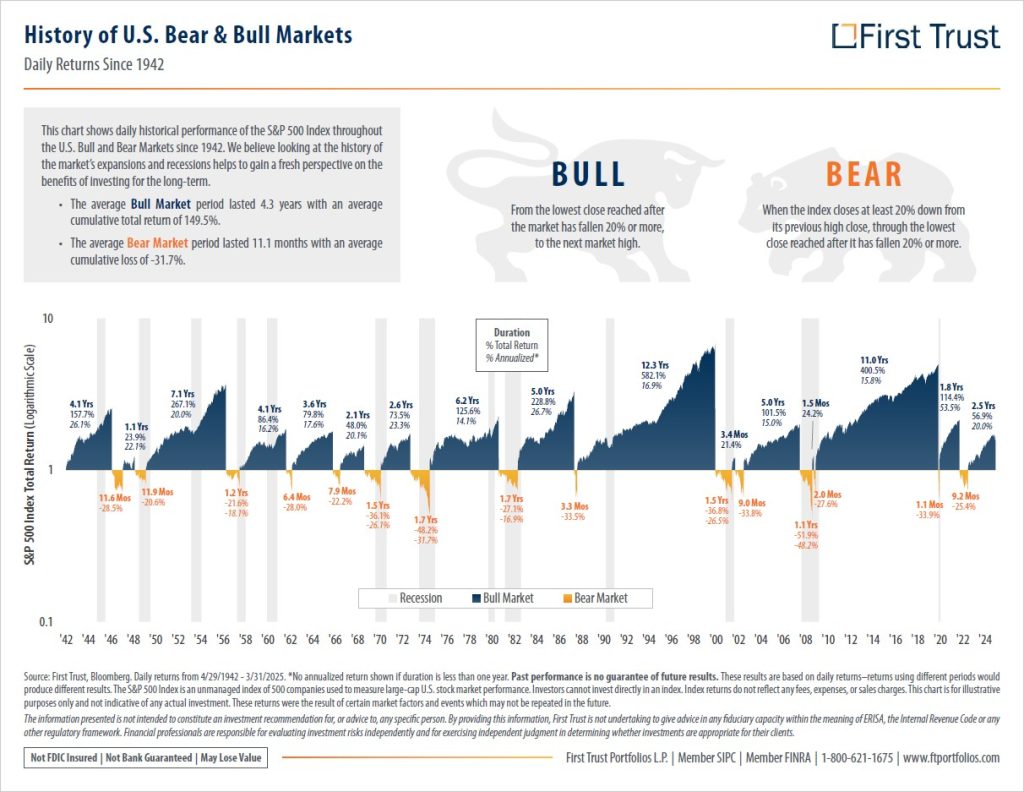

Historical Performances of Bull + Bear Markets

Bear markets are typically measured in months, while bull markets are measured in years. Since 1957, the S&P 500 Index has returned an annualized 10%, yet there are very few years when the return actually fell between 8% and 12%. In fact, across this 67-year period, it has only happened on 7 occasions. Markets tend to have bigger calendar year swings that, historically, have netted out favorably. Here’s a chart presented by First Trust displaying the importance of staying disciplined as a long-term investor.

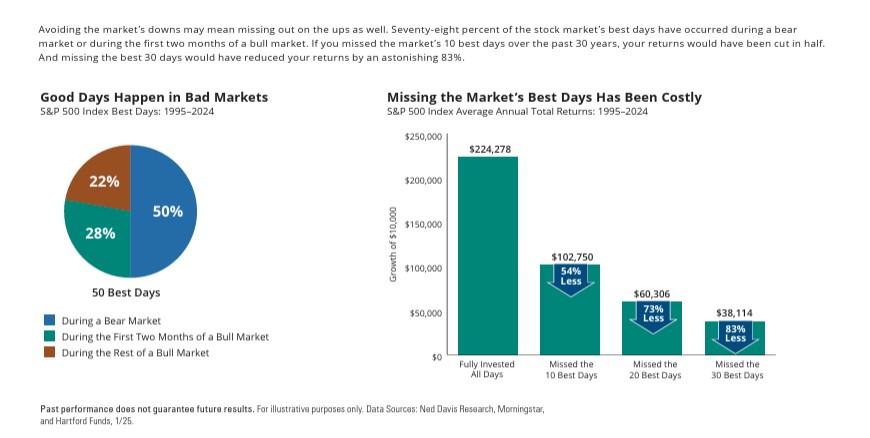

And to beat this point with a stick (iykyk), here’s another illustration showing how costly it would be if you were caught up in the negative consumer sentiment, sold to cash, and ended up missing the best days as the market recovered!

Compared to a portfolio that remained fully invested, if you were caught in cash during the best days for returns, you’d be kicking yourself!

Missed the 10 Best Days → 54% Less Money

Missed the 20 Best Days → 73% Less Money

Missed the 30 Best Days → 83% Less Money

And as noted by the above graphic’s pie chart, these best days are likely to occur during a bear market. While the COVID-19 pandemic initiated an economic shutdown that resulted in GDP decline and peak unemployment in line with the Recession of 1937, the losses in the markets were a blip. If you hadn’t logged into your investment accounts for a couple of months, you would have never known it even happened. So, setting COVID-19 aside, we haven’t seen an extended contraction of the economy since the financial crisis of 2008. This means that we have twenty-somethings who were barely aware, along with individuals in their thirties who lack perspective on the mental toll of watching their portfolio decline. We even have people in their 40s who probably weren’t investors yet themselves and were just starting their careers. That’s a significant portion of the investing population entering their peak earning years without any first-hand experience on how to prepare for a recession.

Prepare for Economic Downturns, But Don’t Panic

If you’re anxious right now, you’re not alone. According to the March results of the Harvard Harris Poll, the two biggest concerns for voters right now are price increases/inflation and the economy/jobs. Inflation continues to be the top issue for voters across party lines. Although we are not currently in a recession, we are nearing the definition of one, along with a bear market. However, we cannot predict what will happen next. We haven’t experienced a global trade war for almost a century. And after an emotionally tolling election and with the 24/7 news cycle, it’s difficult to allow yourself the space to step back from making an emotional decision. But as a local advisor and friend, Jude Boudreaux, would say, respond, don’t react.

Now is a time for focus and introspection. What opportunities do you have to save more or spend less, and what are your household’s biggest threats?

I’m Already Struggling to Make Ends Meet, How Will I Prepare For An Economic Downturn?

Households have two options for saving more money in preparation for a financial crisis:

Reducing Expenses

Earning More

If you are already living paycheck to paycheck with limited discretionary income, the possibility of losing your income or the rapidly rising cost of goods is a frightening prospect. Reducing expenses is already a finite solution, and if you’re living paycheck to paycheck, your ability to do so is severely diminished.

Additionally, if your household’s income comes from a single source, you are at greater risk of needing to withdraw from your savings or rely on credit if the economy experiences a downturn. Income preservation, similar to asset protection, is most effective through diversification. It’s easier said than done, but do you have a path toward increasing or diversifying your income? Can you pivot and further your education on a clearly defined path that leads to career advancement? Can you add extra income to, at the very least, build an emergency fund, perhaps through seasonal employment or gig work? While recessions are undeniably bad, opportunities can emerge. Be realistic about your current situation and how it will project into the future. Don’t be afraid to invest in yourself or leverage your connections toward a brighter future. Nothing worth doing is easy.

Reducing Discretionary Expenses

There’s no time like the present to reevaluate your discretionary spending habits. It’s better to act before a crisis takes hold, but you certainly would not be alone if you delayed this difficult internal evaluation upon reaching an inflection point. As a financial planning note, we hope that you completely avoid being between a rock and a hard place by practicing what we preach regarding cash flow flexibility:

Building a proper Emergency Fund (discussed in the February 2025 Newsletter)

Keeping fixed expenses like home and auto at a conservative percentage of household income, rather than borrowing the maximum a lender permits. (discussed on Great Day Louisiana)

Successfully benchmarking your salary and negotiating a raise (discussed in the March 2025 Newsletter and on Great Day Louisiana)

To quickly reduce spending, here are four key categories to explore for opportunities to make immediate adjustments.

Dining Out: Meal prep at home is always cheaper than dining out and healthier.

Travel: Experiences can add up quickly if you’re not careful.

Impulse Purchases: Create some framework around necessities vs. nice-to-haves.

On-Demand Services: Are you paying a hefty surcharge for convenience services such as same-day shipping, meal delivery, and rideshares?

The Moral Of The Story

As of this writing, we aren’t in a recession or a bear market, and attempting to predict one or how long it will last isn’t worth your energy. I would even go so far as to say that if you have a financial advisor who is making market timing predictions with your money, you may want to reevaluate that service or at least question the methodology of when their crystal ball indicates to reenter the market. Especially considering what you know now about consumer sentiment and diminished returns from missing the best days.

History is a cycle. On a timeline long enough, we wouldn’t be surprised by much. Unfortunately, our moment happens in a blink of the universe’s eye. It’s difficult to stay disciplined when times are uncertain. In today’s world, it’s crucial to uphold your values and what matters to YOU, rather than succumbing to peer influence or the blatant deception found on social media. Life is too short to confine oneself to someone else’s definition of success.

Mike Turi, CFP® APMA™ is the Founder and a Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.