Presidential Elections vs. the Stock Market

New President = New Investment Strategy? Not so fast!

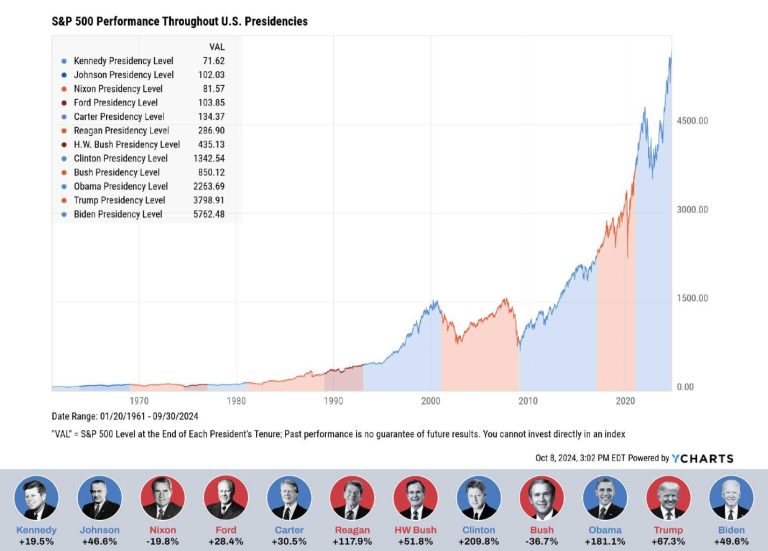

Historically speaking, there is nothing red or blue about the United States stock market. It’s green (see below). Regardless of who is leading the administration, the stock market and your 401k has consistently moved up and to the right.

And look, there are many reasons each election can be conceived as the most important in our lifetime. Indeed, the presidential and congressional election winners affect our geopolitical and economic outlook. Our debt is soaring. Instability is rising across the globe. There’s much work to be done on issues surrounding inequality and human rights at home. However, it pays to zoom out when it comes to the stock market and your 401k + investment portfolios.

Source: YCHARTS

THE Reason Against Changing Your Investment Strategy. Spoiler Alert: It’s Your Money.

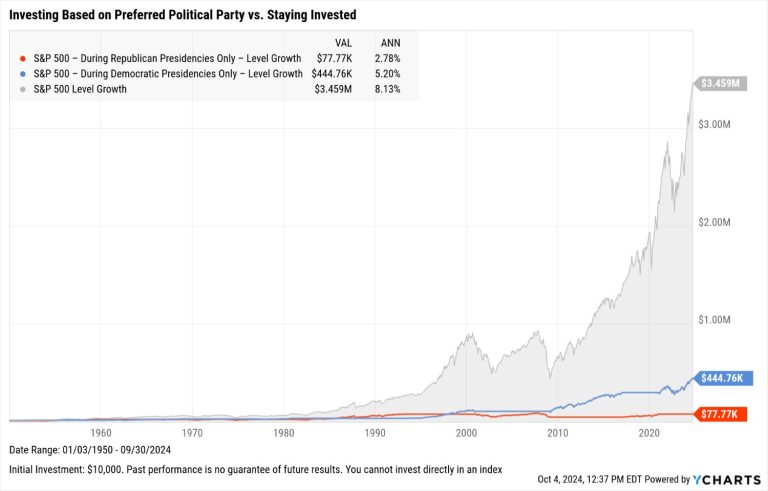

If you had only remained invested when your preferred candidate was in office, you would have missed out on some significant opportunities and cost yourself a fortune. Check out the graphic below created by YCHARTS! Assuming an initial investment of $10,000 starting in January of 1950, here’s how your portfolio would have performed if you had only remained invested under a Democrat or Republican.

- During Democratic Presidencies Only: $444,760

- During Republican Presidencies Only: $77,770

And here comes the big BUT. If you had remained invested regardless of who was in the White House, that $10,000 would have grown to $3.49 Million by September of 2024.

Source: YCHARTS

Allowing your political beliefs to influence your portfolio can lead to disastrous outcomes.

Attempting to time the market is a fool’s errand! Just turn on the TV. No matter if the market is rising or falling, everyone always has an explanation. Although they may act as if they possess one, there is no crystal ball. Not even when it comes to explaining intraday market swings.

Uncertainty is a certainty, which is why I love this Vanguard article and its principle: TUNING OUT THE NOISE NEEDS TO BE YOUR SUPERPOWER.

Now That I’m Thinking About My Portfolio, Are There Any Practical Adjustments I Can Make?

Risk Capacity: Are your investments appropriately aligned with the level of risk you can afford to take? e.g., Do you already have an emergency fund? Could you experience a loss of income, a medical emergency, car trouble, or a home repair without having to withdraw from your investment accounts at an unfavorable time? Depending on the account type, untimely withdraws could lead to penalties and tax issues in addition to loss of principal.

Check out the graphic below compiled by Lincoln Financial Group. From 1976 to 2022, in any given 12-month period, your investment in the S&P 500 (the 500 largest companies in America) may have gained 61.2% at the peak or lost 43.3% at the trough.

Is that a gamble that you want to take if there’s a chance you might need your money in the interim (less than 15 years)? Feel free to check out a quick risk checklist in a previous Upbeat Wealth blog post.

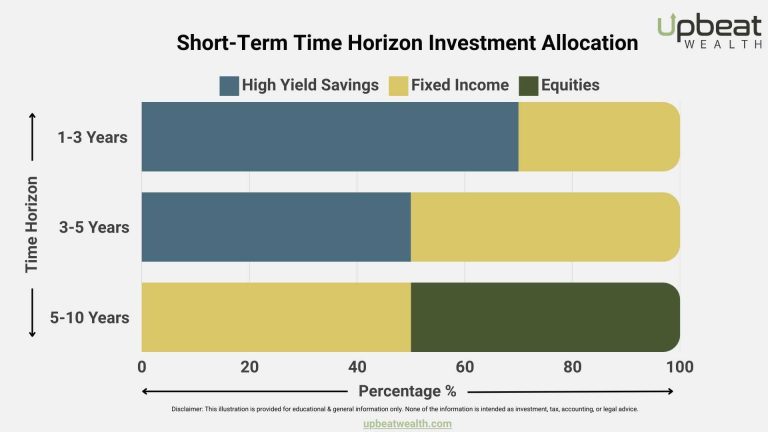

Time Horizon: Have you clearly defined your goals and corresponding timelines to achieve them? Are you properly allocated to maximize risk-adjusted returns based on when you expect to need the money? We often receive questions about investment optimization with condensed time horizons. “I want to buy a home in five years; how should I invest the money?” Well, probably not very aggressively.

Below is our firm’s current general guidance on how to approach short-term time horizon investing, especially given the current high-interest rate environment and the virtually risk-free returns of FDIC-insured high-yield savings accounts and fixed income such as U.S. Treasury bonds, backed by the full faith and credit of the U.S. government.

One strategy we like to implement with our families is to separate taxable investment accounts into different sleeves or buckets. We assist them in identifying their goals and timelines, and we encourage them to create separate accounts for a clearer allocation and visualization of their objectives for those funds.

Managing Costs: Are you invested in low-cost index funds and effectively tax planning around your contribution and investment strategy? I can’t tell you how often I have reviewed household 401(k) investments and seen selections in the highest-fee mutual funds, which seldom beat their respective benchmarks.

Rule of thumb: the fancier the name, the higher the fees. If you see a Yellowstone Dutton Ranch New Pioneers Beth is Aggressively Back on The Booze, Psych – She Never Actually Left Portfolio, RUN for the Vanguard or Fidelity Index Funds if they are there, pleeeeease!

Dollar Cost Averaging: Are you already sitting on a heavy concentration of cash or encountering a sudden money event? Consider investing it over time rather than all at once. While it might not be the mathematically preferred approach, taking this route can help minimize your investment timing risk and serve as a portfolio Ambien when it comes to getting your money a better night’s sleep.

What If This Time is Different?

The U.S. stock market has recently outperformed its average annual returns despite the election, higher interest rates, Russia invading Ukraine, and conflict in the Middle East. When market volatility rears its head, it’s impossible to point to one single factor.

At the beginning of every year, banks and wealth management companies are issuing their annual market forecasts and it’s a whole lot of blah blah blah. Some interesting insights? Maybe. But, ultimately, the themes are indistinguishable and laced with caveats about what the future holds. Because if they knew, they wouldn’t be writing about it. And there are no real consequences because it is all hot air to begin with. Most of the larger well-known wealth management firms conveniently erase their previous year market predictions. Look around, they’re hard to find. That’s because there are no crystal balls, especially during an administration change.

If you make investment decisions solely based on who is in the White House, you might be costing yourself a chance to reach your financial goals. If you’re investing for retirement with 15 years or more ahead of you, embrace a long-term, disciplined strategy. Staying the course now will pay off in the future! It’s important to remember that the market reflects the companies that provide goods and services and drive innovation rather than the actions of any one political party. The only thing we can predict about recessions is that they will occur, but not when. Make sure to have an emergency fund prepared and focus on the things within your control!

“The only president who didn’t complain about the previous administration was George Washington” – like every political speaker or journalist

Mike Turi, CFP® APMA™ is the Founder and a Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.