Why Student Loans Feel So Confusing

Discussing student loans is hard. In my latest Great Day Louisiana TV segment, the host, Malik Mingo, hit me with a “now he’s throwing all the acronyms at us.” I’m not going to lie. It hurt. That’s not who we want to be as a financial planning firm. Our mission is to eliminate the jargon and financial alphabet soup that the suit and tie, corner-office, picture of spouse on a jet ski gatekeepers have historically thrived on, keeping confusion high and their fees higher. We just want to speak to our audience plainly and relatably.

When it comes to student loans, that might just be impossible. Federal student loans were created in 1958 by the Eisenhower administration, and almost every administration since has put its hands on them. Drastic changes have occurred every 4 to 8 years, shaping the modern-day economics of borrowing, seeking forgiveness, and/or repaying. The terms you understood to be true (if you understood them at all) will be different from the ones you’ll need to know when you go to pay them back. And then it will change again, and again, and again. Exhausting! Honestly, it’s like driving somewhere in New Orleans. Just random construction, potholes, street closures, parades, second lines, stray dogs, school zones, and train crossings have you rerouting like the frantic start of every zombie apocalypse movie.

It’s an unfair system for consumers. Put aside what you think about the cost of education, the “dignity” of repayment, or taxpayer-subsidized forgiveness. At the very least, borrowers deserve to understand their options, make informed decisions, avoid being forced to change every few years, and use what was already promised to them when the loans were disbursed.

Instead, borrowers face a system where changes are politically charged and convoluted. The Department of Education and loan servicers themselves can barely keep up and point you in the right direction. Repeatedly, the technology on their websites, which you rely on for accurate information, proves to be false. It leaves borrowers completely scarred. They never want to look at their loans again. Then, there are the interest rates that the government is charging over the life of these loans. As of this publication date, current loan rates for the 2025-26 school year are 6.39% for undergraduates, 7.94% for graduate students, and 8.94% for PLUS loans. These are predatory rates. Far from an “investment” in our future.

So please know you are not alone. Nothing frustrates me more than hearing a friend explain their student loan situation and realizing they’re losing money. The fix is simple, yet they remain stuck in inaction. I conduct seminars for perhaps the smartest people in the city – the doctors at Ochsner (no offense, friends at the bar!). It’s the same situation. So I’m here to try to untangle this once and for all. A glossary to help readers better understand their loans and repayment options.

Financial Aid Terms

FAFSA: The Free Application for Federal Student Aid form is completed annually and determines your eligibility for federal aid, such as grants and loans. The FAFSA opens regularly on October 1st of the year before the award year. The federal deadline for each award year is June 30th (end of the award year). State deadlines tend to be earlier.

Grants: Financial aid provided as a gift that does not need to be repaid. Free money! Grants usually come from limited funds, meaning not everyone who qualifies will receive one. They are often distributed on a first-come, first-serve basis or require very specific eligibility requirements.

Student Loans: Financial aid in the form of loans involves borrowing money that typically accrues interest and must be repaid. These loans are accessible to undergraduates, graduate students, and parents of dependent undergraduates. The loan terms are set by the lender, whether federal or private. Federal loans are standardized, meaning the options and eligibility are generally uniform for all applicants. Private loans are subject to underwriting and lender-specific provisions.

Types of Student Loans

Private Loans: Issued by a bank, credit union, or state-affiliated organization – not the federal government. Repayment schedules and interest rates are determined by the lender at origination. There is no forgiveness, and discharge at death is up to the lender. Once loans are private, they can not be refinanced or consolidated into a federal loan. Private loans are between you and that specific lender, and you are no longer eligible for any relief or programs provided by the federal government on that borrowed amount.

Federal Loans: Direct loans offered by the U.S. Department of Education. Types of Federal Loans:

Direct Subsidized: Available to undergraduate students with financial need, which is determined after completion of your FAFSA. The government pays your interest while you are in school and other qualifying periods, most notably the 6-month grade period.

Direct Unsubsidized: Available to undergraduate, graduate, and professional students. Financial need not necessary. Interest begins accruing immediately and continues to accrue during repayment grace periods.

Direct Consolidation Loans: Combining multiple federal education loans into a single loan. Although this is one loan, it will still be separated into subsidized and unsubsidized amounts. The interest rate is a weighted average of the underlying loans being consolidated.

Parent PLUS: Available to parents of dependent undergraduate students. Interest begins accruing immediately.

Grad PLUS: Previously available to graduate/professional students. Interest accrues immediately. Grad PLUS loans are being eliminated for new borrowers on July 1, 2026, although students can still borrow unsubsidized loans for graduate and professional school under new borrowing limits as explained below. There is an interim exception period for eligible existing Grad PLUS borrowers to continue.

Previous loans offered include Stafford, Perkins, and FFEL. Which repayment plan these loans are eligible for (if not consolidated) depends on the loan itself.

Student Loan Limits (Effective July 1, 2026)

Does not cover limits for students whose parent cannot secure a Parent PLUS loan.

Annual Loan Limit: Maximum amount per loan each academic year.

- Dependent Undergraduate:

- First Year: $5,500

- Second Year: $6,500

- Third Year+: $7,500

- Graduate Students: $20,500

- Professional Students: $20,500

- Parent PLUS: $20,000 per student

Aggregate Loan Limit: Maximum cumulative amount of combined direct subsidized and unsubsidized unpaid principal balance that you are allowed to have outstanding at any point in time.

- Dependent Undergraduate: $31,000

- Graduate Students: $100,000

- Professional Students: $200,000 (includes loans received as a graduate student)

- Parent PLUS: $65,000 per student

Lifetime Maximum Loan Limit: Total amount a borrower can ever receive in loans, regardless of amounts repaid and grade level.

- Combined Dependent Undergraduate, Graduate, Professional Loans: $257,500

- Parent PLUS: $65,000 per student

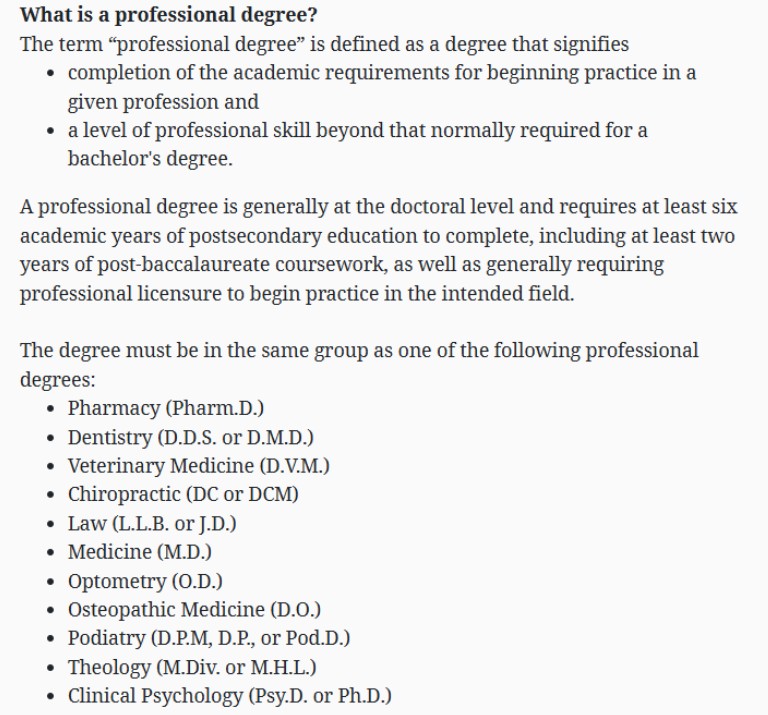

Definition of “professional degree” per the Department of Education website:

Key Student Loan Terms

Award Year: A 12-month period running from July 1 through June 30th is used to determine annual loan limits, financial aid, and disbursement. Your FAFSA from each year is used to determine your financial aid for the following award year.

Example: The 2026-27 FAFSA became available on September 24, 2025. The application deadline is June 30, 2027, but in reality, you need to apply much sooner. This FAFSA determines your eligibility for the 2026-27 award year (fall 2026 and spring 2027 semesters).

Interest Rate: The rate at which interest accrues on the unpaid principal of the loan. For federal student loans, the interest rate is fixed at the time of disbursement and will not change over the life of the loan unless the loan is consolidated. Interest accrues daily.

Accruing Interest: Interest accrues based on the principal balance of the loan. While unpaid interest can be forgiven (more on that later), it is not added to the principal of loan. It is a separate line item that needs to be repaid or possibly forgiven. If you have a $20,000 loan at a 7% interest rate, about $4 in interest would accrue daily ($125 per month). However, if your balance grew to $23,000 because you were in forbearance, deferment, or in a grace period, interest would still accrue only on the original $20,000.

Subsidized Interest: Interest that does not accrue and is paid by the federal government. There are two (2) ways to benefit from this. You have a direct subsidized loan and are either enrolled in school at least half-time, in a 6-month grace period after graduating or leaving school, or in an eligible deferment period. Or, you are on an eligible repayment plan. As of this publication date, the only repayment plan that allows interest to be subsidized is the Repayment Assistance Plan (RAP), which is set to start on July 1, 2026.

Interest Capitalization: Unlike interest that accrues or is subsidized, when your interest capitalizes, it is added to your loan’s unpaid principal balance (which is bad). Your interest is then recalculated based on that higher amount. In other words, you are paying interest on interest. Interest capitalizes on unsubsidized loans after deferments or upon leaving the Income-Based Repayment (IBR) repayment plan.

Repayment Cap: Under the Income-Driven Repayment plans of PAYE and IBR, your monthly repayment amounts are capped at the 10-year standard repayment plan amount. This is generally helpful when you are seeking forgiveness and, later in your loan term, your income exceeds your total balance.

Loan Statuses

Forbearance: An approved pause allowing you to temporarily stop making payments without penalty. Although interest can still accrue during this time. Types of forbearance are general (financial hardship), mandatory (service-related), or administrative (local/national emergencies).

Grace Period: The amount of time you are provided before having to repay your student loans due to leaving school or dropping below half-time enrollment. Eligible loans typically carry a 6-month period. Depending on the loan type, interest may still accrue.

Deferment: A wide range of approved reasons may qualify you to temporarily pause payments on your student loans. Depending on the type of deferment, interest may still accrue during the deferment period and capitalize at the end of that period if not paid.

Delinquent: Nonpayment of student loans when not in an eligible deferment or forbearance. After 90 days, you may receive a ding on your credit score. After 270 days, you’re considered to be in default.

Default: After 270+ days of delinquency, you are considered in default on your student loans. This is not good, and there is a scary list of possible consequences and penalties that the loan servicers or the government can use to negatively impact your finances or to collect the debt owed. Once again, this does not apply to borrowers in approved periods of forbearance or deferment.

Repayment: Actively making your monthly required payments.

Student Loan Forgiveness Programs

There are more, but I will cover only the most common ones here.

Public Service Loan Forgiveness (PSLF): Only available for employees working in the government or non-profit sector. If you satisfy the four (4) key components listed below, you will have the balance on your student loans forgiven. PSLF is a common path for occupations such as teachers, nurses, physicians, public attorneys, nonprofit employees, and government employees. Generally speaking, pursuing forgiveness makes sense if you are employed by a qualified employer and have a high student debt-to-income ratio. As in, you owe more than you earn annually. The four (4) key components:

Have Direct Federal Loans

Make 120 Qualifying Payments (do not need to be consecutive)

Work for a Qualifying Employer (including when you submit your final PSLF form)

Made Payments On Any Income-Driven Repayment Plan or the 10-Year Standard Plan (switching IDR plans does not reset your repayment progress)

Income-Driven Repayment Forgiveness: Accessible to all federal borrowers, no matter their occupation, who have consistently made payments under an income-driven repayment plan. One notable exception is Parent PLUS borrowers who have not consolidated their loans before July 1, 2026 and selected an IDR payment plan by July 1, 2028. IDR forgiveness may make sense if your loan balance is excessively high or if you expect to have a very low income and a correspondingly low repayment amount for the duration of your loan. Each Income-Driven Repayment Plan has its own repayment period toward forgiveness, and the remaining forgiven balance is TAXABLE as income for the tax year.

New IBR Plan: 20 Years

Old IBR Plan: 25 Years

PAYE Plan: 20 Years

ICR Plan: 25 Years

RAP Plan: 30 Years

Student Loan Repayment Options

When making monthly student loan payments, you are either on a “fixed payment” plan or an “income-driven repayment plan.”

Fixed Payment Repayment Plans: Monthly repayment amount is determined by how much you owe, the interest rate, and the loan maturity. Payments are calculated to ensure your loan is paid in full. Unless on a specific 10-Year Standard Repayment plan, you do not accrue credits toward forgiveness.

Fixed Payment Repayment Plans (For Existing Borrowers BEFORE July 1, 2026)

Standard Repayment Plan: Fixed payments for 10 years for individual loans or 10 to 30 years for Consolidation Loans based on balance.

Graduated Repayment Plan: Payments increase gradually every two years on the same maturity schedule as the Standard Repayment Plan. This allows for lower payments early after graduating from college, with higher payments later. Sounds great in theory, but this is typically a costly option.

Extended Repayment Plan: If eligible, it extends your standard or graduated repayment plan beyond 10 years and up to 25 years for non-consolidated loans.

Fixed Payment Repayment Plans (For New Borrowers ON/AFTER July 1, 2026)

Definition of “New Borrower”: If you have a single loan, including a consolidation loan, that is disbursed on or after July 1, 2026, you’ll lose eligibility for any repayment options available to existing borrowers prior to that same date on ALL YOUR LOANS.

Tiered Standard Repayment Plan: Fixed and equal payments over a 10 – 25 year period based on outstanding principal balance. Payments do not count toward loan forgiveness.

Less than $25,000: 10 Years

$25,000 – $50,000: 15 Years

$50,000 – $100,000: 20 Years

$100,000+: 25 Years

Income-Driven Repayment Plans (IDR): Monthly repayment amount is determined by household income and size. IDR plans are eligible for certain types of forgiveness. Whether you would benefit from pursuing forgiveness depends greatly on your specific situation. As previously mentioned, if you qualify for Public Service Loan Forgiveness (PSLF), all IDR plans require 120 qualified payments (10 Years).

Income-Driven Repayment Plans (For Existing Borrowers BEFORE July 1, 2026)

For simplicity, I am not including the Income-Contingent Repayment Plan (ICR) or the Pay As You Earn Plan (PAYE), since these options will be phased out completely for all borrowers by July 1, 2028. There’s only one obscure reason you might hang on to the ICR plan, which is that you’re a Parent PLUS borrower who never consolidated by the July 1, 2026 deadline and are therefore ineligible for other IDR plans. As for PAYE, there’s a chance you’d benefit from being on this plan if you’re only eligible for the Old IBR Plan (borrowed before July 1, 2014).

Old IBR Plan (2009):

Eligibility:

First Borrowed Before July 1, 2014

No New Loans After June 30, 2026

Repayment Amount: 15% of Discretionary Income

IDR Repayment Period for Forgiveness: 25 Years

Subsidized Interest: No

Repayment Cap: Yes

New IBR Plan (2014):

Eligibility:

First Borrowed After July 1, 2014

No New Loans After June 30, 2026

Repayment Amount: 10% of Discretionary Income

IDR Repayment Period for Forgiveness: 20 Years

Subsidized Interest: No

Repayment Cap: Yes

RAP Plan (July 1, 2026):

Eligibility: Federal Loans (unless they include Parent PLUS)

Timeline: Starts July 1, 2026

Repayment Amount: Tiered % based on AGI (Adjusted Gross Income) and the following income brackets:

< $10,000: $10/month

$10,001 to $20,000: 1% of AGI

$20,001 to $30,000: 2% of AGI

$30,001 to $40,000: 3% of AGI

$40,001 to $50,000: 4% of AGI

$50,001 to $60,000: 5% of AGI

$60,001 to $70,000: 6% of AGI

$70,001 to $80,000: 7% of AGI

$80,001 to $90,000: 8% of AGI

$90,001 to $100,000: 9% of AGI

$100,001+: 10% of AGI

IDR Repayment Period for Forgiveness: 30 Years

Subsidized Interest: Yes

Repayment Cap: No

Miscellaneous: $50 reduction for each monthly payment per dependent

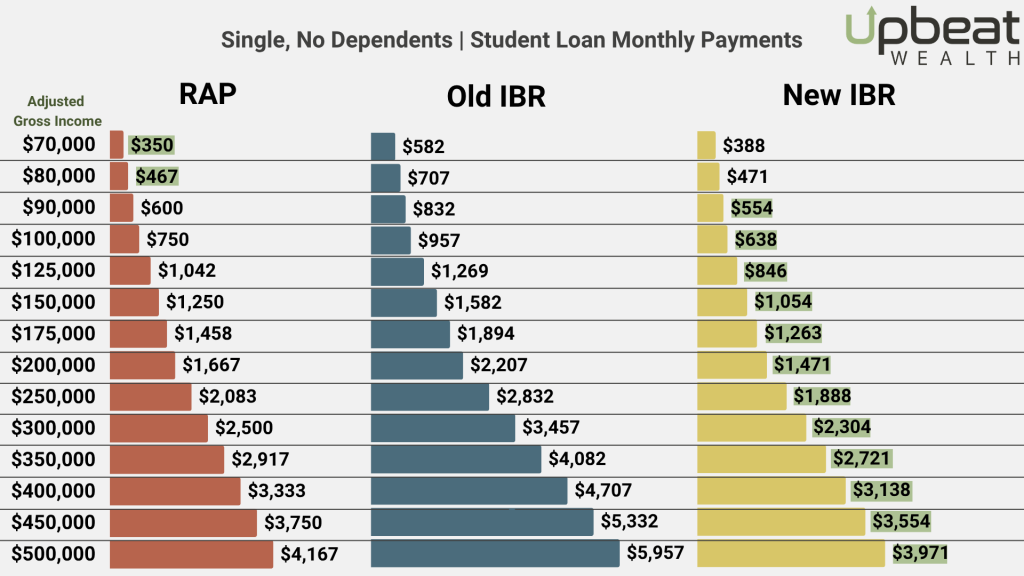

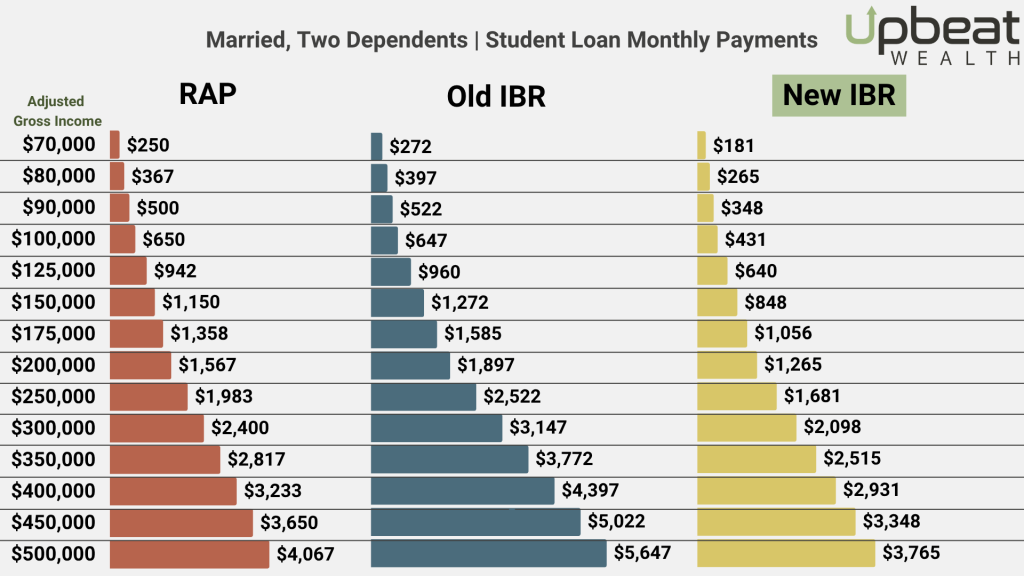

One of the key distinctions between IBR and RAP is how the repayment amount is calculated.

IBR uses a percentage (%) of “Discretionary Income” and RAP uses a percentage of your actual “Adjusted Gross Income”. Discretionary Income is defined as your Adjusted Gross Income Minus the Federal Poverty Level Multiplied by 150%. Here are some monthly repayment examples, assuming one borrower per household and no repayment caps:

Household 1: Individual with $80,000 of Adjusted Gross Income (AGI)

New IBR Plan: ((($80,000 – ($15,960 x 150%)) * 10%) / 12 → $467/mo

Old IBR Plan: ((($80,000 – ($15,960 x 150%)) * 15%) / 12 → $701/mo

RAP Plan: ($80,000 * 7%) / 12 → $467/mo

Household 2: Married + 2 Dependents with $400,000 of Adjusted Gross Income (AGI)

New IBR Plan: ((($400,000 – ($33,000 x 150%)) * 10%) / 12 → $2,921/mo

Old IBR Plan: ((($400,000 – ($33,000 x 150%)) * 15%) / 12 → $4,381/mo

RAP Plan: (($400,000 * 10%) / 12) – $100 → $3,233/mo

Final Thoughts

Congratulations, you’ve made it to the end! Bookmark this for future updates, and we’ll continue to relink any updated versions. Ultimately, the best student loan advice we could ever give anyone is to get a clear plan from an expert if you don’t have one! It might be the best money you’ve ever spent, not just for the money you save, but for the peace of mind it brings.

Frequently Asked Questions About Student Loan Terms

Q1: What is student loan interest capitalization?

A1: Interest capitalization happens when unpaid interest is added to your loan’s principal balance. Once capitalized, future interest accrues on the higher balance, increasing the total cost of repayment over time.

Q2: What is the RAP student loan repayment plan?

A2: The Repayment Assistance Plan (RAP) is a new federal income-driven repayment plan scheduled to begin July 1, 2026. Payments are based on a percentage of adjusted gross income (AGI), and unpaid interest may be subsidized by the federal government.

Q3: How does Public Service Loan Forgiveness (PSLF) work?

A3: PSLF forgives remaining federal student loan balances after 120 qualifying monthly payments while working full-time for an eligible government or nonprofit employer under a qualifying repayment plan.

Q4: Will federal student loan repayment plans change after July 1, 2026?

A4: Yes. Borrowers receiving new federal loans on or after July 1, 2026 may lose access to some existing repayment plans and become subject to the newer RAP and Tiered Standard repayment structures.

Mike Turi, CFP® APMA™ is the Founder and a Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.