Creating a Student Loan Repayment Plan

Let me start by saying that the goal of this article is to provide an objective summary of the changes in the student loan world for existing borrowers, helping people make informed decisions moving forward. The purpose isn’t to criticize or pass judgment on the ongoing legislative issues or poor execution. We’ll briefly mention some changes affecting new borrowers but reserve a more detailed explanation for later. If you’re a parent planning to borrow for your child or a student preparing for graduate or professional school, you’ll face the biggest challenges from the upcoming changes if taking out loans after July 1, 2026. Borrowing after July 1, 2026, can also affect how you repay your existing loans.

Currently, 7.7 million people are on SAVE forbearance. Most people feel frustrated, confused, and uncertain about how they will repay their loans. They are exhausted from being the ball in an endless game of political ping pong. If you’re one of those people, this article is for you.

Student Loan Repayment Options

Need a refresher on student loan repayment options? Here’s a bird’s-eye view from the Department of Education: https://studentaid.gov/manage-loans/repayment/plans

Generally speaking, borrowers have two options to pay back their student loans:

-

Fixed payment: Loans structured for borrowers to pay off their balances in full within a specified time period

-

Income-Driven Repayment (IDR): Monthly payments are calculated using your household income and size. IDR is primarily designed for borrowers seeking some type of student loan forgiveness.

So, why wouldn’t everyone choose to make payments under an income-driven repayment plan and aim for forgiveness? You have a high income. When your student loan repayment is based on your income, it might cause you to pay off your loans too quickly to qualify for forgiveness or raise the payment above what you’re comfortable paying. Or the opposite, you might actually want to pay off your loans quickly but prefer not to deal with the hassle of recertifying income annually. Perhaps you’ll refinance to lower your interest rate and pay off your loans as fast as possible.

Income-Driven Repayment Plans

As mentioned, on an Income-Driven Repayment plan, your total repayment amount is calculated based on your income. The balance and interest of your loan only apply to plans that have “payment caps.” A payment cap puts a ceiling on your total monthly payment, which is equal to what you would pay under the 10-Year Standard Repayment Plan, a fixed repayment plan. Payment caps are applicable to two IDR plans, PAYE and IBR. Payment caps are a valuable feature for borrowers with rising incomes who may still qualify for forgiveness.

There are currently six(ish) IDR Plans: PAYE, Old IBR, New IBR, ICR, SAVE, RAP.

PAYE: Eligible for existing borrowers with loans originated after October 1, 2007 AND a Direct Loan after October 1, 2011 until June 30, 2026

Old IBR (2009): Eligible for existing borrowers with loans originated before July 1, 2014

New IBR (2014): Eligible for existing borrowers with loans originated after July 1, 2014 until June 30th, 2026

ICR: Eligible for existing borrowers until July 1, 2028

SAVE: No longer eligible for enrollment

RAP: Created by the One Big Beautiful Bill Act (OBBBA), but not yet available for enrollment

IBR is technically “one plan,’ but we are treating it as two separate plans because changes made in 2014 benefit eligible borrowers by lowering their payments. Since New IBR is notably better than Old IBR, you need to know which plan applies to you.

Common Paths Toward Student Loan Forgiveness

Public Service Loan Forgiveness (PSLF)

The primary goal of using an income-driven repayment plan is to reduce your student loan payments (especially for those with high balances and low incomes) and eventually qualify for forgiveness. Even professionals with high incomes can benefit from forgiveness if their loan balance is substantial and they experience a period with a temporarily low income, such as during residency for physicians.

Although some occupation-specific forgiveness programs exist, the most well-known and widely discussed is the Public Service Loan Forgiveness (PSLF) program, which covers those who work full-time for a not-for-profit or government organization. Popular occupations include healthcare workers, military personnel, law enforcement officers, first responders, teachers, local and federal government employees, social workers, and nonprofit workers.

Unsure if you qualify for PSLF? There are 4 Key Components:

Have Direct Federal Loans

Make 120 Payments

Work for a Qualifying Employer (including when you submit your final PSLF form)

Make Payments On An Income-Driven Repayment Plan (although the 10-Year Standard Plan also counts toward this)

IDR Forgiveness

Workers in the private sector can also qualify for forgiveness under an IDR plan, but it will take longer than the time available to public servants under PSLF. If you do not qualify for PSLF, you’ll have to repay your loans for 20, 25, or 30 years to get forgiveness, depending on which IDR plan you’re enrolled in.

PAYE: 20 Years

New IBR: 20 Years

Old IBR: 25 Years

ICR: 25 Years

RAP: 30 Years

Another key difference is that PSLF forgiveness is not taxable, whereas IDR forgiveness is. This is often referred to as a tax bomb, and it will take effect again starting January 1, 2026. The forgiven balance of your student loans will be counted as income in the year it is forgiven. To clarify, this does not apply to public servants repaying their loans through PSLF, which remains protected as tax-free under federal law.

Current OBBBA Updates for Existing Borrowers

As of July 29th, 2025, many of the “updates” expected to be rolled out by OBBBA have not yet been implemented. Here are some of the changes that are effective immediately or, at the very least, actionable.

Existing Parent PLUS Loans Now Qualify for IBR

Previously, Parent PLUS borrowers had access only to ICR, the least favorable IDR plan with the highest monthly payments, unless they used a strategy known as the double consolidation loophole. Now, as long as Parent PLUS borrowers consolidate before July 1, 2026, and enroll in an IDR plan before July 1, 2028, they will qualify for plans beyond ICR, which is the least favorable IDR plan. This is good news for parents who have borrowed on behalf of their kids.

SAVE Plan Forbearance

If you are already enrolled in the SAVE plan, you will remain in forbearance until the sooner of a court ruling or July 1, 2028. This should not be confused with the announcement by the Department of Education stating interest will start accruing on August 1, 2025. Interest beginning to accrue again doesn’t mean you have to start making payments. You are protected from defaulting on your loans under SAVE through forbearance. Later, we’ll discuss reasons you may voluntarily move off SAVE, but for right now, you are not required to voluntarily switch or pay.

Future OBBBA Updates for Existing Borrowers

Most of the legislative changes in the OBBBA have not yet taken effect or are scheduled for future dates. Here are a few of the major changes existing borrowers can expect to see in the coming years.

Some IDR Plans (PAYE, ICR, SAVE) Will Be Eliminated

The following IDR plans will be phased out and eliminated. Existing borrowers will not be grandfathered into these plans and will not be allowed to make payments on them beyond July 1, 2028. It is unclear how the Department of Education will handle the transition, but all borrowers in the plans listed below will be asked to switch before July 1, 2028.

PAYE: July 1, 2028

ICR: July 1, 2028

SAVE (formerly REPAYE): Sooner of a court ruling or July 1, 2028

Please note that if you were paying under REPAYE, you were automatically moved to SAVE in 2023.

A New IDR Plan (RAP) Will Be Created

A new IDR plan, called the Repayment Assistance Plan (RAP), will be introduced by July 1, 2026. This will leave existing borrowers (those with no loans originated after July 1, 2026) with the following IDR plan options beyond July 1, 2028.

Old IBR (Borrowers Before July 2014)

New IBR (Borrowers After July 2014)

RAP

Partial Financial Hardship Will Be Removed for PAYE & IBR

Previously, you could only switch to the IBR plans if you had a partial financial hardship, which was defined by your income-driven repayment being less than your 10-year Standard Repayment amount. Lawmakers recognized that this would be problematic for many borrowers who were making payments on IDR plans that will ultimately be eliminated. Therefore, to expand eligibility for PAYE and IBR, they are removing the partial financial hardship requirement for enrollment. Unfortunately, there is no specific timeline for when this change will take effect and be implemented by the loan servicers. So, PAYE/IBR might show as ineligible on your studentaid.gov portal for now, even though you’re eligible to enroll. Frustrating!

Department of Education Confirms “Buyback” Will Continue for PSLF-eligible Borrowers

Borrowers who have 120 months of eligible employment can buy back periods of deferment or forbearance, provided this brings their total to 120 qualifying payments. The Department of Education announced that in the future, borrowers may buy back previous months even if they do not have 120 months of eligible employment. While it is not guaranteed in the future, as of now, you are eligible to buy back every month you’re in SAVE forbearance, assuming you work for a qualified employer. You still cannot buy back months spent not on an IDR plan or working for a nonqualified employer.

Changes for Borrowers Taking Out Loans on or After July 1, 2026

The biggest impact of the OBBBA is for borrowers who need to continue borrowing on or after July 1, 2026, as repayment options will become very limited. New borrowers on or after July 1, 2026, and those who consolidate after that date will only have access to two plans.

An Updated Standard Repayment Plan: the repayment term depends on your loan balance.

The Repayment Assistance Plan (RAP): the only IDR plan option

The situation is even worse for new Parent Plus borrowers; they will only have access to the Standard Repayment Plan, and these loans will no longer qualify for forgiveness.

Borrowers taking out loans on or after July 1, 2026, will face new loan limits for graduate and professional schools as well as for Parent PLUS loans.

There are changes in procedures for exiting default on loans, qualifying for economic hardship, and entering forbearance, none of which are favorable compared to the current rules.

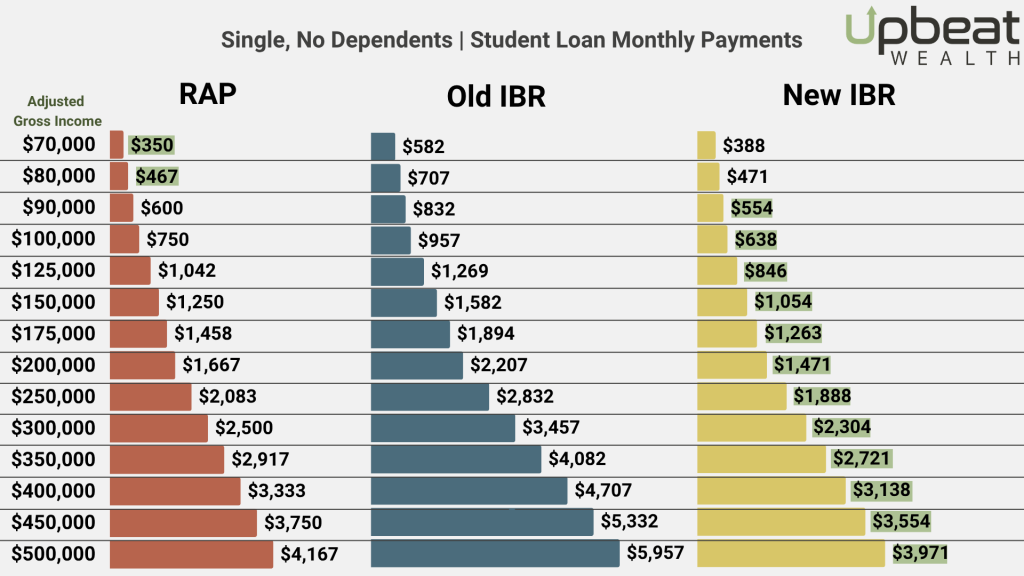

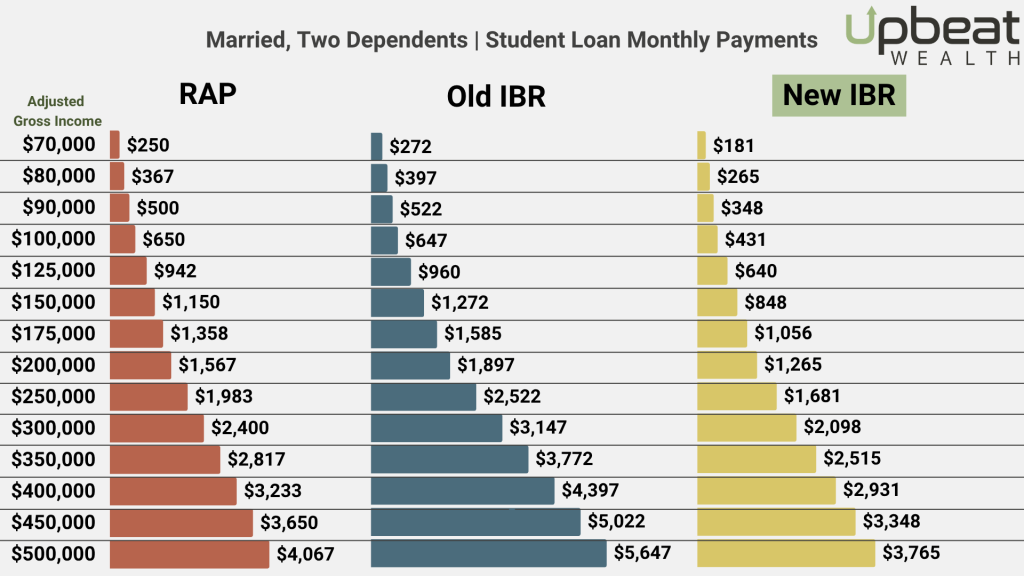

Is the New IDR Plan (RAP) Any Good?

The RAP Plan is the Republican response to President Biden’s SAVE Plan. While the SAVE Plan was very generous for many borrowers, the RAP Plan is not as kind. The SAVE plan effectively lowered payments for many borrowers compared to other IDR plans. RAP, unfortunately, does mostly the opposite. However, there are small pockets of borrowers who will benefit from a lower payment under RAP compared to New IBR, specifically those with balances between $30,000 and $80,000.

In line with Income-Driven Repayment Plans, your payment is based on income, although it’s calculated differently than previous IDR plans. Instead of explaining how the income is calculated, I will show you an illustration of how the monthly payments compare across plans. Here are some example monthly payment calculations for RAP vs. Old IBR vs. New IBR.

Illustration notes: New IBR and PAYE payments are the same. Additionally, this doesn’t consider the monthly payment cap borrowers qualify for under IBR/PAYE, where your payment is limited to the 10-year standard repayment amount. Therefore, the IBR payments shown may actually be lower in your personal situation depending on your loan balance and interest rate.

RAP Plan Pros

RAP upholds a popular student loan strategy where borrowers can file their taxes separately and pay based on their individual income instead of the household’s income. This is especially useful when the borrowing spouse earns less or is currently unemployed.

Similar to the SAVE plan, if your monthly payment does not cover the interest, the government will waive it and pick up the tab. It will not be added to the loan.

In addition to waiving interest, the government will contribute up to $50 toward your loan so your principal actually goes down.

RAP Plan Cons

Lowest-income borrowers will still need to pay at least $10 per month. There is no option to have a $0 student loan payment.

If you don’t qualify for PSLF or other forgiveness programs, you need to make 30 years of payments to get IDR forgiveness with RAP. That’s 10 years longer than what is required by New IBR & PAYE.

Other IDR plans determine the amount you can pay based on your “discretionary income,” which is calculated by subtracting a percentage of the Federal Poverty Level (FPL) for your household size. The FPL increases each year to account for inflation, allowing you to exclude a larger amount of income from your household income when calculating your monthly repayment. The RAP plan bucks this trend, so inflation will not help reduce your payment.

RAP will cost households where both partners have student loan debt. Unlike other IDR plans, there is no prorata calculation used to determine each spouse’s student loan payment based on household income. Instead, as we understand it now, RAP requires each borrower to pay the full calculated amount for their individual loans and does not lower that payment unless you file your taxes married filing separately to exclude your partner’s income.

There is no payment cap relative to the 10-Year Standard Repayment amount.

If I’m In The SAVE Forbearance, What’s My Move?

Giving specific student loan advice is a tall order, so that’s not the goal for the rest of this blog. Ultimately, many variables affect your situation: the type of loans, eligible plans, PSLF or IDR credits, your income, your spouse’s income, projected career path, and household size. And then there’s the total uncertainty of future policy changes. HOWEVER, here’s what I would generally consider in some common scenarios.

When Staying in SAVE Might Make Sense:

You have made or will make 120 payments, including the SAVE forbearance period, and are currently awaiting the Department of Education’s review of your PSLF Reconsideration request for buyback.

You have higher-interest loans that you’re working on paying back, like credit card debt. Your money is probably better spent paying down higher-interest loans.

You are not a public servant, and it’s not clear whether IDR forgiveness or paying off your loans completely is the better financial choice. Additionally, until the partial financial hardship requirement for PAYE or IBR is removed, you’re stuck with the least favorable plan, ICR, as your only option. You might just let the interest on your loans accrue until that partial hardship is removed.

You expect your income to decrease in the future, making your payments toward forgiveness cheaper than they are now.

You don’t want to remove yourself voluntarily from SAVE until it’s official that interest will truly accrue.

You already filed your 2024 taxes as married filing jointly, but ideally, you might benefit from filing married filing separately and using only your income to determine the monthly payment.

When Switching from SAVE to PAYE Might Make Sense:

Your income is similar to your last recertification, and you’re ready to start making payments again to earn credit toward IDR forgiveness or PSLF.

Once the partial hardship is removed, you can switch and still be limited to the 10-Year Standard Repayment, which allows you to balance the option of continuing earning forgiveness credits with paying back your loans in full.

You took out loans before July 1, 2014, and now only qualify for Old IBR. PAYE is a more affordable plan in any situation compared to the Old IBR. Yes, you’ll need to leave PAYE by July 1, 2028, but at least you’ll get a few years of lower payments before that.

You’re far from forgiveness and have a career path with increasing income. You might want to start earning guaranteed PSLF/IDR credits now at a lower amount, avoiding the need to buy back later. It’s also possible that the buyback amount will be the same as your PAYE payment today.

When Switching From SAVE to Old IBR Might Make Sense:

You only need to make a few more payments to reach 120 credits and want to avoid waiting for PSLF buyback, or you need to act quickly on PSLF because you’re leaving a qualifying employer. Remember, you must be actively employed at a qualified employer when submitting your PSLF forgiveness application.

When Switching From SAVE to New IBR Might Make Sense:

The advantages of switching to New IBR and PAYE are 99% similar. However, you can go directly to New IBR if you prefer not to switch off PAYE when it becomes obsolete in 2028. The New IBR will continue to exist, and the payments for New IBR and PAYE are exactly the same. The only downside of New IBR compared to PAYE is that if you ever need to switch off New IBR, your interest will capitalize. So, if a more attractive IDR plan is introduced in the future, any unpaid interest will be added to the loan principal. This only becomes a problem if you need to pay off your loans in full later.

Private Refinancing Might Make Sense:

You will definitely pay off your student loans, and refinancing with a private lender can lower your student loan interest rate by over 2%. I mention 2% because you should carefully consider this option, as a private takeover of your federal loans is irreversible and can also remove some protections. Additionally, it could exclude you from any future relief resulting from policy changes by a different administration.

The Biggest Variable is Future Policy Uncertainty Beyond This Administration

Student loan policy may become a single-issue concern for voters in the future. There will be considerable frustration due to the fallout from OBBBA. And contrary to belief, this isn’t just coastal liberal arts professionals who will suffer. Doctors and lawyers are also taking a big hit. Furthermore, the downsizing of the federal government eliminated the possibility of PSLF for many public servants. Our teachers, first responders, and soldiers, who are already struggling to make ends meet, may now face higher payments. This is pure speculation, but I believe the Democrats will try to capitalize on this, and if they successfully regain unified control, we could see another major shift in policy.

Our Biggest Recommendation

If you’re confused, hire a knowledgeable expert in student loan repayment and forgiveness. Several reputable companies offer one-time consultations for $400 to $700. Student loan strategies can be complicated, and choosing the right one could save you tens of thousands of dollars. That’s a potentially huge return on your money. And whatever you do, ignore anyone in the media *lecturing* you about how you should pay back your student loans dollar for dollar. Ignore their tired ass complaints about how people used to honor their debts in the past. If you are eligible for a path toward forgiveness and will spend less getting there than paying back your student loans in full, it is your American right by law to pursue it!

Mike Turi, CFP® APMA™ is the Founder and a Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.