The Benefits of Upgrading Your Home

Is this not your first rodeo when it comes to buying a home, and you’re ready to get back on the horse? This blog is for you. It’s natural for young families to want to upsize their homes at some point. Common reasons for upgrading include:

More Space

Better School District

Higher Paying Job

Closer to Free Childcare, I mean, Family

Weighing the Pros and Cons

Some trade-offs, such as increased income, public schooling, or free childcare, may result in a net neutral or positive cash flow outcome, thereby avoiding the need for lifestyle adjustments. Others may result in a diminished ability to cover current expenditures and lifestyle goals. Examples of expenses and goals that could be negatively affected by a larger mortgage and escrow:

-

Education Funding

-

Retirement

-

Travel

-

Everyday Pleasures

-

Work-Life Balance

As a financial planner, it isn’t our job to plansplain what your values should be! Yes, I did just invent the word planspain. Our role is to help you clarify your priorities, establish boundaries, and evaluate trade-offs, enabling you to make the most informed decision based on your specific situation. So, what are some healthy boundaries when deciding what a reasonable amount to spend on a new home is? There are several handfuls of rules of thumb from asset-based and income-based approaches for determining maximum home affordability. I will focus on our preferred guideline, which has been adjusted to be more conservative than the lender’s standard.

Enter the 25/33 Rule, Adjusted Down from the 28/36 Rule

We recommend the 25/33 Rule, which states you shouldn’t spend more than 25% of your pre-tax monthly income on housing and no more than 33% on all debts. Other factors, such as family wealth, lifestyle, schooling costs, and overall assets, also influence your financial flexibility beyond this rule. Still, everything else being equal, going over the 25/33 Rule often causes families earning less than $200,000 to feel financially strained in other areas.

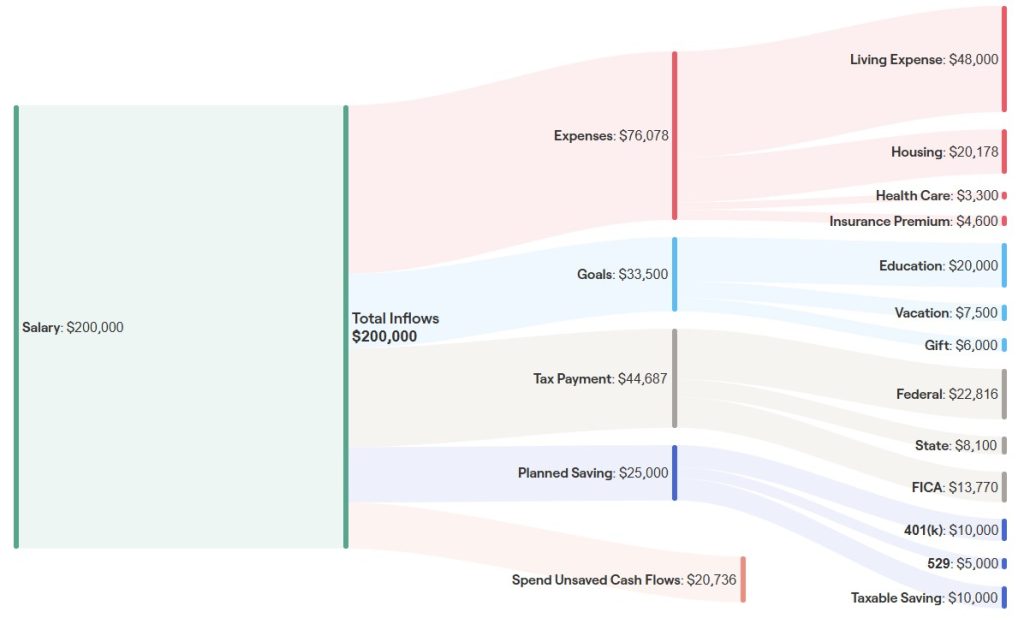

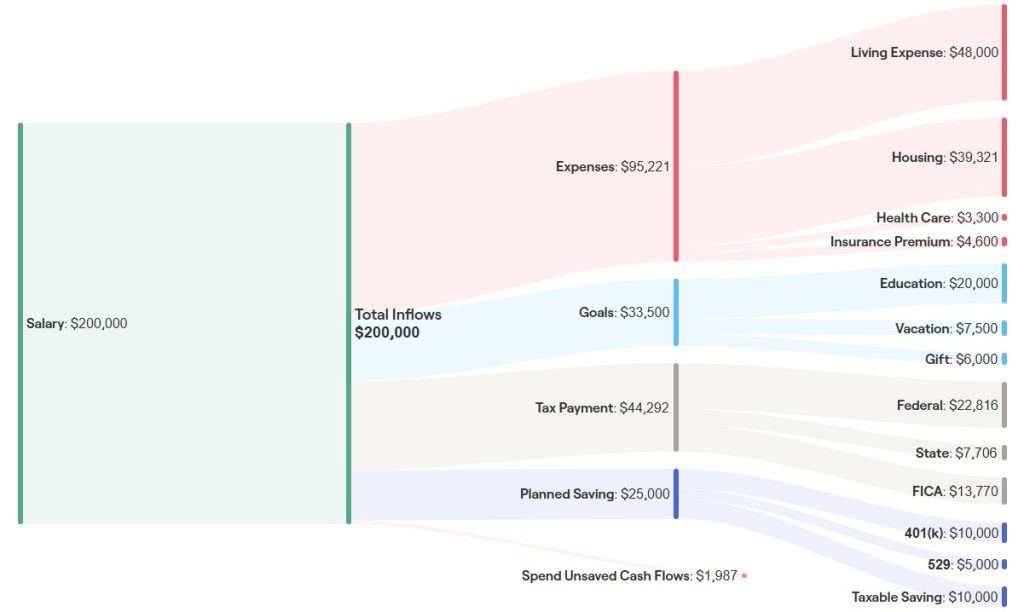

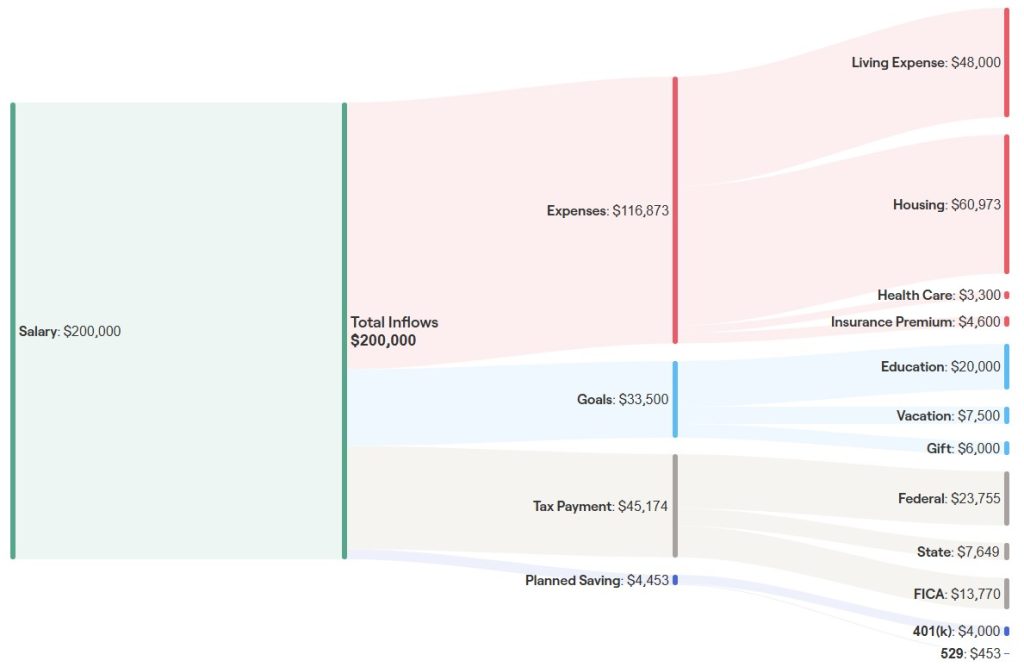

Let’s examine sample cash flows from families whose housing costs are 10%, 20%, and 30% of their pre-tax income.

Case Scenario 1: Millennial Family with 10% Total Housing Cost

Case Scenario 2: Millennial Family with 20% Total Housing Cost

Case Scenario 3: Millennial Family with 30% Total Housing Cost

In the above scenarios, the total housing cost includes not only your mortgage (principal + interest), but also property tax, homeowners insurance, and maintenance costs. For maintenance, we always use the 1% rule, which recommends setting aside 1% of your house value annually for upkeep. As your total housing costs progress from 10% to 20% to 30% of your salary, watch that cash flow dry up. Your ability to save for your future or your children’s becomes increasingly difficult. Travel, Gift, and Education budgets could all find themselves on the chopping block. Depending on your liquid assets, you might have limited options to act or respond during times of uncertainty or when your life becomes more complicated.

The Risk of Your Primary Residence Equaling Your Net Worth

You also wouldn’t be alone if you considered your primary home your most valuable asset and the key to building wealth. Here are the risks:

-

Lack of Diversification. While it CAN work out, putting all your eggs in one basket is a risky approach.

-

Illiquidity and Inconvenience. If you need to take money out of the home, it could be expensive in the form of a loan. Or, you might need to sell the home and move entirely.

-

Surprise Maintenance Costs. It’s important to remember that your Principal, Interest, Tax, and Insurance is the MINIMUM amount you’ll pay.

-

Mortgage Amortization: If you are forced to sell, you may not have built a meaningful amount of equity in the home. Depending on your interest rate, a significant portion of your mortgage payment goes to the lender as interest during the first 5 years. The payments typically don’t shift to mainly principal until 10 to 15 years into the repayment period.

The Danger in Upsizing Your Home Before Milestones, Specifically KIDS

The times when upsizing your home presents the biggest hurdles:

- Before you have kids, if that’s the path you’re choosing.

- As you are paying for childcare.

The cost of raising children alters not just your cash flow but your outlook on life. Locking yourself into a bigger home too early, especially one at the upper edge of what you can reasonably afford, can cause financial problems if it’s not part of your long-term plan. And while you might believe you’re preparing for that moment, it’s hard to understand the unknown. It’s worth thinking about how long you stayed in your *starter* home before life changed and you began reviewing options to upgrade. Milestones tend to prompt us to reassess our lifestyles.

Renting vs. Selling Your Previous Home

If you are relocating or upsizing and wondering whether to keep your previous home as a rental, you’re not alone. We get this question often. As of the published date of this blog, mortgage rates are approximately double what they were 3 years ago.

Here are the two questions you need to ask yourself.

-

Will the rental income you receive actually cover not only your minimum financial costs like principal, interest, taxes, and insurance, but also generate a surplus for unexpected expenses such as vacancies and maintenance?

-

Do you actually have any desire to be a landlord? If you used to worry about spending evenings and weekends on home maintenance projects and repairs for your family, now imagine doing that for complete strangers on their schedule, while you’re commuting. And oh, by the way, you’re likely moving into a bigger home, which will also require a greater time commitment for maintenance.

If you’re answer is “no” to either of these questions, you should highly consider selling your previous home. Otherwise, you’re really just speculating that you’ll get a better price in 1 – 3 years. That’s a complete dice roll. And if you don’t sell within 3 years, you miss out on a significant tax exclusion where your primary residence is exempt from capital gains tax. The Capital Gains Exclusion for Primary Homes allows you to exclude the first $250,000 of gain for an individual and $500,000 for a married couple filing jointly from being subject to capital gains tax.

Run. Those. Numbers. Then Actually Implement It!

When analyzing upgrading your home, the same principles apply as when you purchased your first home. And now, you’re a seasoned homeowner. You know that the cost of property tax and insurance only go in one direction, up! You understand that maintenance and upkeep costs are not zero, and they are generally expensive and a hassle. You will not mistake your approved borrowing amount with how much home you can afford.

But until you lay out your cash flow and see the trade-offs firsthand, you are blindfolding yourself when it comes to making this decision. My recommendation is to live within the confines of your new projected budget for several months to ensure it’s a worthwhile tradeoff. Are you willing to make the sacrifices necessary to your current lifestyle when it comes to upsizing to a more expensive home? Otherwise, you risk falling into the biggest wealth trap: becoming house poor.

Need a refresher on what total housing costs look like? Last month (May 2025), Lead Planner Eddy Jurgielewicz shared some helpful advice on how much money you need to buy a home. He also included one of our in-house home purchase calculators to help prospective buyers understand the total cost of homeownership. While the calculator was an exclusive offering for our newsletter subscribers, you can view the excerpt about approaching homeownership from Eddy in this LinkedIn post. Want to avoid missing out on future exclusive content? Sign up for our newsletter using this link: subscribepage.io/eXkcnF

Mike Turi, CFP® APMA™ is the Founder and a Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.