Once you have a firm grasp on the fundamentals of incentive stock options, it’s time to peel back the layers on their tax implications. While they can seem needlessly complex, rest assured that ISOs do have plenty of positive attributes when it comes to their relationship with taxes. So it pays to get a handle on it.

To tackle this, we’ll examine some very specific tax-related questions:

- What unique tax advantages do ISOs have?

- What is the Alternative Minimum Tax?

- Why do I need to worry about AMT with ISOs?

- What are the different tax scenarios I could face when selling exercised ISOs?

- What types of taxes are owed?

- What are the possible advantages of an early exercise (if available)?

- How should you cover the tax liability associated with selling stock acquired through an ISO grant?

- What ISO-specific tax documents and forms should you be on the lookout for?

And if you need a refresher on all the ISO terminology, be sure to visit the bottom of our Part 1 post for a list of must-know definitions!

What unique tax advantages do ISOs have?

The headline tax benefit of incentive stock options boils down to WHEN you pay taxes and the TYPE of taxes you’ll owe.

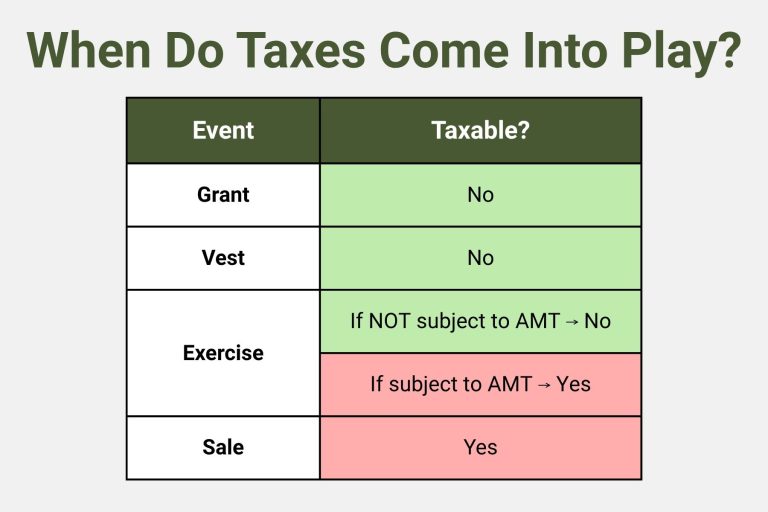

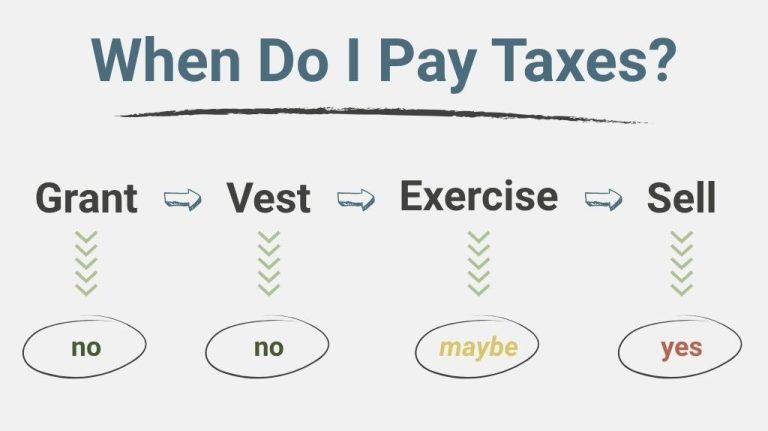

ISOs are not taxed at all when they’re granted or when they vest. The kicker is that – unless AMT is owed – there is also no tax liability created when you exercise either. What’s more, it’s possible in some scenarios that the entire financial benefit realized through an ISO exercise and subsequent sale is taxed at the friendlier capital gains tax rate (vs. ordinary income rate).

For comparison… In the case of their equity comp cousin – Restricted Stock Units (RSUs) – the value at the time of vest is immediately counted towards your ordinary income for that year. And for the more closely related sibling – non-qualified stock options (NSOs) – you should expect to pay ordinary income tax at exercise.

What is the Alternative Minimum Tax?

The Alternative Minimum Tax (AMT) is an entirely separate tax system and calculation that exists in addition to the “regular” one most of us are accustomed to. Technically, everyone should calculate both their regular tax and AMT liability each year – then pay whichever is higher. But for the vast majority of people, the “regular” tax amount is the bigger bill.

One of the big differences between the two tax systems is that some of the credits and deductions people can take when calculating their regular tax don’t apply for AMT. A good example is the deduction for state and local taxes – it can’t be taken at all under AMT. This gets at why the system was created in the first place, as a way to try and make sure some wealthier individuals weren’t benefiting too much from credits and deductions in the regular tax framework.

The alternative minimum tax has different tax rates and standard deductions. On top of federal AMT, some states have their own version. Those lucky states are California, Colorado, Connecticut, Iowa, and Minnesota.

Why do I need to worry about AMT with ISOs?

The spread (difference between the strike price and FMV on the date of exercise) is not taxable under the normal tax system. It’s not considered income on Form 1040. Unfortunately, the spread is one of those pesky items considered income for AMT purposes and is thus factored in on Form 6251, which is used to calculate an individual’s Alternative Minimum Tax liability.

If you exercise ISOs and do NOT sell them in the same tax year, you need to check to see if this pushes you into AMT territory. If, however, you do sell the shares in the same year as exercise, the spread will not need to be added into the AMT calculation.

Bear in mind that just because you have an ISO spread for the year, it doesn’t mean you’ll owe AMT. It’s only if it pushes your AMT liability to a higher amount than your regular tax liability comes out to be.

What are the different tax scenarios I could face when selling exercised ISOs?

Moving on from exercising incentive stock options to selling the shares here… Again, this might be the first time many recipients of ISOs have to worry about paying any taxes.

It’s important to know that there is no default withholding when you sell the shares you received from an exercise. Therefore, it’s on you (plus your advisor and CPA, hopefully!) to proactively assess taxes that are due and how/when to pay them. The first step is to determine whether the sale of the ISO shares is considered a qualifying disposition or a disqualifying disposition.

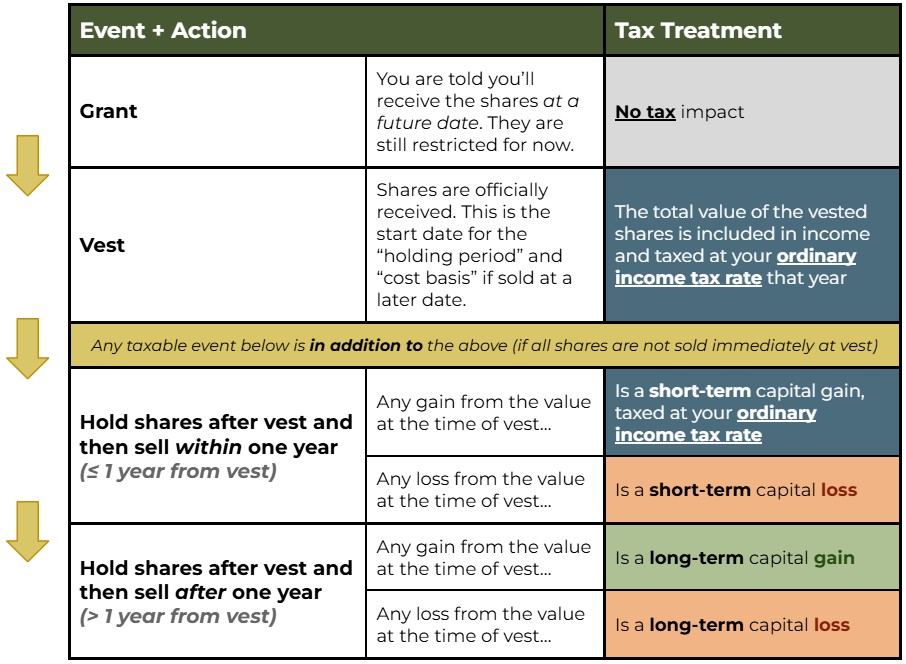

Qualifying Disposition

The sale is a qualifying disposition if the stock was held for at least 1 year after exercise AND at least 2 years after the grant date. In this case, ALL proceeds are taxed at the more generous long-term capital gains rate. Your basis in the sale is whatever the strike price was. So your spread PLUS any increase in value after exercise get that preferential tax treatment.

Of course, the stock price could decline after exercise. If this were to occur, then you would still pay long-term capital gains tax on the difference between the FMV on the date of sale and the strike price.

Disqualifying Disposition

The sale is classified as a disqualifying disposition if it does not meet both of the criteria mentioned above. In this event, the tax situation could play out a couple of different ways…

No matter what, the spread is taxed at ordinary income tax rates in a disqualifying disposition. If the holding period of the stock is less than one year after exercise, any gain is also taxed at your ordinary income tax rate (short-term capital gain). In less common situations, the holding period could be more than 1 year from exercise, but less than 2 years from grant – in which case the spread is still taxed at ordinary income tax rates, but any gains would get long-term capital gains treatment.

Will I owe Social Security and Medicare taxes when selling ISOs?

Social Security and Medicare (FICA) taxes are NOT owed on ISOs when they’re sold, regardless of whether it’s a qualifying or disqualifying disposition. So you only have to worry about federal and state taxes (if you live in a state with income tax).

As described above, you may encounter ordinary income tax AND/OR capital gains taxes at the point of sale.

What are the pros/cons of an early exercise (if available)?

If your employer allows for early exercise (not all do), it is worth evaluating whether it makes sense in your situation! The ability to exercise the options before they even vest comes with potential advantages, but you should be aware of the possible downsides too.

The main reasons to consider an early exercise

- You may be buying the stock when the strike price is the same as the FMV or the difference is very slim. This means that the income included in your AMT calculation is $0 or close to it – potentially helping to reduce or avoid any tax impact at exercise.

- Early exercise starts the clock on your holding period, speeding up the time it takes to achieve a qualifying disposition and for applying long-term capital gains tax to the full gain.

- For those at a company eligible to be classified as a qualified small business, it starts the clock on their QSBS holding period – which can lead to some rather dramatic exclusions on capital gains.

- You’re especially confident that the company will perform well.

The main pitfalls of an early exercise

- It’s a very early bet and the company might not make it.

- It will likely be hard to dispose of your shares for some time. The company is private and it’s hard to know when a liquidity event will come around.

- It requires a fully cash purchase, so you need to have the savings available to part with (unless you finance it).

- Early exercise does NOT change the vesting schedule of the ISOs. So you still have to stick around to collect them. If you were to end up leaving the company before all the shares vest, the company could buy back any unvested stock that you exercised early.

Remember from Part 1 that an early exercise requires filing an 83(b) election within 30 days of the exercise.

How should you cover the tax liability associated with selling stock acquired through an ISO grant?

If ISOs work out and make you money, you’re going to have to pay taxes. But remember that there’s no default tax withholding when you sell the shares, and failing to pay enough taxes during the year could result in a penalty from the IRS. They like getting what they’re due when it’s due. To know what “enough” is, you need to calculate what’s called your safe harbor threshold, which can be figured one of two ways:

- 100% of last year’s total tax bill (or 110% for those with an AGI over $150k)

- 90% of the eventual tax bill owed for the current year (more difficult to know)

If any tax liability generated from selling ISO shares pushes your total projected tax for the year over the safe harbor amount, you need a plan to pay the tax on that income as it’s received. We recommend either paying estimated quarterly taxes or increasing the withholding on your regular paycheck by updating your W-4 to cover the tax gap.

What ISO-specific tax documents and forms should you be on the lookout for?

Come tax time, your life will be much easier if you know what paperwork to gather. There are also a couple pages in the tax return that you’ll need to be sure to complete if you sold company stock.

What you’ll need to help you prepare your taxes

- W-2

- This one shouldn’t be anything new. Just know that if you had a disqualifying disposition of ISOs, the income generated from that transaction will be included in the amount in box 1.

- This is sent to you by your employer.

- Form 3921

- This form contains information for any ISO exercise.

- It’s provided by your employer (or possibly a broker, or 3rd party).

- Form 1099-B

- This includes details about any sale of stock and the associated capital gains/losses.

- You’ll get this form from the custodian that holds the account the stock was in.

Forms to fill out on your tax return

- Form 1040

- This should look familiar. It’s the first page of the return and reports your income for the year.

- Schedule D

- This page reports the total gains and/or losses from the sale of stock during the year.

- Form 8949

- This is used to list out the specifics of each stock sale.

Wrapping It Up

Don’t let the tax intricacies of ISOs keep you from taking advantage of them in the most optimal way! There is potentially a lot to be gained, but it starts with taking the time to understand all the rules. Lastly, stay tuned for the final post in this 3-part ISO series, which will revolve around decision-making strategies and tie it all together.

Still have questions? Keep up with our latest insights by subscribing to our monthly newsletter. Or reach out!

Eddy Jurgielewicz, CFP® is a Partner and Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.