RSUs are an increasingly familiar form of equity compensation these days. When handled well, they can be a true boon to your financial plan – expediting progress toward major goals and having the potential to change your life for the better.

In our work, we’ve had the fortune of seeing this play out in a variety of scenarios, allowing clients to:

- Quickly pay down debts

- Pay for an international vacation

- Max out tax-advantaged retirement accounts

- Top off the down payment for that dream home

- Purchase an engagement ring and pay for the wedding

- … and more!

But to experience the optimal impact with RSUs, a few things are absolutely necessary. You need to:

- Understand what they are

- Have a framework for deciding what you’ll do with them

- Proactively prepare for the tax implications

And that’s exactly what we’ll cover here. So top off that cup of coffee and strap in!

PART 1: WHAT ARE RSUs?

An Overview

Restricted Stock Units (RSUs) are batches of stock in the company you work for. They are given (“granted” or “awarded”) to you over an established period of time, before which they are… restricted! RSUs are typically found at public companies and are ultimately a form of incentive compensation. Instead of the employer saying, “We’ll pay you more cash via your paycheck,” they’re saying, “We’ll give you some shares of our company stock and then you decide what you want to do with them”.

Vesting

RSUs create a nice carrot at the end of a stick in that you have to stay with your employer long enough if you want to realize the benefit. Upon being awarded a grant, the shares aren’t yours right then and there – bummer. Rather, they’re restricted up until a point at which “vesting” begins. Vesting refers to when you will actually start receiving ownership of the stock units (we’ll look at a sample schedule shortly).

In the event you do leave the company or are terminated, you typically won’t receive the remaining number of unvested RSUs. But you will keep the shares that have already vested before that time.

Review the paperwork

If you receive RSUs as equity compensation, then all the nuts and bolts of the award will be spelled out in a grant letter – which is provided by HR. This will provide the specifics on the number of shares to be awarded, the vesting schedule, what happens to unvested shares upon departure from the company, plus tons of fun jargon and legalese. It’s critically important to review this information so that you can be crystal clear on what to expect.

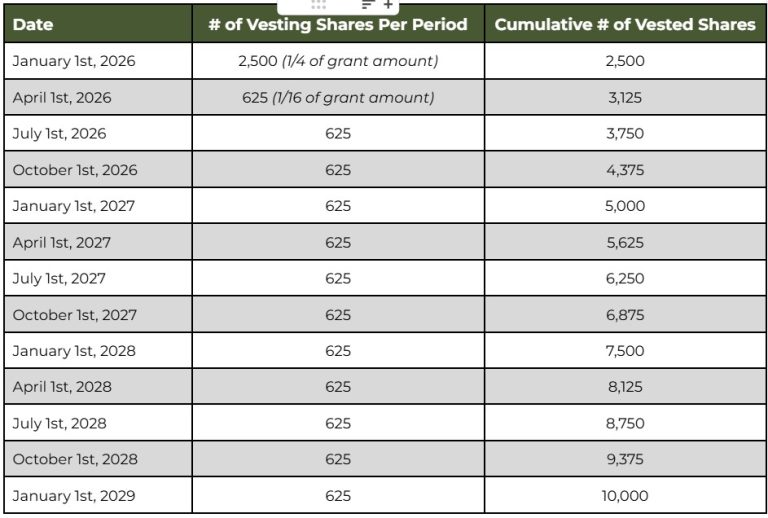

A Vesting Schedule Example

Let’s say Darrow is awarded a grant of 10,000 shares in his company, The Rising Industries, on January 1st, 2025. The vesting schedule is over 4 years with a 1-year cliff, and shares will then vest quarterly after 1 year. This would look as follows:

~ Jargon Break ~

A “cliff” is very common and means the vesting date for the first chunk of shares is delayed until after a specified period of time, typically 1 year. Then, the remaining shares will often vest more frequently from there (such as monthly or quarterly). In Darrow’s case above, no shares were vested at all until after a full year.

PART 2: DECISION-MAKING

Alright, now that you understand what RSUs are, it’s time to think about how you’re going to utilize this resource… Once they vest, it’s game time, and there are 2 things you can do upon gaining ownership of the company stock. Ideally, there’s already a strategy in place before this happens to help them support your goals as effectively and seamlessly as possible.

A Mental Framework for RSUs

It’s perfectly normal for people to get analysis paralysis with RSUs and hesitate when the time comes for a decision. To get the gears turning in the right direction and guide your thought process, I suggest asking yourself the question:

“What would I do if my employer gave me a cash bonus for this amount (the dollar value of the vesting shares)?”…

Your 2 Options at Vest

Hold onto the shares...

- Once the stock vests, you can choose to keep them as is – maintain the shares in your company stock. Doing this is essentially saying, “If I were given this value in a lump sum of cash, I’d turn around and use the entire check to buy stock in my company.”

- It’s worth emphasizing here that inaction with RSUs is still an active decision in regards to your financial plan.

- Even if you plan to sell the shares at a later date, you’ve now taken the bet on your company and will ride the movement of the stock price for better or worse.

Sell the shares right away...

- Alternatively, you could sell the shares at the earliest opportunity. Going this route opens up the conversation for using that cash for some other purpose within your greater financial plan – be it adding funds to savings, investing those dollars in a diversified portfolio, paying down debt, etc.

Again, RSUs are simply a type of compensation in the form of equity. The employer is committing to paying you with company stock in place of cash. As such, it should be thought about in the same vein – as if you were receiving a cash bonus for the amount of vesting shares. This mindset can simplify the process of evaluating what the next steps would be after receiving shares.

I find that very few people are quick to say they’d want to invest all that money back into their company stock. Instead, most prefer to find another – more practical – use for those resources.

You Should Definitely Consider Selling the Shares at Vest if ANY of the Following Apply:

You…

- Have high-interest debt balances

- Are still short of an adequate Emergency Fund target balance

- Have major unfunded short-term cash needs within the next 1-3 years (think: house down payment or repair, car replacement, etc.)

- Could use the income to contribute to tax-advantaged retirement accounts that your normal cash flow otherwise wouldn’t allow for

- Are not comfortable with higher levels of risk in your investment portfolio

- Are still working to get on track with your long-term financial independence goal

- Would miss that money if it went to $0

- Already have sizeable exposure to your company stock through other means

It May Be OK to Consider Holding Onto the Shares at Vest if All of the following apply:

You…

- Have adequate cash buckets in place

- Are already on schedule for meeting all your short and long-term financial goals

- Are comfortable with, and have capacity for higher levels of investment risk

- Wouldn’t miss the money if the share price went to $0

- Understand and are ok with the potential for paying income tax on a value you may never realize

A mix of the two options is possible as well… It doesn’t have to be all or nothing. If you understand the pros/cons and how the decision will affect your specific situation, you may choose to sell some of the shares and hold onto a portion, as long as you still check all of the boxes in the second list above.

The Risk of Accumulating Too Much Company Stock

Concentration is a helpful tactic when your spouse is giving you a list of things to pick up at the store. But concentration can be quite risky when it comes to your investment portfolio.

Without paying much attention, you could accidentally amass a rather large amount of stock in your company thanks to RSUs. Some questions worth asking yourself if you realize this has happened are:

- Are you willing to tie your list of future financial goals directly to the success of your company stock price?

- What would be the impact on your plans if the value of your shares were to suddenly go to zero?

If you find yourself in a position where you’ve already vested a lot of RSUs over the years and they’re still sitting there, it is worth reflecting on your tolerance and capacity for investment risk – then putting together a tax-mindful strategy to diversify out of your highly concentrated company stock over time.

Trading and Blackout Windows

Many companies have certain times of the year when you CAN and CANNOT sell your company stock, due to rules around insider trading. It’s not uncommon for the vesting of RSUs to coincide with a blackout window, during which you’re prohibited from selling any shares. If this happens to be the case for you and your plan is to sell the RSUs at vest, it requires an extra step.

You should take note of when your trading window will open back up and mark it on your calendar so that you’ll remember to go back in and sell at the earliest permissible time. Forgetting to do this could result in accidentally holding the shares longer than you may have wanted.

Don’t Forget About What Comes Next!

If you do sell the shares at vest, there will still be planning to follow! That cash will need to be deployed into your financial framework… Make sure you take the next step to direct the proceeds into their new home within your plan.

PART 3: TAXES

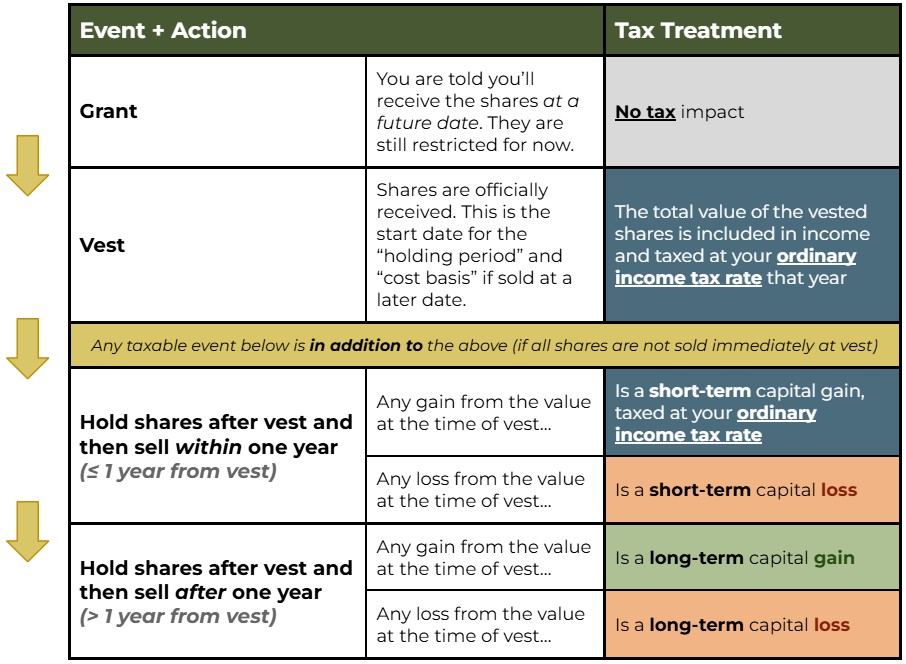

Now for everyone’s favorite part! No matter what you do (or don’t do) with the RSUs after they vest, there are going to be tax impacts.

Income Tax Treatment of RSUs

The main thing to know is that the market value for a set of RSUs (# of shares x stock price) is added to your annual income on the day that they vest. This means that the value of the vesting shares is taxed at ordinary federal and state income tax rates right away – even if the shares aren’t immediately sold. Applicable Social Security, Medicare, and Medicare surcharge taxes are owed as well. To drive it home… this is the case whether you hold onto the shares or sell them.

Withholding Rates

It is normal for employers to withhold income taxes owed on RSUs for you. They do this by selling some of the shares on your behalf upon vesting, using the proceeds to pay the tax. There are default rates (for “supplemental income”) that are used to determine how much is withheld, as follows:

Federal...

- Taxes are withheld at a rate of 22%. If you earn over $1 million, the default rate is 37%.

States...

- Have their own set flat rates for supplemental income that are applied to RSUs. For example, California’s rate is 10.23% and some states – like Louisiana – have no supplemental withholding rate even though there is a state income tax.

FICA...

- Tax rates are the same as your other income.

This gets “fun” because your actual income tax rate almost certainly differs from the default withholding rate, meaning we come across plenty of situations where taxes are some combination of over- and/or under-withheld for federal and/or state. Behind deciding whether to hold or sell RSUs at vest, this is one of the most common things that trips up clients out there. The withholding discrepancy goes unnoticed, and then April delivers a big surprise…

In all cases, proactive tax planning throughout the year comes in clutch to manage this and avoid those unexpected shocks to the bank account courtesy of the IRS and your home state.

Filling the Tax Gap

If we project an under-withholding because the default supplemental rate is insufficient, we work closely with our clients on a plan to cover the difference. This can be done in one of a handful of ways:

- Ask your payroll department if they can change the withholding rate specifically on your RSUs to a custom percentage (not all employers will facilitate this)

- Adjust your W-4 to have more money withheld from your regular paychecks

- Pay estimated quarterly taxes

- Set funds aside in a dedicated high-yield savings account to pay the lump sum tax bill in April (as long as we’re not worried about falling short of safe harbor thresholds)

If you’re going to “try this at home”, the IRS has a tax withholding estimator you can use to get an idea of what your federal situation may look like. It will finish by giving you suggested guidance on updating your W-4.

Capital Gains Tax

But wait, there’s more!

At the time that RSUs vest – if the shares are not all immediately sold – it starts the clock and sets the cost basis for any shares that may be sold at a later date. From this point forward, the vested RSU is treated like any other stock that’s purchased under usual circumstances, meaning that any growth or loss beyond that point will receive the appropriate long-term/short-term capital gain/loss treatment.

~ Jargon Break ~

“Cost Basis” is what the IRS considers the amount you paid for an asset (in this case, the stock). They need to know this because if you later sell an asset, you will be taxed on any growth you realize. When you eventually sell the stock, the “gain” or “loss” is determined relative to that “cost basis”. In the case of RSUs, you are NOT purchasing the stock. Nonetheless, the IRS will use the value of the company stock on the day it vests as the “cost basis” to assess any taxes on growth from that point if you choose to hold onto it (or to record any losses).

Key takeaway: There is no tax benefit to holding onto RSUs after they vest.

Another Common Mistake – Misreporting Cost Basis on Your Tax Return

In addition to withholding snafus, the most frequent tax-related mistake we see with RSUs is the incorrect reporting of cost basis on tax returns. Let’s break down what I mean here by bringing back our friend, Darrow, of The Rising Industries…

Let’s say that Darrow vested $10,000 worth of RSUs this year and immediately sold them all. As we now know, his “cost basis” would be $10,000 → the value of his shares in The Rising Industries at the time of vest.

Regarding his taxes on these RSUs...

- $10,000 was added to his “ordinary income” for the year, meaning he’ll pay regular federal and state income taxes on that amount just like the rest of his earnings.

- Because he sold them all right away, there are no capital gains/losses to factor in.

Where this gets tricky...

- It is up to YOU, the taxpayer, to properly report the “cost basis” of the vested RSUs on your tax return.

- The custodian (investment company that facilitates your RSUs) will provide you a tax form called a 1099-B, which gives information on stock sales you made. And because they aim to make your life difficult, the cost basis on this document will probably show as $0…Which is incorrect!

- Now, if you were to write $0 as the cost basis for your RSUs when completing the tax return, this would create a DOUBLE tax situation → you would pay ordinary income tax on the $10,000 that vested PLUS capital gains taxes on the difference between $0 (supposed cost basis) and $10,000 (amount you sold them for).

So, how do you fix this...?

- Your custodian (E*Trade, Fidelity, etc.) will also make a document called a “Supplemental Information” sheet available. MAKE SURE TO GET THIS.

- This document will list out the correct cost basis information for your RSUs. You’ll need to use this to properly report it on your tax return to avoid the potential double taxation.

If you made it to this point, I applaud you. That was a doozy… But hopefully you’re leaving with more than you started with!

As with all types of equity compensation, the right understanding and coordination can make RSUs a game-changer for you. Ensure you have a working strategy in place to optimize them for your unique goals!

Eddy Jurgielewicz, CFP® is a Partner and Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.