As if you didn’t already have enough things to consider when thinking about your child’s future, another ball has been tossed your way to mentally juggle. Enter the Section 530A “Trump” Account.

Kind of like that one friend whose entire identity is siestas and super late dinners after spending a few weeks in Barthelona… This new-to-the-scene account walks and talks a lot like a Traditional IRA, but there’s no denying it has another identity hiding beneath the surface.

In this post, we’ll get under the hood of this new account option for your child to answer: “How does it work?” and “Should you open one?”.

What Are Trump Accounts & Who Can Open Them?

In short, Trump accounts are retirement accounts for kids. Born out of the OBBBA in 2025 their true purpose is to invest money for your child to tap into decades into the future. An account can be opened for any beneficiary (the child) with a SSN, who is younger than 18 for the duration of the calendar year in which it is established.

Since the child is a minor, an “authorized individual” other than the beneficiary handles opening the account and managing it. This person can be – in the following order of priority – a legal guardian, parent, adult sibling, or grandparent.

How Do Trump Accounts Work?

There are two distinct “phases” to Trump accounts. The first is called the “Growth Period”, though I find this to be somewhat misleading since the account balance doesn’t have to stop growing after this phase is complete. Then, there’s what comes after the Growth Period.

Growth Period

This time period begins when the account is established and ends on December 31st of the year in which the child turns 17. It’s during this time only that contributions can be made and distributions are generally not allowed.

Only certain investments can be utilized in the Growth Period. They must be a mutual fund or ETF that tracks a US equity index, cannot use leverage, and have fees of 0.1% or less. Unlike IRAs, there is no requirement that the beneficiary have earned income in order for contributions to be made to Trump Accounts. And if the child is able to contribute to an IRA separately (thanks to having some income), TA contributions won’t count agains their annual IRA contribution limit.

There are four types of contributions that can be made to Trump Accounts:

Direct Contributions

These are made by any individual and have an annual limit of $5,000. They must be depsoited by the end of the calendar year (12/31) and are always made with “after-tax” dollars (meaning the beneficiary won’t pay taxes on these same dollars again, just the growth). Lastly, these contributions are considered a gift for gift tax purposes.

Employer Contributions

Employers of a parent whose child has a Trump Account may choose to make contributions of up to $2,500 per year, which does count toward the $5,000 direct contribution limit mentioned above. The limit is per employee, not per dependent or account.These are made with “pre-tax” dollars (the beneficiary will pay taxes on this contribution amount + any growth upon withdrawal).

Pilot Program Contribution

The federal government has committed to add $1,000 to an account for each child born between January 1st, 2025 to December 31st 2028. This money does not count against the $5,000 direct contribution limit. It’s made with “pre-tax” dollars. Importantly, you have to opt into it when opening the account. It’s not automatically granted to your child.

Qualified General Contributions

Charitable organizations or government entities may elect to contribute to the accounts of children based on a specified geographical location and age. There is no annual limit on these contributions and they also don’t count toward direct or employer contribution limits. Similar to Employer Contributions, these are also made with “pre-tax” dollars. An example of a QGC is the Dell Foundation’s donation of $250 to all children age 10 and under living in ZIP codes with a median income of less than $150,000.

After the Growth Period

Beginning on January 1st in the year the beneficiary turns 18, the Growth Period is over. From here on out no more contributions can be made to the account and distributions can be taken, if desired. But remember, the money doesn’t necessarily stop growing (it can continue to be invested). Ultimately, the child has 4 options:

- Keep it as a Trump Account

- Wait for penalty-free withdrawals after age 59 ½

- Pay income tax upon making withdrawals on any “non-basis” (pre-tax) dollars

- Withdraw the money

- Pay income taxes + a 10% penalty on any non-basis balance

- Pay only income taxes on non-basis balance when a 10% penalty exception applies

- Roll the funds into a Traditional IRA

- No taxes are paid or penalty due

- Convert the funds over to a Roth IRA

- Pay income taxes on the non-basis balance

- No 10% early withdrawal penalty due

Let me reiterate: the child has 4 options… It is now entirely up to them what they want to do with the money. At the age of 18, they become the owner of the account.

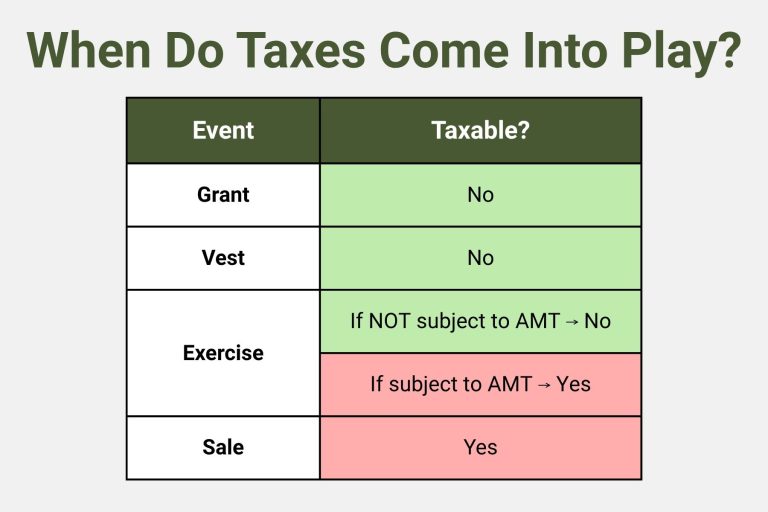

Taxation of Trump Accounts

From a tax standpoint, standard IRA rules generally apply moving forward. Specifically, the taxable portion of any distribution is included in ordinary income. A 10% early withdrawal penalty is also assessed before age 59 ½, aside from a few exceptions such as for education, first time home purchase (up to $10k), etc.

Be aware that, if any Direct Contributions were made, there will be a mix of pre-tax and after-tax money in the account, so it’s critical to keep track of the “basis” (the amount that represents already-taxed dollars). If no Direct Contributions were made, the entire balance will be pre-tax. In other words, taxes are owed on every dollar that comes out.

Growth in the account is tax-deferred at the federal level. However, some states are planning to tax earnings in the account each year. It’s also TBD whether or not states will tax employer and/or qualified general contributions.

Trump Accounts & Roth Conversions

Good tax planning aims to reduce your lifetime tax bill. Sometimes, that means voluntarily creating more income in years of relatively lower earnings (or no earnings) to pay taxes on those dollars at a lower rate than you otherwise would in the future. It’s quite possible that when a beneficiary becomes the owner of their Trump Account, or soon after, this will be their exact situation. If so, converting the balance to a Roth at that time may be rather compelling.

One very important notice: Don’t forget about the kiddie tax!

The kiddie tax comes into play when the…

- Child is under age 18 at the end of the year

- Child is 18 years old with earned income that is less than or equal to ½ of their support

- Child is age 19-23 and a full time student, with earned income that is less than or equal to ½ of their support

Under these rules, the first $1,350 of income is tax free, the next $1,350 is taxed at the child’s rate, and the remaining income is taxed at the parents’ rate.

Therefore, a Roth conversion is likely to make the most sense once the kiddie tax is no longer applicable. Lastly, there must be a plan for how the taxes will be paid on the conversion.

Should You Open a Trump Account for Your Child?

Can Your Child Get Free Money?

As we’ve covered, there are multiple ways your child could receive funds in their account from another source. Whether it’s the $1,000 pilot program, $250 from the Dell Foundation, another future qualified general contribution, or employer contributions, free money is free money. So if they can get it, take it. Simple as that.

What About Contributing Your Own Money?

It comes down to evaluating the priorities you have for the money that’s being put to work for your child and targeting the most optimal account for that goal.

- Primarily focused on helping to pay for their education? Then a 529 and/or regular old brokerage account (owned by you) are going to serve you better.

- Want to build a flexible resource for them to access for various milestones throughout their life, but before retirement? A brokerage account (owned by you) and/or a UTMA/UGMA will make more sense.

- Looking to give them an early boost on retirement and your child has earned income? Start by setting them up with their own Roth IRA.

If you’ve already checked these boxes, or they don’t pertain to your situation, then go ahead and weigh putting your own money into a Trump Account for your child’s future. Again, it is best positioned for your child to use after they turn 59 ½.

Prepare Them for the Money & the Decisions

The lump sum suddenly at their fingertips, facing off against some vague idea of very delayed gratification… A potentially complicated situation with both taxable and nontaxable balances comingled in the same account… Possible early withdrawal penalties… A menu of options for what to do next, if anything… It’s a lot for anyone, let alone an 18-year-old!

If you open a Trump Account for your child, it’s crucial to communicate with them well before they reach their account owner status. Educating yourself, and them, is sure to facilitate more beneficial outcomes in the long-term.

How Do You Open a Trump Account?

There are two ways to set up an account. You can either file Form 4547 with your tax return or visit trumpaccounts.gov. The program is slated to launch July 4th of this year. Accounts will initially be opened at BNY and Robinhood, through a designated partnership. Later on, you should have the ability to roll it into a Trump Account at another custodian.

Frequently Asked Questions About Trump Accounts

Q1: What is a Trump Account?

A Trump Account is a Section 530A investment account created under the OBBBA that allows money to be invested on behalf of a child before age 18. The account is designed to function similarly to a retirement account, with restrictions on contributions, investments, and withdrawals.

Q2: Who is eligible for a Trump Account?

Any child with a Social Security number who is under age 18 during the calendar year the account is opened may be eligible for a Trump Account.

Q3: Does a child need earned income to have a Trump Account?

No. Unlike an IRA, a child does not need earned income for contributions to be made to a Trump Account.

Q4: What investments can be held in a Trump Account?

During the Growth Period, investments are generally limited to qualifying U.S. stock index mutual funds and ETFs that meet specific fee and leverage requirements.

Q5: Can Trump Account funds be withdrawn before retirement?

Yes. Once the Growth Period ends, the beneficiary gains control of the account and may withdraw funds, although taxes and potential penalties may apply depending on how the money is used.

Q6: Can a Trump Account be converted to a Roth IRA?

Yes. Funds can generally be converted to a Roth IRA, although income taxes may be due on any pre-tax balance converted.

Q7: Is a Trump Account better than a 529 plan for education?

Not necessarily. A 529 plan is typically more effective for education savings, while a Trump Account may be better suited for long-term retirement-focused savings. The best option depends on your family’s goals.

Eddy Jurgielewicz, CFP® is a Partner and Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.