Are you planning on donating to a charitable organization this year?

If so, you may be able to take advantage of some helpful tax strategies – in addition to supporting your desired cause.

So You Want to Give to Charity… What Gives?

At Upbeat Wealth, we love working with households that prioritize giving. Many families we serve are eager to put some of their resources into action for the community. This, alone, is awesome. Goals like this excite us as planners and motivate us to do what we do. So before we move on, I want to be clear that the way we view it, the primary goal of giving should be to provide those resources to an effort that’s important to you. The benefit is in doing good. Full stop.

Now, there is a potential secondary benefit to charitable giving, which we’ll discuss here. It’s an afterthought—a cherry on top—but not the leading reason we believe people should make donations. As with many things in our world, it has to do with… taxes!

The IRS’ Gift to You

The added available benefit (secondary to lending that neighborly hand to those in need) comes in the form of a tax deduction.

Bear in mind that a tax deduction is something that reduces the portion of your income which is subject to tax. The idea here is that it then reduces the amount of taxes you would pay for the year. This is different from a tax credit.

By giving money to a charity, the IRS lets you take a deduction against your income for the value of what you give in that tax year, up to a certain limit.

A very important qualifying detail here is that this advantageous deductibility factor only really enters the conversation if it will help you itemize at a level over the standard deduction threshold (whether alone or combined with other itemized deductions). The standard deduction in 2025 is $15,750 for individuals and $31,500 for those filing MFJ. So, as an example… If you’re a married couple who is making charitable contributions this year and this helps get your itemized deductions above $31,500, then you’re probably in a spot to capture this extra tax perk.

A couple rules

- Currently, if you give cash, you’re able to deduct your gift amount up to 60% of your AGI for the year. If you donate an investment, that limit is 30% of AGI.

- Additionally, you need to make sure the organization qualifies for tax-deductible charitable contributions. It must be a US-based 501(c)(3). The IRS provides a tool for checking this.

But Wait, There’s More!

Of all the ways one can donate, cash and invested securities are the two most common methods we see. A “cash” contribution is your classic check written to the name of the organization or maybe you enter your credit card information on their website. Alternatively, someone can choose to donate an investment they own – such as stocks, mutual funds, or ETFs.

If your charitable giving goal is enough to allow for a beneficial deduction, then we’ll want to consider some further possible tax strategies (that’s right, there’s more!) – one of those being whether it makes more sense to give investment assets instead of cash.

Give Your Giving a Bigger Boost

Now here’s the kicker for donating that investment… When you do so, you are not selling the investment yourself. You give it away and then the nonprofit sells it. Therefore, you don’t have to worry about paying any taxes on the gains. Under normal circumstances, you have to pay “long-term capital gains” taxes on the growth of an investment when you sell it (assuming it was held for over 1 year). For many people we work with, the tax rate is either 15% or 20%. Because of this, you’re increasing your gift vs. selling the stock and donating the after-tax proceeds.

Additionally, you’re able to take a tax deduction for the full fair market value of the asset on the day that you donate it (up to an annual limit of 30% of your AGI). Let’s take a closer look at this with an example…

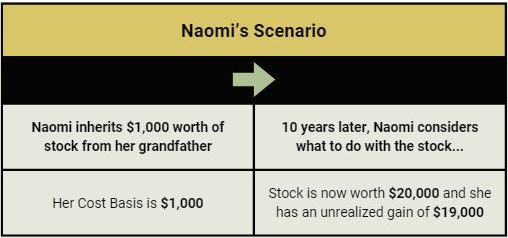

An Example

When Naomi was 23 years old, she inherited a taxable account from her grandfather consisting of a single stock. Her cost basis upon receiving the stock was $1,000 (the fair market value at that time). She’s now 33 years old and still owns the stock, which has jumped in value to $20,000.

Naomi is single, earning an income of $300,000. She’s in the 35% federal tax bracket and has a 15% rate for long-term capital gains + is subject to the 3.8% net investment income tax. She has also decided to begin donating $20,000/year to her favorite local nonprofit, which she could comfortably do from cash flow if she wanted.

She wants to determine the most optimal way to make her donation this year.

naomi checks the key boxes for us to consider some enhanced tax strategies...

☑️ She plans to donate to a qualified 501(c)(3c).

☑️ Her intended giving level will get her to an itemized deduction amount ($20,000) that is more than what her standard deduction would be ($15,750).

☑️ She has a “long-term” asset in a taxable account.

☑️ The investment has appreciated in value.

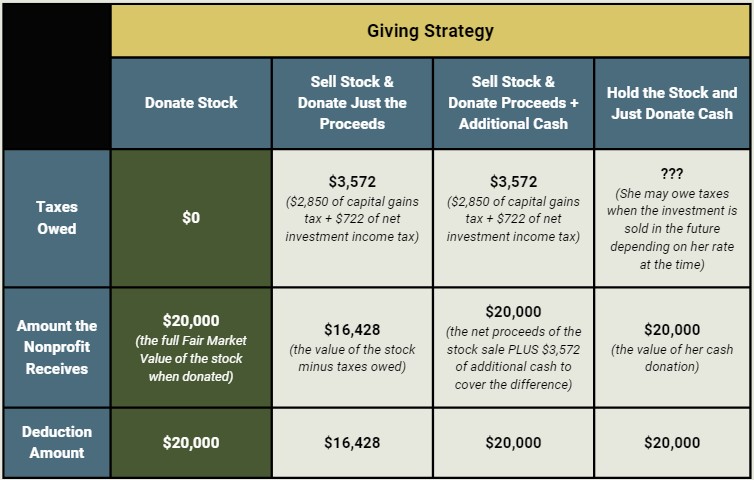

As such, we’ll want to explore the opportunity of donating her stock instead of cash.

it makes a lot of sense to donate her stock to the nonprofit instead of cash

In doing so…

- She provides the intended level of financial support to charity.

- She avoids paying capital gains taxes on the stock that she donates.

- She won’t have to worry about dealing with capital gains taxes on this investment at some point in the future (which she may have to if she continues to hold onto it).

- She can take a $20,000 itemized deduction for the gift on her taxes (the full fair market value of the stock on the date she donated it).

- Since she already has the free cash flow available, she can then use that money to buy into a diversified investment portfolio that helps support her greater financial plan – essentially replacing the investment value of the donated stock. This new investment will have a substantially higher cost basis than the gifted stock ($20,000 vs. $1,000) – which can help reduce potential capital gains taxes down the road.

Donating the stock is the ONLY strategy that allows her to be certain of paying $0 in taxes on the disposition of the stock and get a full $20,000 deduction in the current year.

Some Common Situations Where This Can Make a Lot of Sense…

Other examples of scenarios in which you may find yourself with a similar opportunity include:

- You purchased an investment yourself several years ago. It’s been sitting around but doesn’t entirely fit in with your current investment strategy.

- You have accumulated vested RSUs or exercised stock options that haven’t been sold yet.

- Someone gifted you stock, or another investment in the past.

- A parent or other family member opened and funded a custodial account (UTMA/UGMA) for you when you were younger. You’re now the full legal owner of the account several years later.

- You are overly concentrated with a certain investment inside of your taxable portfolio.

- You have an old mutual fund with relatively high expenses.

- Maybe you just have some nice gains in your diversified portfolio and want to take them off the table in a tax-efficient way.

So You’ll Donate Investments – But How Do You Even Do the Thing?

Directly to the organization...

In some cases, you may be able to arrange to send your stock or other investments directly from the custodian that holds your account. Not all charitable organizations are set up to receive your stock, mutual fund, or other investment. So you’ll want to check that first. If they are, it will involve some paperwork and coordination between them and your investment custodian.

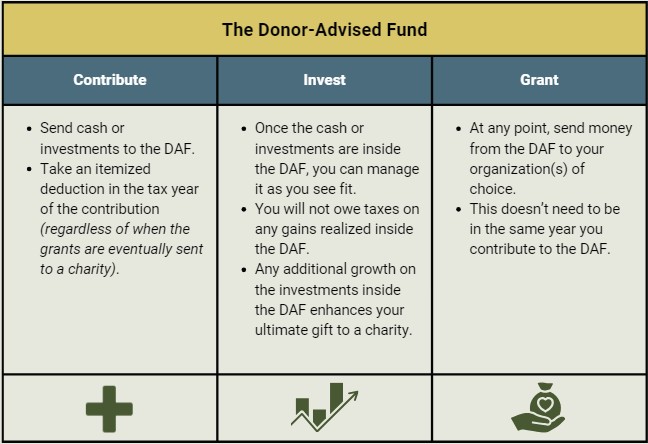

donor-advised fund...

The Donor-Advised Fund presents a flexible way to facilitate your giving strategy. It is a type of investment account that is facilitated by a 501(c)(3) public charity – you will recognize them as independent flavors of major custodians, such as…

… to name a few. When you contribute cash or investments to a DAF, you are literally giving money to a charitable organization at that point, thus allowing you to take a deduction for the DAF contribution in that tax year. However, you’re able to manage the assets inside the DAF as you see fit. This gives you the chance to grow your eventual impact even further. Additionally, you’re not taxed on any gains inside the account. Be aware that – if your investments do increase – that doesn’t impact your tax deductibility. The tax deduction is simply based on the value of what you put into the DAF on the date you do so. Then, you can choose to make grants from the DAF to your organization(s) of choice at any point down the road. These grants don’t need to occur in the same year you contributed to the DAF.

you might consider a donor-advised fund if:

- Your organization(s) of choice do not readily accept direct gifts of invested assets. If you donate the asset to the DAF, you can take a deduction for the full FMV on the date of the contribution. Then, the DAF can sell the investment (no tax impact on you) and send a check to your selected charity.

- You’re ready to take the tax deduction but want to give the cash/investment more opportunity for growth before ultimately granting it to the designated organization.

- You want greater flexibility on when and how you distribute grants.

- You want to streamline a bigger-picture philanthropic strategy.

Things to be aware of with donor-advised funds:

- Some have minimum initial contribution requirements

- They may have a minimum grant amount

- They are likely to have administrative fees (0.6% is typical)

If You Plan to Donate an Investment, Avoid Doing The Following

- Donating an investment that has lost value.

- It’s better to sell the investment first, take the deduction for the capital loss, and then donate the cash to charity.

- Donating an appreciated investment you’ve held for a year or less.

- It’s possible to donate an investment you’ve held for a year or less (at a “short-term capital gain”), but you’re not able to take a tax deduction for the full FMV. Instead, you can only deduct the cost basis (what you paid) minus what you would have owed in taxes for the gain on the investment.

- Remember that donating an appreciated long-term asset allows you to deduct the full FMV at the time of the gift.

Ask Yourself These Questions to Determine if Donating an Investment is Worth Exploring

- Are you already donating to charity, or are you planning to do so this year?

- Do you have any long-term (held longer than 1 year) investments in a taxable account?

- Have those investments appreciated in value?

- Will your charitable contributions plus other deductions put you in a place to itemize over the standard deduction?

- Extra Credit: Do you have the available cash flow to replace the investment(s) donated from your brokerage account?

- This one is not necessarily a must but can be a nice element.

- It could be in the form of monthly cash flow, bonus pay, vesting RSUs, etc.

If you answer “yes” to at least #s 1-4, it’s worth looking into how this strategy fits into your greater plan.

Eddy Jurgielewicz, CFP® is a Partner and Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.