What does a financial planner reflect on in the final days before getting married???

Finances.

Ok. Sure – a couple of other things too… But it’s up there. It’s who I am.

Money + Romance = What You Make It

We’ve all heard some version of the statistic about money being a common cause of divorce… Whatever the real percentage may be, or the specific money-related issue that tips the scale – I knew I didn’t want to be in that number. So as I count down the final hours before my wedding, I find myself thinking back on the journey my partner and I have taken to navigate the financial waters together.

While I wouldn’t say it was the first thought that came to mind after she said “yes” (I was mostly consumed by relief that I got the answer I’d been hoping for and somehow managed to string together adequately coherent words), it wasn’t too long after our proposal that I started to think about how Christina and I would begin tackling finances together. I’ve been part of too many conversations with spouses who were already years into their marriage and still dealing with the heavy burden of misaligned thoughts on money. I’ve seen up close the strain it can have on a relationship when matters aren’t properly addressed early on. For me, it was critical to tackle this head-on in my own romantic partnership – so that the two of us were in control, rather than the other way around.

Now let’s lay some things out there before we get into it…

- It’s not a given that finances will be a point of distress for all couples. It may naturally work for some. But it will definitely be a matter worth giving time and attention to for most.

- People are not likely to fully change how they think about or interact with money. They will continue to have their own unique habits and mindsets that stick with them. But couples can learn how to work positively together despite such differences.

- Before any couple can begin to work through financial matters together, they MUST first work to understand the other person’s money story… Their influential memories, their emotions, any anxieties or convictions, and so on.

- Any level of judgment will make the conversations exponentially more difficult. Money is already a topic that requires substantial vulnerability for some individuals. It will never help to feel as though someone is looking down on how they handle or think about things.

More on Why I Felt This Was Important

It’s probably no surprise, but money stuff comes fairly easy to me – it’s what I do and talk about all day every day in my professional life. That’s not the case for my fiancée. She’s a psychiatrist who would rather think about most other things besides money. And while she’s a hell of a lot smarter than me, it’s just not something she enjoys devoting a lot of mental space to. Now I know that I’m going to spend the rest of my life with her and I hope it’s a long, happy one! But if I’m suddenly not around one day or lack the mental capacity, I would like Christina to feel confident enough to manage important financial affairs independently.

I’ve seen a similar dynamic in plenty of other couples too. Quite often, one partner is the “chief financial officer” of the household and makes the majority of the decisions. While I’m not opposed to a spouse taking on this role, I do believe it’s highly beneficial for the other person to at least understand what’s being done and why. Further, they should be invited to provide their input – if nothing else, given the opportunity to say, “It’s up to you”.

So it was ultimately a two-part goal…

- Learn how to weave healthy joint financial decision-making and expectations into our relationship early on.

- Ensure that both of us understand, have the chance to be a part of, and can comfortably handle the most important money matters.

Where Did Each of Us Come From?

Our socioeconomic backgrounds are quite different. I’m the son of a teacher and a carpenter, whereas she’s the daughter of a cardiologist and a mother who raised her and her five siblings full-time. I went to public school, she went to private. I carried the financial responsibility of my education and she had a college fund to take care of that. I say this simply to help illustrate that we had very unique interactions with money from a young age. As a result, we now have stark differences in how we approach financial matters as adults. I tend to stress over expenses and consider a cost for far too long while Christina generally has no issues in that department. I’m naturally more of a saver. She’s more of a spender. Neither is right, neither is wrong – we’re just different.

All that to say… if WE can figure it out, YOU can too!

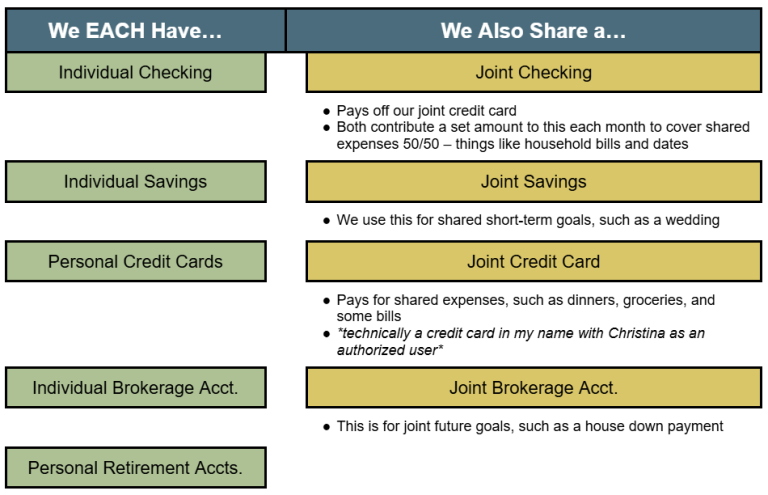

What’s Our Account Setup?

Some couples go all in on doing everything jointly. Others keep it fully separate. For us, we have things that we do together and shared hopes for the future. As individuals, we have our own preferences and unique goals. Our framework is structured to allow for money movement in both arenas.

For things we do together and use together, we’ll typically pay for those out of a shared account. For those things we do independent of the other, they come out of personal accounts. That way we can avoid any potential judgment on how the other spends their money. As long as we’re both putting the right amounts towards the things we need and want together (both for fun and necessary goals), we’re each free to spend our other personal dollars how we want.

Taking it Beyond the Accounts

The train can’t stop at simply setting up joint accounts. Opening a savings account together won’t automatically create magical money harmony. And in my mind – this is the MOST important aspect of the journey to comingle finances… It’s the process of having meaningful conversations about how to handle financial decisions together, about how you each interact with money individually, and what your future financial goals are – both those that are personal and shared. As I referenced earlier, conversations were also important to help share my financial acumen with Christina – so that she’d better understand the value of having appropriate cash savings in place, how to optimize various tax-advantaged accounts, where and why a brokerage account makes sense, even how to place trades, and so on…

I have to say, it was an especially proud partner/financial planner moment when Christina first told me she’d maxed out her Roth IRA and invested the money (without me doing it with her)!

How Did We Do This?

Money Dates!

I hear you… it doesn’t sound all that romantic to discuss finances on a date. But here’s the thing: I believe it is much easier to talk money at an agreed-upon and preset time when both parties are expecting it, rather than randomly when one person may be caught off guard. It’s helpful to protect the time too, or it may never happen. It’s easy to put things off if they’re not on our calendars. Further, making it a date can hopefully create a more enjoyable environment. Pour a glass of wine, crack open a beer, go to your favorite dinner spot… do something to set those positive vibes. Finally, limit the time. If one or both of you aren’t all that excited to have this kind of conversation at first, knowing that it will only go on for a short chunk of time might make it more agreeable.

Our approach? We decided to have one 30-minute Money Date one Sunday per month.

It’s worth mentioning that this was a very helpful method in our relationship. Part of why Christina doesn’t like to talk or think about money is that it can easily make her anxious to do so. Again, I have no issue talking about it. By putting these short time blocks on our calendar, she was way more receptive to the conversation – it was never a surprise and she knew it wouldn’t go longer than a half hour (we even cut the first few down to 15 minutes).

I want to be clear: I’m not saying this has to be the ONLY time you and your partner discuss finances. But it may be the easiest and most productive way to do so while giving it the prioritization it deserves.

The Result

As with other areas of our relationship, the work is never done. Nonetheless, I’m happy to report that – after about a year and a half – I feel great about where we are. There aren’t any issues or doubts about what our shared and individual financial expectations are. Money has not been a source of contention for us. And don’t just take my word for it! I did ask Christina what her feedback on our Money Dates and overall journey has been. She expressed that, while she was very hesitant at first and really didn’t want to have “talks about money”, it’s been extremely helpful. Now she’s far more open to discussing finances rather than pushing the topic aside.

So forget about that statistic! For us, money will be something we…

- Work on together

- Have clear expectations on

- Understand and are comfortable managing

- Discuss openly and honestly in a healthy way

- Agree on for big picture planning and household goals – even though we may interact with it differently in certain aspects of our lives

Eddy Jurgielewicz, CFP® is a Partner and Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.