Why You Should Double-Check Your 2025 Tax Return

Unlike me, you probably filed your taxes weeks ago. You know, that thing you do where you take a weekend and go all Adam Scott *severance* at your computer. Now, I’m going to ask you to try to *reintegrate* with that moment and review that return for accuracy. Whether you delegate to a CPA or file your own taxes, it’s highly possible you left money on the table. Provisions of the One Big Beautiful Bill Act (OBBBA) in 2025 might have led you to overlook certain tax deductions that differ from those in previous years. If you received overtime pay, tips, or bought a new vehicle in 2025, you could have qualified for certain savings. In addition to the legislative changes made in the middle of last year, we’ll also provide some of the more common (and easily fixable) tax mistakes we see each year.

OBBBA Tax Changes That May Not Be Automatic

This is not an exhaustive list of tax-related changes enacted by last year’s legislation. Some of those changes will automatically flow through your return. For instance, the senior bonus deduction. Individuals age 65 or older can deduct an additional $6,000 of income, and married couples age 65 or older can deduct an additional $12,000 of income from their federal taxable income if their modified adjusted gross income is less than $75,000 for individuals or $150,000 for joint filers. Because it’s age-based, tax-filing software will catch this automatically, assuming you list that correctly.

However, there are three (3) new tax deductions that your tax-filing software may NOT catch automatically and may require additional information or documentation.

Overtime Pay Deduction

Tip Deduction

Car Loan Interest Deduction

Overtime Pay Deduction: What to Know

If you receive compensation for overtime hours, most commonly “time and a half”, you are likely eligible for the overtime pay deduction unless your household income is too high, as noted below.

Overview

- Effective for Tax Years 2025 – 2028

- Maximum Annual Deduction

- Individuals: $12,500

- Married Filing Jointly: $25,000

- Income Phaseout

- Individuals: $150,000

- Married Filing Jointly: $300,000

Eligibility

- Employees with a Social Security number who are covered by the Fair Labor Standards Act and considered overtime-eligible (non-exempt).

Employer Reporting Requirements

Because of the mid-year legislative changes, employers are NOT required to itemize overtime compensation on employee W-2s for 2025. However, this is a requirement for tax years 2026 – 2028. If your employer added this to your 2025 Form W-2, it would be listed in Box 14. However, there’s no need to fret if you know you worked eligible overtime and Box 14 is blank. You can refer back to your last pay stub of the calendar year, which will provide you with your Year-To-Date (YTD) total overtime compensation for 2025.

Claiming the Overtime Pay Deduction

The most important note about claiming the overtime pay deduction is that only the overtime premium is tax-deductible, not the full amount.

Example: Jon is an individual filer with less than $150,000 of modified adjusted gross income. His normal hourly rate of pay is $30. His overtime premium is “time and a half”, and he receives $45/hr as compensation. He worked 250 hours of overtime in 2025, for a total overtime compensation of $11,250. To calculate how much he can deduct from his federal taxable income, Jon can either take his overtime premium of $15 ($45 – 30) and multiply it by the number of hours worked, or divide the total compensation of $11,250 by 3. Either way, the result is that Jon can now deduct $3,750 of his overtime pay against his 2025 federal income. Suppose Jon can deduct that amount against income in the 22% marginal tax bracket, that would save him approximately $825 in federal taxes.

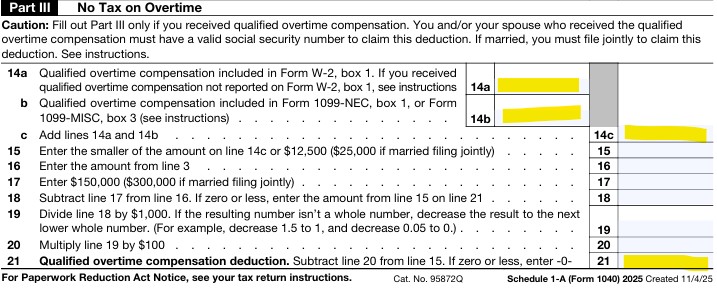

To see if the overtime pay deduction made it onto your tax return, taxpayers can refer to page 2 of their Form 1040, Line 13b. And more specifically, they should look directly at Schedule 1-A, Part III, labeled “No Tax on Overtime.” Box 14 will ask you to list your qualified overtime compensation.

So, using the example above, Jon would list $3,750 in Box 14a. This would flow through to boxes 14c and 21.

Tip Deduction: What to Know

Overview

- Effective for Tax Years 2025 – 2028

- Maximum Annual Deduction

- Individuals or Married Filing Jointly: $25,000

- Income Phaseout

- Individuals: $150,000

- Married Filing Jointly: $300,000

Eligibility

- See the IRS-compiled list of occupations that are eligible because they “customarily and regularly receive tips.”

- Tips must be voluntary and in cash or charged to a credit or debit card. They include your share of any pooled tips. One notable exception is that mandatory service charges are NOT considered qualified tips for this deduction.

Employer Reporting Requirements

- For employees, your employer is supposed to record your income from tips on your Form W-2, and this should be itemized in either Box 7 or 14.

- For independent contractors, your 1099 will likely not show tips separately.

Note that reporting requirements are a two-way street. Employees are required to maintain a daily record of cash and noncash tips and submit them to their employer monthly when the total exceeds $20 for that month. If employers allocate tips to employees in Box 8 of their Form W-2, it’s the employees’ responsibility to maintain records proving they received less income and do not owe taxes on the full amount. For self-employed individuals and 1099 independent contractors, you also have a responsibility to maintain daily records of tip income received, even though this income is not reported to the business where services are rendered. Any tips not reported by your employer on your W-2 must be reported on Form 4137 when you file. In 2026, this will be required to qualify for deducting those tip amounts.

Claiming the Tip Deduction

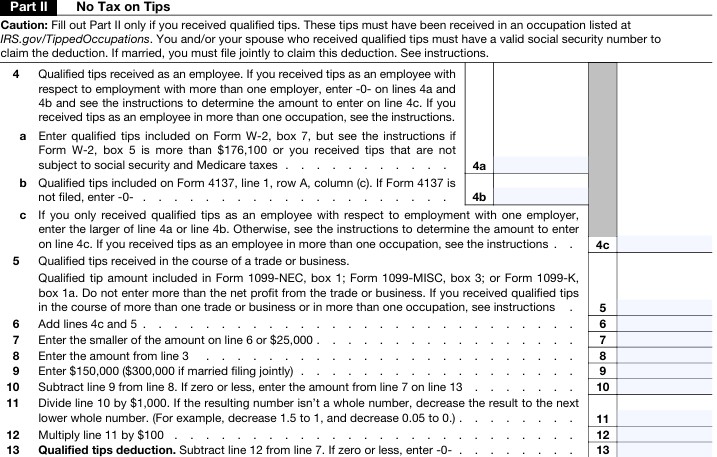

To see if the tip deduction made it onto your tax return, taxpayers can refer to page 2 of their Form 1040, Line 13b. And more specifically, they should look directly at Schedule 1-A, Part II, labeled “No Tax on Tips.”

Car Loan Interest Deduction: What to Know

Overview

- Effective for Tax Years 2025 – 2028

- Maximum Annual Deduction

- Individuals or Married Filing Jointly: $10,000

- Income Phaseout

- Individuals: $100,000

- Married Filing Jointly: $200,000

Eligibility

- Qualified vehicle purchased with a loan originated after December 31, 2024

- Must have undergone final assembly in the United States, as verified by the National Traffic Highway Safety Administration

- Vehicle must be for personal use with the taxpayer as the original purchaser

Claiming the Car Loan Interest Deduction

Taxpayers must include the VIN number. You do not need to itemize your deductions to claim the car loan interest deduction.

To see if the tip deduction made it onto your tax return, taxpayers can refer to page 2 of their Form 1040, Line 13b. And more specifically, they should look directly at Schedule 1-A, Part IV, labeled “No Tax on Car Loan Interest.”

Example: Stevie and David are joint filers with an adjusted gross income below $200,000. They purchased a qualified vehicle in 2025 for $50,000 and financed $40,000 at 5%. They paid $5,291 in annual interest. Assuming a 22% marginal tax rate, deducting this interest from their adjusted gross income would save them $1,164 in federal taxes owed.

Other Common Tax Return Errors

The remaining common errors are unrelated to the OBBBA legislation but occur all too often. These aren’t just warnings for taxpayers who file their own taxes. Remember, your CPA may not automatically identify some of these issues, as their work relies on receiving accurate documentation.

Missing Mortgage Interest (Multiple 1098s)

This is a big one for taxpayers who itemize their deductions. Each year, you’ll receive a Form 1098: Mortgage Interest Statement from your lender detailing the amount of interest you paid. But what if your lender changes mid-year because your loan was sold? You’ll now receive two (2) Form 1098s, one from your previous lender and one from your current lender. You have to submit or upload both forms to deduct the full amount of mortgage interest paid that year from all lenders, as that number does not carry over to each form!

Medical Expense Deduction

Another deduction that households that itemize can miss is in years with large healthcare expenses. Different than the self-employed healthcare deduction, taxpayers can deduct eligible expenses that exceed 7.5% of their gross income for the year. This is common in years when you have surgical procedures, undergo IVF treatments, or give birth. These expenses don’t live on any issued tax form, so you have to manually enter them or let your tax professional know.

Filing Duplicate 1099s

If you have a non-qualified brokerage account with a custodian such as Charles Schwab, Fidelity, or Vanguard, you’ll likely receive a 1099 by the end of February detailing any capital gains, dividends, and interest for the year. However, sometimes your custodian receives additional information from the fund companies that requires them to *correct* your 1099. They will then issue you a separate, corrected version of the 1099 in March. Do not upload both to your tax return! Doing so will ultimately double your tax liability as you’ll find yourself paying on duplicate information.

Misreporting Cost Basis of Restricted Stock Units (RSUs)

Upon receiving RSUs, you’ll likely have the compensation added to your ordinary income for the year on your Form W-2. However, the custodian (the investment company that facilitates your RSUs) will provide you with a tax form called a 1099-B that shows whether you sold any of your stock. The cost basis on this document will likely read $0, which is incorrect. Your custodian will also send you a document called a “Supplemental Information Sheet,” which will list the correct cost basis information for your RSUs. This sheet allows you to properly report it on your tax return and avoid any potential double taxation.

Backdoor Roth Mistakes

Mechanically, this topic deserves its own post on how to correctly make a nondeductible Traditional IRA contribution and convert it to a Roth IRA. The outputs of Form 8606, which documents this transaction, are rather simple. But for taxpayers who file their own taxes using DIY software, we see recording errors more often than not. Furthermore, making contributions and doing conversions across different tax and/or calendar years introduces an additional layer of complexity.

Excess Health Savings Account (HSA) Contributions

This isn’t a tax prep error, but rather a coordination error among spouses. When both spouses are taking advantage of their HSAs through their respective workplaces, it can lead to contributions that exceed the household IRS limit. For two (2) reasons, the first being that the combined individual limits are MORE than the household limit. The second being, if one spouse has dependents on their High-Deductible Health Plan, they may already be making the full family contribution. So any contribution (employee or employer) that is added to the spouse’s plan will also exceed the IRS household contribution limit. If you do not catch or correct this, you’ll pay a 6% excise tax year-over-year as long as the overcontributed amount remains in the account or isn’t applied to a future year contribution limit.

Filing an Amended Return

If you missed a deduction, you can file an amended return within three years to correct it and get a refund. While these are some common errors we’ve seen on client tax returns, please note this is not an exhaustive list. Always consult with your tax professional before making decisions related to your personal situation.

For helpful tools when it comes to tax planning and filing, check out the Free Resources page on our website.

Currently working? Here’s a separate, helpful guide for reviewing your 2025 tax return.

Frequently Asked Questions About Missed Tax Deductions

Q1: How do I know if I missed a tax deduction on my 2025 return?

A1: Check Form 1040, Line 13b and review Schedule 1-A for specific deductions like overtime pay, tips, and car loan interest. Compare your return against your income documents (W-2, 1099s, loan statements) to confirm nothing was overlooked.

Q2: Can I deduct overtime pay on my taxes in 2025?

A2: Yes, but only the overtime premium portion (the extra pay above your standard rate) is deductible. The deduction is subject to income limits and must be calculated manually in many cases.

Q3: Are tips tax-deductible in 2025?

A3: Qualified tips may be deductible if they are voluntary and properly reported. However, service charges do not qualify, and you must maintain accurate records to claim the deduction.

Q4: Is car loan interest deductible for personal vehicles?

A4: Under 2025 rules, yes—if the vehicle meets eligibility requirements, including U.S. final assembly and a qualifying loan. You do not need to itemize deductions to claim it.

Q5: Can I fix a mistake after filing my taxes?

A5: Yes. You can file an amended return (Form 1040-X) to correct errors or claim missed deductions, typically within three years of the original filing date.

Mike Turi, CFP® APMA™ is the Founder and a Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.