Mortgage Rate Trends

It’s no secret that homebuyers from 2023, 2024, and 2025 may be eager to refinance. With mortgage rates dropping in 2025 and expected to fall even further, you might be wondering if now is the right time. Yesterday, on September 17th, 2025, Jerome Powell announced the first 0.25% rate cut of 2025, and the Fed as a whole offered lukewarm guidance about additional cuts this year.

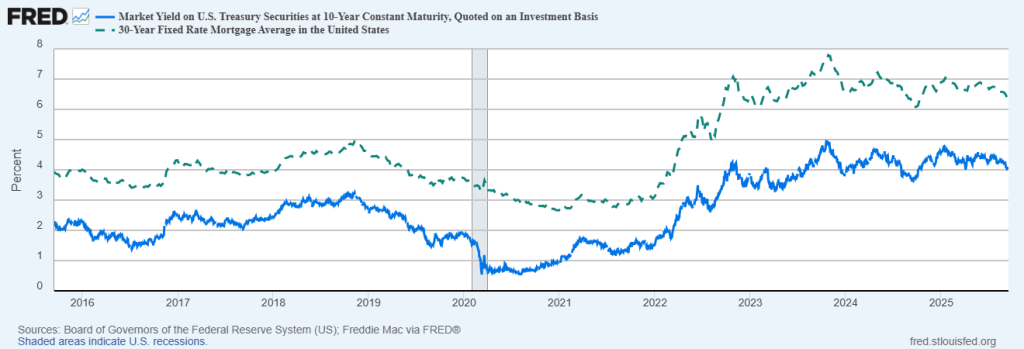

Glass half full: Right now, mortgage rates are near their lowest levels in the past three years and nearly match the lows from 1970 to 2001.

Glass half empty: They are still well above the sub-3% rates of 2020 and 2021.

Why Is Everyone Focused on the Federal Funds Rate?

One common misconception about mortgage rates is that they are directly linked to the Federal Funds Rate, which is set by the Federal Reserve. Want to learn more about the federal funds rate? Check out this explainer from Investopedia. The essence of it is that the Fed uses the federal funds rate to influence bank lending, which in turn affects the money supply available to consumers. When *cheap* money is accessible, consumers tend to invest more aggressively and spend more. If left unchecked, this can result in inflation, which increases the costs of goods and services and may even lead to financial bubbles like the one seen during the 2008 financial crisis. Following the economic stimulus triggered by Covid-19, the Fed sensed the economy was *overheating* due to the 0% federal funds rate and took steps to ease us into a “soft landing” a.k.a. a sustainable reality. A prime example of our economy starting to overheat was the surge in home values, as well as the GameStop trading frenzy, which we wrote about in an earlier blog.

What Mortgage Rates Actually Track

What’s important to know is that the 30-year mortgage rate does not move in lockstep with the federal funds rate. Just because the Chair of the Federal Reserve, Jerome Powell, announces a 0.25% rate decrease doesn’t mean the 30-year mortgage will drop by 0.25%. It’s important to recognize that determining the mortgage rate is not an exact science. There are variables, many of them. And certainly, the federal funds rate has a role.

Borrowers should consider the 10-Year Treasury as a gauge for where 30-Year Mortgage rates are headed. As shown below, mortgage rates tend to be 2 to 2.5 percentage points higher than the 10-Year Treasury yields. This then leads us to the question: if mortgage rates follow 10-Year Treasury rates, then how are 10-Year Treasury rates determined?

Enter the 10-Year Treasury Yield

If we think of the federal funds rate as an educated guess on how to best drive the economy forward and a proactive measure, then the 10-Year Treasury yield represents the market’s response and reaction to that direction. Scorsese makes the movie, and the audience must decide what to make of it. And we’ll run with the movie analogy even further.

Director = Fed Chair

Professional Critics = Fed Board of Governors

Supply and Demand = Theatrical vs. streaming release

Market Sentiment = Pre-release buzz

Inflation Expectations = Cost to see today vs. tomorrow

Term Premium = Can you afford to have the ending ruined for you?

Geopolitical Events = Actor nutjob says something they shouldn’t have

Wrap all of these together, and you have investor/consumer sentiment for 10-Year Treasury rates and renting/owning a movie!

So, Is Now The Time to Refinance?

Refinancing is decided on a case-by-case basis, depending on your current rate, refinance terms, and how long you plan to stay in the home. However, we do recommend a general rule of thumb. Are you lowering your rate by 0.50% and is your break-even point on upfront costs within 18 months or less?

The Break-Even Point

Typically, refinancing your mortgage comes with an upfront cost. And while that’s not always true, lenders typically want something in return when it comes to doing a lot of paperwork to save you money. Therefore, you have to know what your one-time cost is to lower the interest rate for the life of your mortgage. For example, if it costs you $2,000 to refinance your mortgage and refinancing saves you $200 a month on your principal and interest, that results in a 10-month breakeven point. As long as you plan to stay in the home long enough to realize those monthly savings, it’s a sweet deal. And this is a good reminder that ALL you’re looking at is your principal and interest, not your escrow, which may include insurance and taxes. Your mortgage rate isn’t affected by how much you owe in property taxes or homeowners’ insurance, so it’s best to keep the comparison as clear as possible.

Let’s also imagine you refinance, and before you hit your break-even point, rates drop again, giving you another chance to refinance. What do you do? Another part of staying in the home long enough to see those monthly savings is considering whether you reasonably expect to be able to refinance again before reaching the break-even point. And this is where following Federal Reserve guidance can be helpful. As discussed, it’s not the primary driver of mortgage rates, but it is a part of the overall picture. So if they are signaling several subsequent rate cuts, it likely makes sense to wait until those are completed before taking action. Ultimately, if unexpected rate cuts occur, you’ll fall back on the same rule of thumb and treat the original refinance cost as a sunk cost. Saving money in the long run remains the goal, even if you misjudge the timing slightly.

Exercise Caution When Refinancing

Like most things, there are certain things to look out for when it comes to refinancing.

Upfront Costs

Don’t be fooled: just because there are no upfront costs on a refinance, it doesn’t mean there are no costs at all. When you roll costs into the loan, your monthly payments will go up. That’s why it’s crucial to not only know your mortgage rate, but also your Annual Percentage Rate (APR), which includes the total cost of the loan beyond just the borrowed amount.

Existing vs. New Lender

Even if your current lender is eager to work with you on a refinance, don’t assume those are the best terms you’ll get. While they are certainly a natural first step in inquiring about refinancing, remember that mortgages are sold all the time. You should compare their offer with what a new lender can offer. I suggest checking with both a local and a national company. There are also rate comparison sites online if you don’t mind receiving spam emails and calls.

Amortization Schedule

Let’s say you’re a few years into a 30-year mortgage and refinance to another 30-year loan. By definition, you’ll be making payments for over 30 years. But if you’re refinancing to a lower interest rate, it doesn’t matter how many extra years you add to the loan. You’ll still come out ahead over the life of the loan since you’re just lowering your existing balance’s interest rate, which results in less interest paid. Understand that you don’t necessarily have to refinance to another 30-year loan, though. You might try to match your remaining payments to 15, 20, or 25 years, whichever is closest to your original number of payments left. Some lenders will even match the exact number of years you have left on your existing loan. The other option is to refinance into a 30-year loan but keep making your same monthly payment, which effectively prepays your loan and saves you interest over the life of the loan.

When a Recast Might Be Beneficial

There’s a lesser-known approach to traditional refinancing called recasting. It’s for borrowers who can make a lump-sum payment of 10% or more of their loan balance. Although your interest rate won’t change, your lender might let you make a big payment toward your balance and reamortize the loan, resulting in a lower monthly payment going forward. As a result, you’ll keep your current payment schedule with a lower monthly payment rather than shortening the term of your loan. So this is a way of saving today instead of saving tomorrow.

Mike Turi, CFP® APMA™ is the Founder and a Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.