By now, you’ve hopefully developed a baseline understanding of just what exactly incentive stock options even are and have a working sense of how taxes fit into the equation. Equipped with that knowledge, the final step in readying yourself to make the most of your equity is to put all the pieces together. In this post, we put rubber to the road and dissect many of the decisions you’ll likely face with ISOs!

When it comes to ISOs, here are the high-level decisions you’ll face…

- Evaluate if you even want to exercise at all

- Determine how much you’ll exercise

- Calculate the cost to exercise

- Plan for how you’ll cover the cost

- Develop a strategy for when to exercise

- Decide when the shares will be sold

And, of course, manage the tax consequences throughout. It amounts to quite a bit, so the best thing you can do to position yourself for success is to get ahead of it!

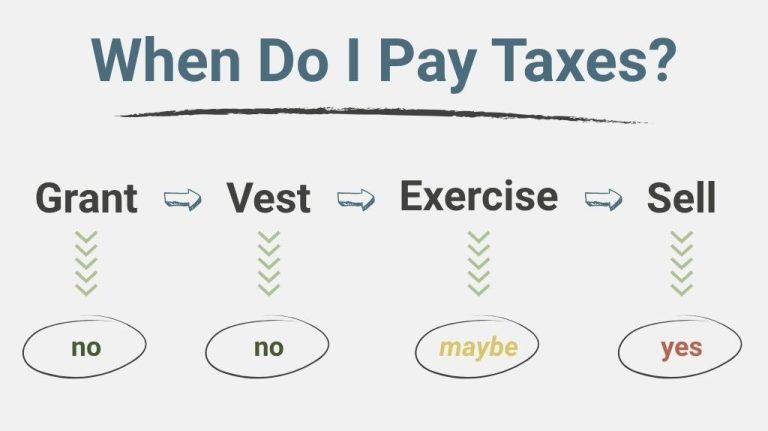

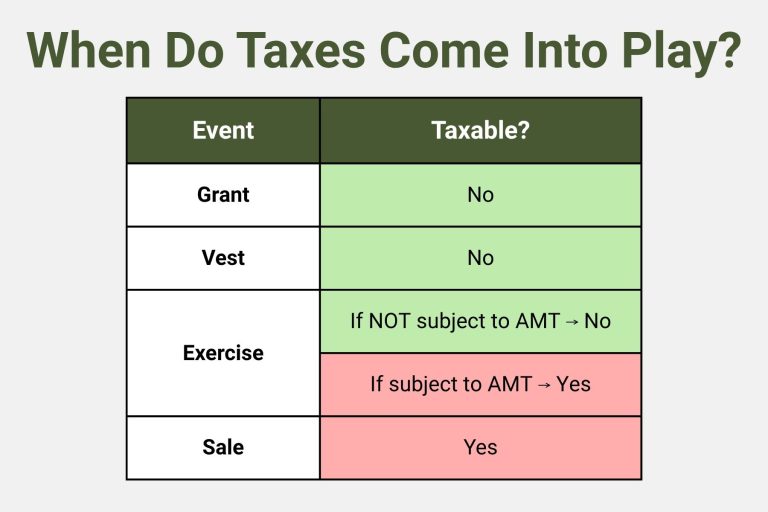

TO EXERCISE OR NOT TO EXERCISE?

Options are just that – options. You’re not required to do anything with them at all (though you often should!).

Evaluating whether or not to exercise is an investment decision above all else. So you have to first assess your personal comfort level with investment risk and understand how such risk will influence the rest of your financial picture. While ISOs have the potential to create real wealth, it’s also possible to lose money. Therefore, some initial questions you’ll need to answer first include:

How much do I believe in this company?

- If you’re super confident in its future success, then maybe it’s worth investing your money.

- If you’re doubtful, set some limits on what you put in, if anything at all.

How diversified is the rest of my investment portfolio?

- When you exercise, you now own stock in your company. Owning too much of any single stock creates added risk – think, “don’t put all your eggs in one basket”.

- Would exercising mean that a majority of your net worth is now tied directly to the performance of your employer? If this is the case, tread carefully.

- Once a holding of an individual stock starts to exceed 5% of your total liquid net worth, we want to be especially careful and really consider the impact on your goals given that stock’s potential performance.

- On the other hand, if after exercising you’d still have a healthy amount of your net worth allocated to other investment accounts that are well-diversified to suit your goals and risk tolerance, then it becomes a less risky decision to own the shares in your company.

Is my company private or public?

- This gets into how easily you’d be able to sell the shares after exercising.

- If your company is still private, know that it may be difficult (or impossible) to sell the shares until there’s some type of liquidity event, such as an IPO or acquisition. This can add a level of risk to the decision.

- If your employer is already public, or about to be, then selling will be far easier (though you may still need to be mindful of “blackout windows” during which you cannot sell). This can make exercising a little more manageable if you want to be able to quickly pivot away from holding the stock.

Can I afford the cost to exercise?

- We’ll dive more into how you can pay for the exercise below, but there’s certainly a real cost involved.

- Ultimately, it’s important to balance this with everything else you have going on.

As we continue from here, we’re going to examine very specific scenarios at each of the following stages…

HOW MUCH TO EXERCISE

Exercise up to the AMT limit as a ceiling

If you’re looking to optimize ISOs in such a way that the only taxes owed are long-term capital gains (no AMT or ordinary income tax), then this is the way to go.

The way it works… You’ll want to determine the available spread you could realize before tipping the scales into AMT territory. This will tell you how many options can be exercised without pushing you out of the standard tax system and then owing AMT. Staying within this limit means no taxes are owed in the year of exercise. For those who have a big pile of ISOs built up, it often means implementing this strategy over multiple years to exercise them all without ever triggering AMT.

Note: You would NOT want to do this if you have a large AMT credit, since it would diminish or prevent your ability to recoup that credit.

* A SPECIAL SECTION ON THE AMT CREDIT *

Hearing that you might owe more, or a different kind of tax can be anxiety-inducing. And it’s a valid response. The “standard” income tax system is unnecessarily complicated on its own. To learn there’s an additional tax system that often comes into the picture for those with ISOs is enough to make some people dizzy.

What is the AMT credit?

In reality, paying AMT isn’t always worth avoiding like the plague. That’s because you get a tax credit when AMT is paid. This credit is equal to the difference between the tax liability of the two systems. For example, if your AMT liability was $200,000 and your standard tax liability was $150,000…

- First of all, you’d pay AMT that year because it’s higher.

- Second, you’d get a credit of $50,000 ($200k – $150k).

Using the credit

This credit can then be used in future years, but only in years that your standard tax bill is higher (meaning you pay taxes under the regular system, not AMT). Additionally, the amount of credit you can use in those years is limited to the difference between the two tax liabilities. So let’s say you have the same $50,000 credit from above for a prior year and your current year’s tax situation looks as follows:

- Standard tax liability: $175,000

- AMT liability: $150,000

You’d pay the standard tax because it’s the higher amount, and you’d only be able to use $25,000 of the $50,000 credit for this year ($175k – $150k). The remaining $25,000 of unused credit carries forward to future years.

All this to say...

If you unexpectedly exercise ISOs to a point that forces you to pay AMT in a given year, all is not lost! Depending on the amount, it may be possible to “get it back”. Still, be mindful that if there’s a large enough bargain element, it could be quite a hurdle to cover the subsequent AMT bill that’s been created come April in the year following exercise – at least if you want to avoid selling the shares. Further, the process for recouping an AMT credit adds even more complexity that some may prefer to do without. There’s additional nuance involved that’s outside the scope of this post.

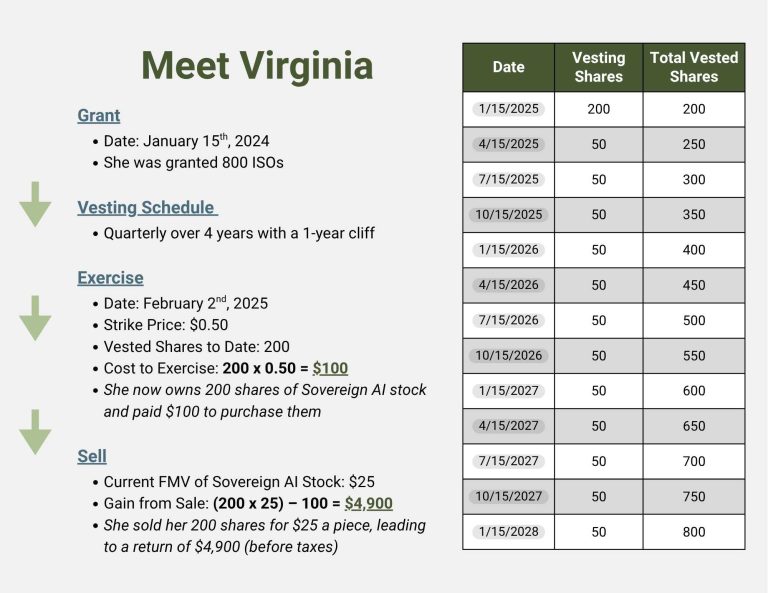

CALCULATING THE COST

This is straightforward! Simply multiply the exercise price (AKA strike price) by the number of options you plan to exercise.

Example...

- # of Vested Options: 500

- Strike Price: $4.50

- Cost to Exercise 500 Options: 500 x $4.5 = $2,250

* this does not include potential AMT, which should be factored into the cost if applicable *

HOW YOU’LL COVER THE COST

All stock option plans allow you to exercise by paying for the options with your own cash. Some plans will also allow for what’s called a “cashless” exercise, meaning you don’t have to come up with the funds yourself.

So, if you have the choice to make, the question becomes… Exercise with cash or go cashless?

How a cash exercise works…

- Simply come up with the cash (for example: take money from savings)

- Once you exercise, it’s entirely up to you as far as what you do with the shares next

- When you sell…

- How many you sell…

- How you cover the tax liability…

How a cashless exercise works…

- First, you need to check the details of your company’s stock plan to confirm that this exercise method is allowed by your employer.

- If it is, then you’ll need to select one of two routes for your cashless exercise:

- Exercise and sell to cover

- In this transaction, the desired number of options is exercised and, at the same time, enough shares are immediately sold so that just enough money is raised to cover the exercise cost (along with any fees and taxes).

- You keep the leftover shares to then sell when you want down the road.

- Put simply: exercise without bringing money to the table and walk away with shares in the company.

- Exercise and sell all

- Choosing this method means that your desired options are exercised and then ALL of the shares are simultaneously sold.

- In doing so, a portion of the proceeds is used to cover the cost of the exercise, plus any fees and taxes. The rest is paid out to you.

- Put simply: exercise without bringing money to the table and walk away with just cash.

So which one should you go with?

Consider a cash exercise if…

- You have plenty of liquidity (easy access to cash) over and above your emergency fund + any short-term needs, and are ok with the increased concentration of your wealth into the company stock.

- You want to maximize the number of shares you’re able to hold onto.

- You want the most control of the tax consequences and are targeting a qualified disposition for as many shares as possible.

Consider a cashless exercise if…

- You aren’t in a position to pull from savings or other resources to foot the bill.

- You are ok with some (or all) of the shares being sold right away as a disqualified disposition.

- You are ready to quickly capitalize on the value of the stock options

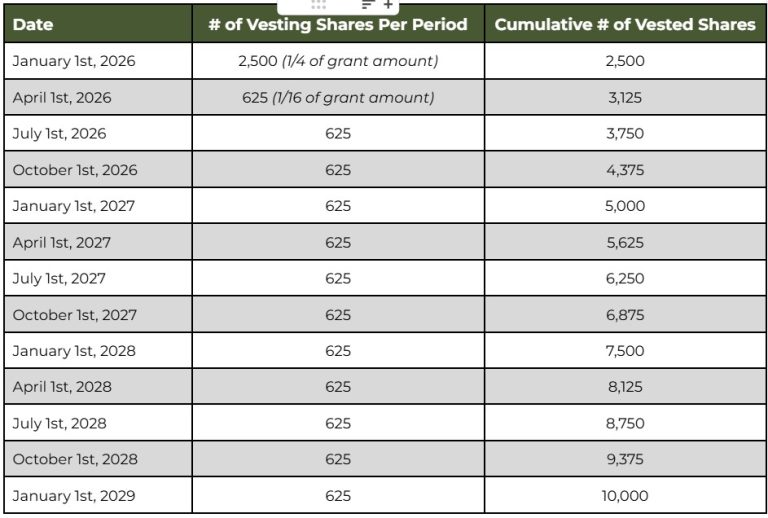

WHEN TO EXERCISE

There are a lot of alternatives when it comes to the timing of your exercise:

- Earlier in the overall vesting schedule

- Waiting until later on in the vesting schedule, or beyond

- An “early exercise” before they even vest

- Early within a calendar year

- Later in the calendar year

Why consider exercising sooner in the grand scheme of your award vest? (not referring to an 83b election – just earlier rather than later)

- Get a jump on the holding period requirement for the shares to be classified as “qualified” when eventually sold, earning long-term capital gains tax treatment on the full difference between the exercise price and FMV at sale.

- Allow yourself to exercise more options, given the AMT threshold…

- Earlier on in the lifecycle of your award grant and vest timeline, it’s more likely that the current FMV/409A of your company is lower, thus closer to whatever the exercise price of the options is (or in some cases, the same).

- If the spread is smaller, you’ll be able to exercise more options without pushing into AMT territory compared to if the FMV/409A of the company balloons significantly.

- In short: lower spread = lower AMT income realized

- You’re confident in the future performance of the company and expect the share price to increase. Plus you’re ok with the risk that the price could also go down if the company takes a turn, leading to a loss on your investment.

- You anticipate some type of liquidity event (IPO/acquisition) that would allow you to cash in on the shares in the future.

Why consider exercising later?

- You’re not confident in the future trajectory of the companyand you’d prefer to see how the share price moves before putting up the money to exercise the options.

- The options are currently “out of the money”… This means that the strike price is higher than the current FMV/409A. In other words, there’s no value to be gained. You’d pay more to exercise the options that you could get for selling the shares.

- You don’t have the cash on hand to easily cover the cost and/or there’s no ability for a cashless exercise.

Ok, what if you are able to “early exercise” with an 83b election?

Some companies will give you the ability to exercise your options early – even before they vest. If this is the case, it could deliver a big tax win.

The way it works… Instead of waiting a year+ to start exercising in many cases (based on the vesting schedule), you could choose to do so as early as being granted the options. Remember, the spread between the strike price and FMV at the time of exercise is what counts as income for calculating AMT. If this spread is very small, or even nonexistent due to the 409A being the same as the strike price early on – then it could translate to a large number of options exercised with little or no income under AMT.

This method would require coming up with the cash, as a cashless exercise isn’t a possibility at this point. So it might be a cost that’s not realistic or worthy to take on, depending on the strike price. It’s also an even earlier bet that your company will be successful and make the options worth something for you in the future, so there’s added risk involved.

Lastly, if you pursue this, you must file what’s called an “83b election” with the IRS within 30 days of the exercise.

Now, what about the timing of the exercise within the year – exercising early in the year vs. later in the year?

Exercise Later in the Year – Using the AMT Threshold as a Ceiling

If you are using the AMT threshold as a limit for how much you plan to exercise, as discussed earlier in this post, then it makes sense to wait until later in the calendar year. That’s because this approach requires a heavy level of tax projections. So it’s helpful to have the bulk of the data making up your full tax picture, which becomes clearer at the end of the year.

Exercise Early in the Year – To Maximize Choice

This technique only provides value if your employer is a publicly traded company.

Exercising early in the calendar year (no later than April) delivers some handy flexibility as you manage next steps by allowing you to:

- Decide between holding onto the shares long enough to meet the criteria for a qualifying disposition (more than 1 year), or sell during that same calendar year to avoid AMT.

- [Should you choose the first of the above two options] Have more time to plan for how you’ll cover the AMT owed, if any.

For example, if you exercise on February 1st of 2025, taxes are due in April of 2026 – a little over 14 months later. In this scenario…

- You could easily meet the holding requirement for long-term capital gains treatment that comes with a qualifying disposition (by selling after February 1st, 2026). Selling the shares would also raise cash that could be used to pay any AMT owed.

- On the other hand, if the share price drops during the same tax year to a point where there is no longer a capital gain, it very well may make sense to sell the shares as a disqualifying disposition. In this case, there would be no AMT owed, and there wouldn’t have been a benefit to holding for 1+ year if there was no capital gain to be realized.

What if you separate from your employer?

If your employment is terminated, an important clock begins ticking immediately: your vested ISOs will convert to nonqualified stock options within 90 days. NSOs are less beneficial from a tax standpoint since the spread at exercise is always taxed at ordinary income rates.

So if your goal is to exercise after separation and you want the tax benefits of incentive stock options, it will require you to act quickly. If, on the other hand, you’re good with the tax treatment of NSOs or simply don’t want to rush into an exercise, you may still have time – often up to 10 years. To be certain, it’s best to check with your employer to confirm the details of their “post termination exercise period” (PTEP) so you know how long you have before the options expire completely.

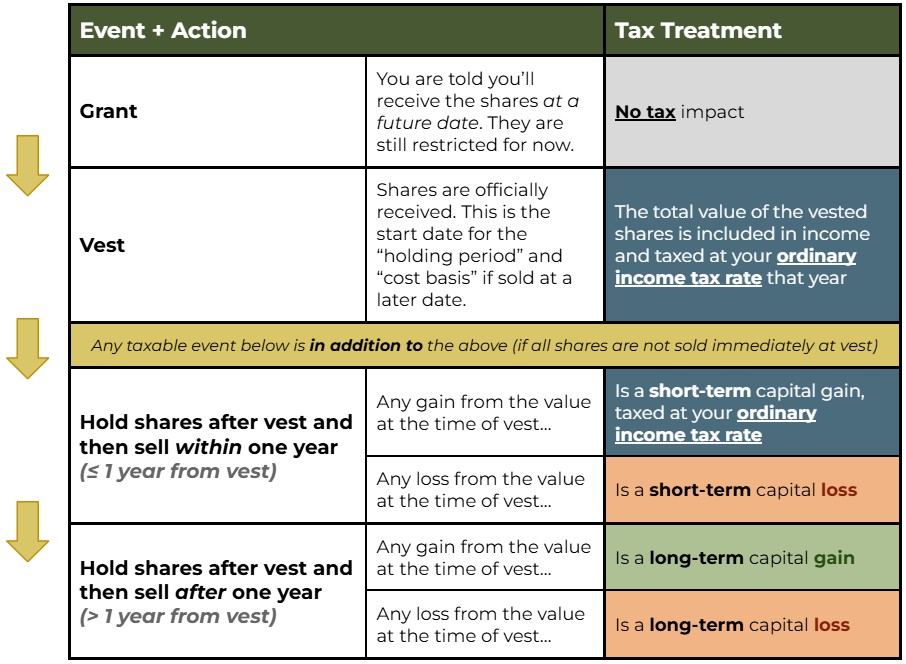

WHEN TO SELL

Hold onto the exercised stock long enough to meet the requirements for a qualifying disposition…

Holding the shares for at least 2 years from the grant date and at least 1 year from exercise allows you to take advantage of the kinder long-term capital gains tax rate when they’re sold (compared to your higher ordinary income tax rate).

* Keep in mind that this route requires you to factor in the potential AMT impact *

This is worth considering if:

- You are able to take on the added investment risk of a large position in your company’s stock.

- The cash that could otherwise be generated from selling isn’t needed for any short-term goals.

- You believe the stock price will increase with time (and are comfortable with the possibility of a decline in value).

You shouldn’t go for this if:

- You are uncomfortable with increased investment risk. Accumulating a big position of any single stock carries heightened risk, and often more so if that stock is in a younger company.

- The cash you could receive by selling will be instrumental in working toward an important goal (such as paying down high interest debt, funding a major purchase, etc.).

- You doubt the future performance of the company.

Selling sooner, as a disqualifying disposition…

Sometimes, your decision is – at least partly – already made if you’ve executed a cashless exercise. Remember, if you sell to cover → a portion of the shares is immediately sold to cover taxes. Or, as part of a cashless exercise, you may elect to immediately sell all the shares in the same transaction.

Selling all the shares immediately might be necessary to help cover the cost of exercising and the taxes, but it can also be strategic if the proceeds will be put towards another meaningful financial goal. Additionally, this is a way to simply reduce the risk that comes with building up a large portion of your net worth in your employer, by then investing the proceeds in a diversified portfolio.

Finally, unloading the shares as a disqualifying disposition becomes the smart move if it’s done to avoid paying AMT on shares that no longer look like they’d yield any capital gains – like I shared above.

Here’s an important point with all this…

- To some extent (*disclaimer to always check with your tax professional first*), it’s not necessarily worth getting all caught up in the mental tug-of-war over selling shares as a “qualified” or “disqualified” disposition.

- Remember that there’s inherent risk involved in holding onto the shares for over a year with the hopes of paying less in taxes by way of long-term capital gains treatment. For young companies, much can happen in those 365+ days after exercising. If the price takes a hit, it very well could erase any potential tax benefit you would have otherwise received.

- Money is money.

- If you’re prepared for the taxes involved, a disqualifying disposition can still be (and often is) an incredibly positive life-changing event.

- It could be what allows you to… buy that dream home, take the trip you’ve been putting off for years, spend more time with family, and so on.

- Don’t discount the value it delivers to your life just because it isn’t the most “optimal” tax scenario.

- If you’re prepared for the taxes involved, a disqualifying disposition can still be (and often is) an incredibly positive life-changing event.

MAKE IT HAPPEN

Given all the nuance involved, we always recommend working closely with a financial and tax professional to carefully evaluate the most appropriate path forward with incentive stock options. In doing so, they’ll be able to help you:

- Know the purpose of your plan… How will this resource best support you in achieving your ideal life?

- Lay out all of the options (not the ISOs, but the scenarios) side-by-side.

- Understand all the possible implications… The tax impacts, investment risks/benefits, what you’re saying “yes” to and what that means you’d be saying “no” to, etc…

- Create an action plan and put it into motion.

Building this plan in advance helps to minimize the emotion attached to the process and increases your chances of successfully following through.