Understanding Your First Paycheck for College Graduates

If you are anything like me, you may be surprised when you get your first paycheck. Until that moment, I had only worked jobs as an independent contractor, where earning a $1 meant actually receiving a $1. If you’ve accepted a job as a true W2 employee after graduation, you likely negotiated a salary that doesn’t reflect your actual take-home pay. It may not be close at all, leading you to wonder, “I think there is something wrong with my paycheck.” In this blog and the accompanying video, we clarify essential terms for recent college graduates and anyone curious about their paystub, providing a jump start to understanding the United States tax code.

Independent Contractor vs. Employee

First, it’s important to understand the difference between how the person is viewed performing the work for the business. Are you an employee of the company or an independent contractor? Certainly, some companies operate in a grey area when it comes to classifying labor. You may feel like an employee, only to discover after reading this article that you’re actually classified as an independent contractor, which essentially makes you a business owner! For this article, we will set aside the legality of the matter regarding your employer in the eyes of the Department of Labor.

There is nothing inherently good or bad about this, but there is a stark difference in your benefit eligibility, tax responsibility, and ability to make certain deductions. A deduction is something that ultimately lowers your taxable income. To qualify for many deductions, you need to be self-employed to take advantage of them.

For example, a remote worker cannot claim a home office deduction and deduct this expense from their income. However, if other eligibility requirements are met, an independent contractor can use the home office deduction to reduce their taxable income.

Important Paycheck Terms for Employees

There are three (3) general categories of deductions that reduce your gross pay.

Employee Taxes: Ordinary income tax + Federal Insurance Contributions Act (FICA) tax that funds Social Security and Medicare

Federal Income Tax

State Income Tax: 3% for Louisiana residents

Old Age, Survivors, and Disability Insurance (OASDI or Social Security): 6.2% on a maximum income of $176,100 in 2025.

Medicare: 1.45% + 0.90% on income over $200,000.

Pre-Tax Deductions: These will vary depending on your employee benefits, but the common ones are:

401k Contributions

Health/Dental/Vision Insurance Premiums

Flexible or Health Savings Accounts

Post-Tax Deductions: These will also depend on your employee benefits and selections, but the most common ones are:

Roth 401k Contributions

Some Life and Disability Insurance Premiums

Legal Insurance

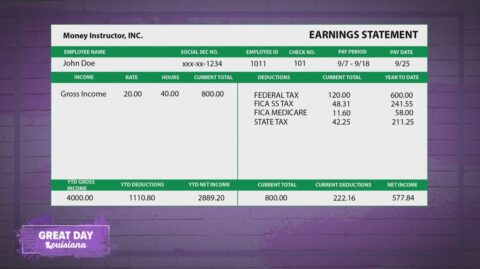

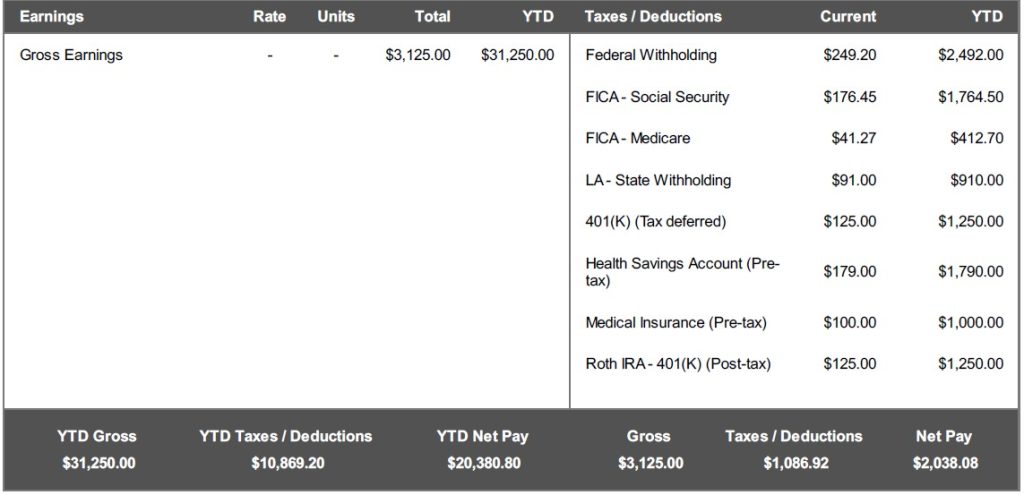

Sample Paycheck

As a basic and common example, here’s what a pay period might look like for an Individual earning $75,000.

Assumptions

- Tax Filing Status: Single

- No Dependents

- Pay Periods: 24 (Semi-Monthly)

- Pre-Tax 401k Contribution: 4% ($3,000 annual)

- Roth 401k Contribution: 4% ($3,000 annual)

- HSA Contribution: $4,300 (2025 Individual Max)

- Health Insurance Premium: $200/month

In this scenario, the employee’s net pay is 65% of their gross pay. 18% of their income is allocated to taxes, while 17% is earmarked for employee benefits, including health insurance and retirement savings. This leads to the individual having $2,174 less each month to allocate toward their budget for housing, transportation, food, and discretionary expenses.

If you’re unsure what your net pay might look like, I recommend using 60% as a baseline. This will provide a fair estimate of your actual pay that will reach your checking account before you commit to significant fixed expenses, such as rent or transportation. It also provides an opportunity to begin your journey as a saver or investor, as illustrated in the example above.

Does This Affect Independent Contractors Differently?

As an independent contractor, you’ll be paid, but you won’t get earning statements or paystubs detailing your income. But here’s what you need to understand: you owe taxes! The United States has a pay-as-you-go tax system. If you have income, you are generally required to make payments as you earn it. As an employee, this occurs through your paystub via mandatory company withholding, as shown above. For independent contractors, you are responsible for estimating what you will owe, setting that money aside, and remitting payment quarterly. If you don’t pay your estimated taxes quarterly, you could face underpayment penalties come the tax deadline (April 15th of the following year).

Here are the dates you are expected to estimate your quarterly taxes owed and pay by:

- Q1 January – March: April 15th

- Q2 April – June: June 15th

- Q3 July – September: September 15th

- Q4 October – December: January 15th

As stated, there are no safeguards in place, like the mandatory withholding for employees. If you haven’t paid any taxes, you’re in for a nightmare when your tax filing software spits out the amount owed. Additionally, you owe not only the employee side of the FICA tax but also the employer side (another 7.65%). We’ll save the nuance of correctly making self-employment deductions for another day! Some individuals may not fit neatly into employee or independent contractor categories; for example, one can be an employee while also running a side hustle. Keep reading…

Is My Company's Withholding For Me 100% Accurate?

At the start of employment, everyone will fill out a W-4 Employee Withholding Certificate to instruct their employer how much money to withhold for taxes. Unless you tell them otherwise, they only account for the money they are paying you, along with the information you provide regarding tax filing status and dependents.

Have a side hustle?

Your employer will only adjust your withholding if you instruct them to do so on your Form W-4 and accurately complete the form to take your additional income into consideration. Otherwise, you will need to manually calculate the taxes owed for this additional income and make quarterly payments, as mentioned in the section above regarding independent contractors.

The most accurate way to do this is to go online and use the IRS’s Tax Withholding Calculator.

Negotiating Your Next Salary

Not everything that reduces your gross pay to actual pay is bad. In fact, most are either beneficial or, at the very least, unavoidable, like taxes. In our sample pay stub above, this individual had access to a 401k retirement plan and a Health Savings Account. Although not shown here, most (but not all) employers offer matches for these types of accounts. That’s MORE money paid to you than you bargained for. When reviewing job offers or negotiating your salary, it’s crucial to assess the complete range of compensation and benefits available. The most significant variable beyond any form of equity compensation is always health insurance. How attractive are the plan options in terms of the premium amount, as well as the deductible and out-of-pocket maximum?

If you’re a recent college graduate, this is the first paycheck of (hopefully) many! Set aside time to understand the foundational aspects of it so you can prepare for future earnings.

Tips on negotiating your next salary? We got you!

Tips for selecting benefits during open enrollment season? We also got you!

Mike Turi, CFP® APMA™ is the Founder and a Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.