Too Much Cash?!

Yes, it’s possible.

Much like any time I sit down with a spoon and a pint of Ben & Jerry’s, the same holds true with cash… You can, in fact, have too much of a good thing. When it comes to the ice cream, I always do. When it comes to your cash, we want to help you avoid “overindulging”.

Of course, cash has its benefits:

- Security

- Financial flexibility

- Easy access to your money

Even so, there’s a very real tradeoff. What you gain in safety, you give up in potential growth and progress toward longer-term goals.

Risk #1: Inflation

As we all know too well, stuff gets more expensive over time – except, of course, for the Costco hot dog. One dollar today doesn’t buy what it did 20 years ago. This is the handiwork of inflation. It erodes the real value of money through the years, reducing your “purchasing power”.

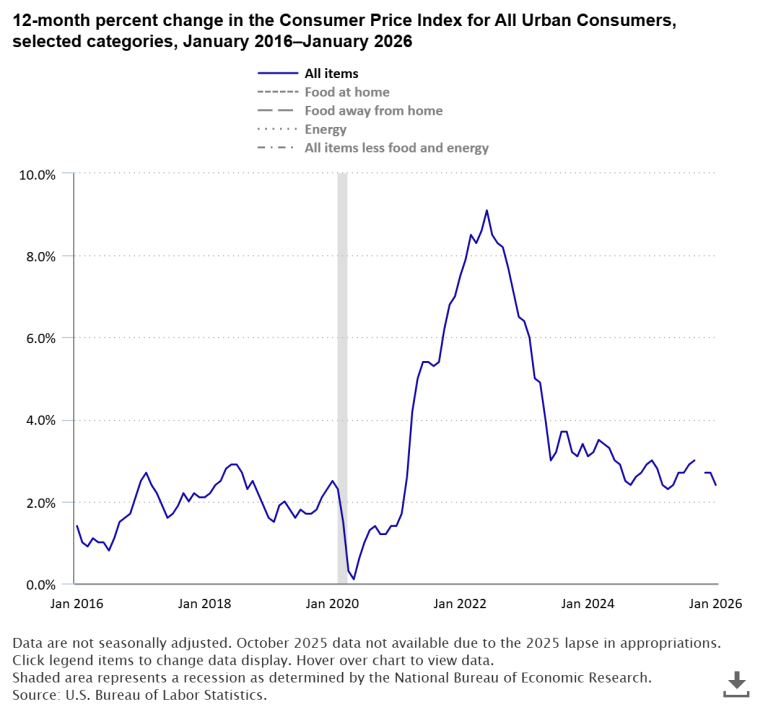

The graph below shows year-over-year inflation during the last decade.

Source: https://www.bls.gov/

Even now, with inflation cooling, prices were 2.4% higher in February of this year relative to February 2025.

If your dollars aren’t growing at a rate that outpaces inflation, you are losing money in terms of actual spending capacity. An account balance of $100k 30 years from now won’t do nearly as much for you as it would today.

In fact, going off inflation data for the last 30 years, it would do about HALF as much! To buy the equivalent amount of goods and services with $100k in 1996, you’d need $211k today (based on this CPI calculator).

Thanks, largely in part, to the post-COVID spike, the average annual inflation rate over the 10-year period between the start of 2016 and end of 2025 was 3.2%. The Federal Reserve has a target inflation rate of 2%. So even in “the best of times” prices are still expected to go up.

Cash vs. Inflation, an Example

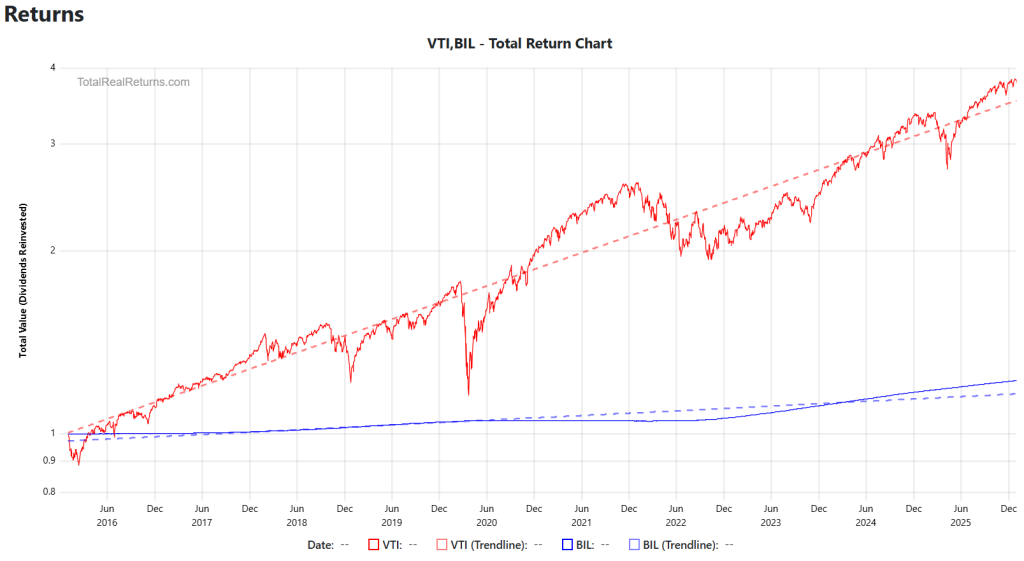

Let’s take a look at what inflation would have done to even a relatively favorable cash position over the last 10 years.

The State Street SPDR Bloomberg 1-3 Month T-Bill ETF (BIL), as the name indicates, invests in Treasury bills with maturities of 1-3 months. Because T-bills are issued by the US government, they’re considered to be nearly risk-free and are a “cash alternative”.

We’ll match that up to the overall US stock market, using the Vanguard Total Stock Market Index ETF (VTI). Specifically, we’ll view the performance of these two funds for the 10-year period from 1/1/2016 to 12/31/2025.

Assuming that dividends were reinvested, the overall return for each of these funds during the stated period was:

- BIL: 2.04%

- VTI: 14.25%

Here’s what that looked like:

Source: https://totalrealreturns.com/

If you were in search of safety for your money, BIL would have done well preserving your capital while earning some interest. $10,000 would have grown to $12,236.59. This is roughly what your cash would have done had it been sitting in a high-yield savings account during that stretch.

However, there’s one (now hopefully obvious) flaw here. The 2.04% overall return is before accounting for inflation. The returns above are what we call “nominal”. When we adjust for inflation, we work with what’s called the “real” return.

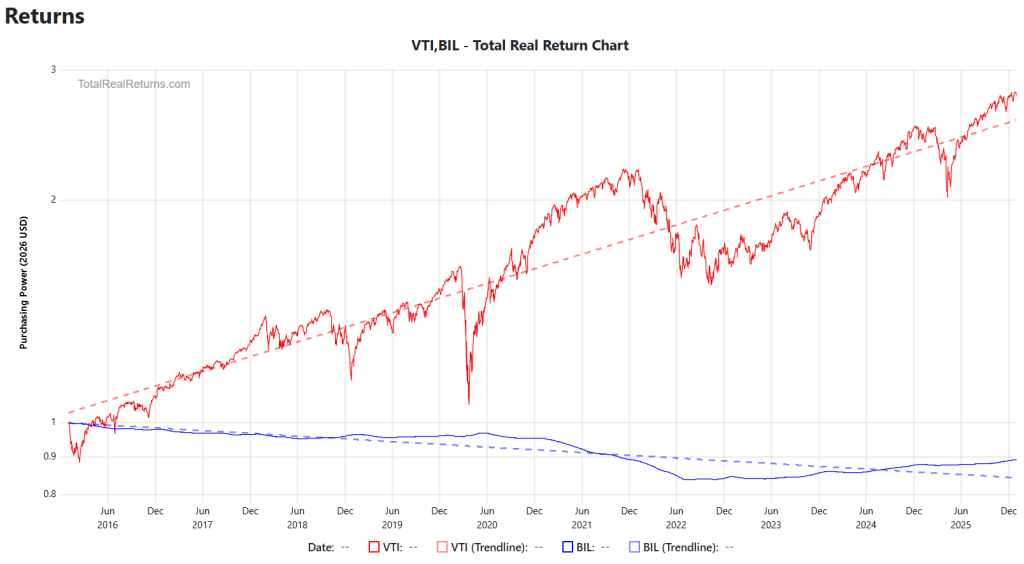

So here’s how those funds compare over the last 10 years with inflation (CPI-U) baked in…

Real Return

- BIL: -1.12%

- VTI: 10.71%

Source: https://totalrealreturns.com/

In terms of what your money could actually do for you, it would have lost value if left in BIL for 10 years.

If that same $10,000 was collecting dust in a checking account or traditional savings account, earning 0% to 0.05%?? Forget about it.

Risk #2: Longevity

At this juncture, some people out there may wonder, “What’s so bad about losing just ~1% over 10 years? At least my money wasn’t subject to big swings in the market. In the end, I barely lost any purchasing power.”

Well, sure. But it’s a simple fact: the longer you want (or need) your money to support your lifestyle, the more of it you need to have. So the growth rate of your assets over time directly contributes to the length of the runway you build up for yourself.

This isn’t to say you should go full throttle on the most aggressive investments you can get your hands on. There’s a wonderful world that exists between the extremes. But it underscores the importance of taking a risk-appropriate approach to growing your wealth so that you set yourself up for the best chance of success in realizing your ideal future state.

What is the RIGHT Amount of Cash to Hold?

To determine the “right” amount of cash…

- Calculate your Emergency Fund need

- Evaluate any short-term goals (new car, vacation, home project, etc.)

- Add these together and voila!

We recommend keeping these funds tucked away in a high-yield savings account. To take it one step further, we favor using an option like Ally that allows you to create “buckets” within a single account. That way, you can easily categorize the savings and always know exactly what each dollar is set aside for.

And bear in mind, the point of this cash is NOT to be a growth engine in your plan. Rather, it DOES…

- Cover you when something inconvenient inevitably occurs

- Help prevent the need for taking on higher-interest debts (credit card balances)

- Allow for quick and easy access

- Avoid market losses

OK, Now What?

Once you’ve established the optimal cash balance to keep on hand, it’s time to create a plan for the rest. One benefit of getting clear on your cash need is that it frees you up to take on more risk (appropriately) with other resources, creating more efficiency all around. Having adequate cash set aside increases your plan’s risk capacity. In other words, with your bases covered, you are in a position to handle greater risk in the accounts geared toward your long-term goals.

In short, that “extra” cash is ready to be invested.

Similar to what you did above, ask yourself: What is the purpose of these surplus funds? What will they ideally do for you? Additionally, consider the anticipated timeline before you expect to access them.

Addressing these points will guide what type of investment account those resources go into and how much risk you can reasonably take on when they get to work. For example, money tagged to help support your retirement at age 60 makes sense going into a Roth IRA, where it might be allocated to 100% equities. Funds that will be used to help with a down payment 6 years from now are not as well-suited in an IRA, nor should they be invested so aggressively. Those will serve you better in a taxable brokerage account, with a more conservative approach.

Cash plays a critical role in your financial plan. Yet, it pays to understand its limits and what to do if you can identify any excess.

Frequently Asked Questions for Cash

Q1: How much cash is too much to keep in savings?

You may be holding too much cash if you’ve already set aside enough for your emergency fund and any short-term goals, but still have a large amount sitting in checking or savings with no clear purpose. Cash is useful for flexibility and protection, but too much of it can quietly slow your long-term progress if it isn’t keeping up with inflation.

Q2: Why is holding too much cash a problem?

The biggest issue is that cash often loses purchasing power over time because of inflation. Even if your account balance stays the same, or grows a little, the real value of that money can decline if prices rise faster than your interest rate. Over long periods, that can create a meaningful drag on your financial plan.

Q3: Is cash losing value because of inflation?

Yes. Inflation reduces what your dollars can buy over time. That means money sitting in cash may feel “safe,” but if it isn’t earning enough to outpace rising prices, it is losing real value in the background. This is one of the main reasons excess cash can become costly over the long run.

Q4: Where should I keep my emergency fund?

Your emergency fund should usually stay somewhere safe, liquid, and easy to access—typically a high-yield savings account. The goal is not maximizing return. The goal is making sure the money is available when you need it, without taking market risk.

Q5: Should I invest money instead of leaving it in cash?

If the money is not needed for emergencies or short-term goals, investing may make more sense than leaving it idle in cash. The best place for that money depends on its purpose and timeline. Money needed soon should generally stay conservative, while money for long-term goals like retirement can usually tolerate more investment risk.

Q6: Is a high-yield savings account enough to beat inflation?

Not likely. A high-yield savings account can help reduce inflation drag compared with a traditional checking or savings account, but it won’t consistently outpace inflation over long periods. It can be a great tool for cash reserves, but it usually shouldn’t be your primary strategy for long-term wealth building.

Eddy Jurgielewicz, CFP® is a Partner and Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.