Spring Is Here, And It's Time to Declutter Your Finances!

We all know how the end of the year goes—dreaming about the year ahead. Perhaps making some grand declarations about new beginnings to a room full of friends and family—but tonight, they are really just fellow Chappell Roan fans. Dry January officially starts in five minutes, but having a drink after midnight doesn’t truly count. Who’s keeping track anyway?

And so it begins… by the time spring arrives, the ball, figuratively and literally, dropped long ago. What happened? We focused on the result, not the process. We aim to “get healthier,” but we haven’t actually established a framework to achieve it. We strive to “be more present,” but we haven’t clearly defined what that even means. Sometimes our biggest role as financial planners is to hold families accountable for the goals they set and the positive behavior changes they seek, or to help them clearly define those goals in the first place.

Ultimately, the most effective way to create change or drive positive impact is through small, sustainable actions. So, for today’s blog, we will help you *spring* into action to declutter your finances with a boring ass checklist to prevent costly mistakes. These steps offer a quick and dirty way to help you move closer to healthier financial habits without sacrificing your presence with loved ones, especially during festival season here in New Orleans.

Prioritize Obtaining Your FREE Credit Reports

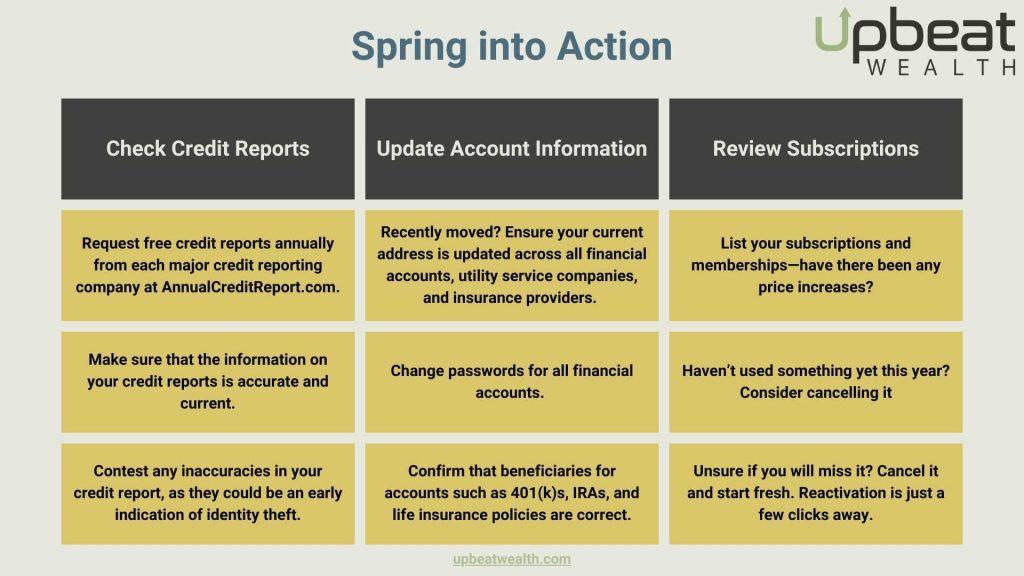

Wondering where to start checking off boxes on your spring to-do list? Start by reviewing your credit reports for free once a year at AnnualCreditReport.com.

THE ONLY INFORMATION YOU NEED:

- Name

- Birthday

- Social Security Number

- Current US Address

From there, you’ll be able to see reports from Experian, TransUnion, and Equifax. What *really* is a credit bureau and how do they work? Check out this helpful Investopedia article. For the purpose of this blog, these are the three bureaus that lenders will depend on to evaluate your creditworthiness. Your creditworthiness directly influences the amount you qualify to borrow and the interest rate offered. The higher your credit score or creditworthiness, the better your lending terms will be.

WHAT THE CREDIT REPORTS WILL SHOW YOU:

- Opened/Closed Credit Cards

- Mortgage Balances

- Installment Loan Balances (i.e. Auto or Student Loans)

- Lender Requests for your credit history

- Debts sent to a collection agency

- Public Records such as bankruptcy

One thing it won’t show you for free is your credit score, but that is merely a numerical representation of an accurate credit history. If you’d like to check your credit score, most major credit card companies permit you to view it online at no cost as a perk.

While a temporary government program permits you to check your credit reports weekly, we suggest reviewing them at least once a year and additionally a few months prior to making a major purchase. This provides you time to dispute any inaccuracies with the major credit bureaus and repair your credit history if needed, for instance, if you’ve been a victim of identity theft or incorrect reporting. Most importantly, periodic reviews of your credit reports can help minimize financial damage from someone attempting to defraud you by catching it early. Can’t imagine this will ever happen to you? A 2021 report from the Bureau of Justice Statistics found that 1 in 5 people had experienced identity theft in their lifetime.

Feeling Unsecure? How To Protect Account Information

In reality, we know most busy young people don’t log into their financial accounts all that much. And when it comes to checking investment balances, that’s not a bad strategy to minimize mixing emotions with investing. However, just because you might not use your login information frequently doesn’t mean someone else isn’t attempting to access it. Do yourself a favor: while wiping off the dust from your financial account logins to gather tax documents for your filing, refresh those passwords!

Additionally, ensure that your current address is accurately listed so your secure information isn’t sent to a previous address where it could fall into the wrong hands. This goes for financial accounts, utility service companies, and insurance providers. Heck, you might even unknowingly have an overdue bill that you’re missing because the notices are going to an old address. Then all of a sudden, you have a collections agency calling you… not good!

The next important piece of account information to review… your beneficiaries! Confirm they are correct. We often see these left incomplete, or even worse, the selections no longer reflect your wishes.

Popular Accounts for Beneficiary Designations:

- 401(k) or other Employer-sponsored Retirement Plans

- IRAs

- Bank Accounts (most states allow a Transfer on Death)

- 529 Plans (Successor Custodian)

- Life Insurance Policies

Setting your beneficiary designations correctly is an important first step in creating a proper estate plan. These designations at the account level will supersede your Last Will and Testament.

Don’t Kill My Momentum—I am Springing into Action

As previously mentioned, those New Year’s resolutions are likely far behind us. However, when it comes to your cash flow, now is an excellent time to review all of your memberships and subscriptions. As planners, we often discover bigger opportunities to assist families in increasing their cash flow through proper tax planning, intentional savings, student loan management, and much more. However, I believe that reviewing your subscriptions annually is a healthy practice. While your $20 Netflix subscription may not be the primary obstacle, if you’re not using it, it’s still money being wasted.

Individually, these subscriptions might not seem costly, but collectively, they can build up and eat away at your discretionary budget. Let’s be honest: the primary business model of these companies falls into one of two categories. They initially offered their services essentially for free but have raised the price each year since then, hoping you have become too dependent on the service to resist paying whatever they charge. Or you might have entirely forgotten that you were subscribed to the service in the first place.

Hence, our easy three-step guide to evaluate your memberships & subscriptions:

List them all out with their current pricing to see the cumulative monthly total. Don’t forget the annual subscriptions either!

Have any promotional offers that originally drew you in as a customer expired, or has the service’s price significantly increased from inception?

Have you used the service you’re paying for since the start of the year?

When in doubt, consider tearing it all down. What’s likely to happen is they will offer you a discount to stay with it. Or if you really do cancel and end up genuinely missing that service, you’re likely only a few clicks away from reactivating it as needed!

Mike Turi, CFP® APMA™ is the Founder and a Lead Financial Planner at Upbeat Wealth, a fee-only firm based in New Orleans and serving clients virtually across the country. He specializes in providing straightforward financial guidance to ambitious young families as they navigate life’s many milestones.

Do you have questions about what we shared in this post, or anything else in general? Feel free to schedule a free consultation or drop us a line!

Sign up for our newsletter (at the bottom of this page) to stay up to speed on our Upbeat Insight.